SMM, June 6:

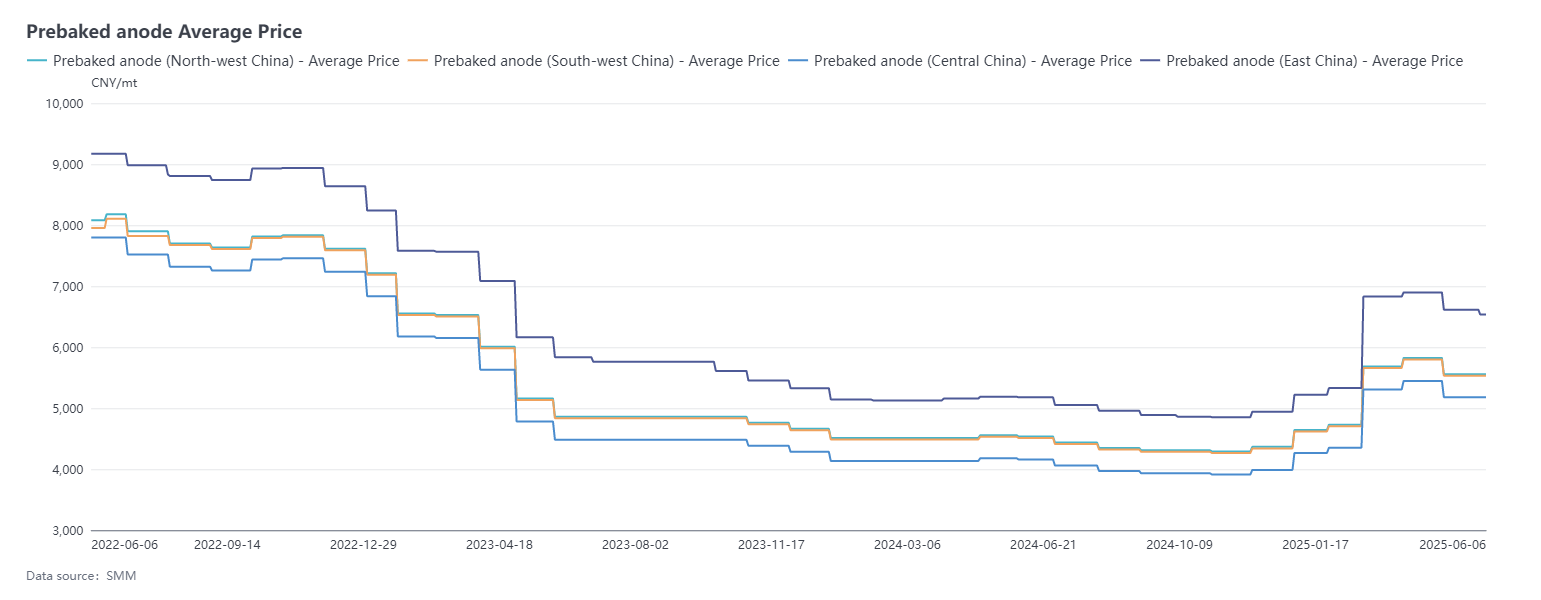

During the period from May 9 to June 6, SMM prebaked anode prices remained stable with a downward trend. The benchmark purchase price for a certain aluminum plant in Shandong in June 2025 was 4,939 yuan/mt, unchanged from the previous month's benchmark. According to SMM, the export order prices for prebaked anode in June were mainly adjusted downward due to falling costs, with adjustments concentrated around 15-30 US dollars/mt. As of now, SMM anode prices in east China closed at 4,939-8,133 yuan/mt.

Raw Material Side: During this period, the market performances of petroleum coke and coal tar pitch diverged. For petroleum coke, the price of low-sulphur petroleum coke continued to decline due to weak downstream demand. According to SMM statistics, in north-east China, the price of low-sulphur petroleum coke continued to fall during this period due to weak downstream demand. As of now, its average price was approximately 3,433 yuan/mt, down 13.26% from May 9. The price of petroleum coke from local refineries also continued to fall due to poor downstream purchasing enthusiasm. Entering June, with the end of the Dragon Boat Festival holiday, some enterprises slightly restocked, and the slight improvement in demand drove petroleum coke prices to stop falling and slightly rebound. As of June 6, the average price of petroleum coke from SMM local refineries had fallen to 2,293 yuan/mt, down about 5.72% from May 9. In the coal tar pitch market, the price center of high-temperature coal tar shifted upward during this period, and the price of coal tar pitch showed a fluctuating upward trend under cost support. According to SMM data, as of June 6, the average price of coal tar pitch was 3,997 yuan/mt, up 5.55% from May 9. Overall, although the market trends of petroleum coke and coal tar pitch diverged, the cost support for prebaked anode showed a downward trend.

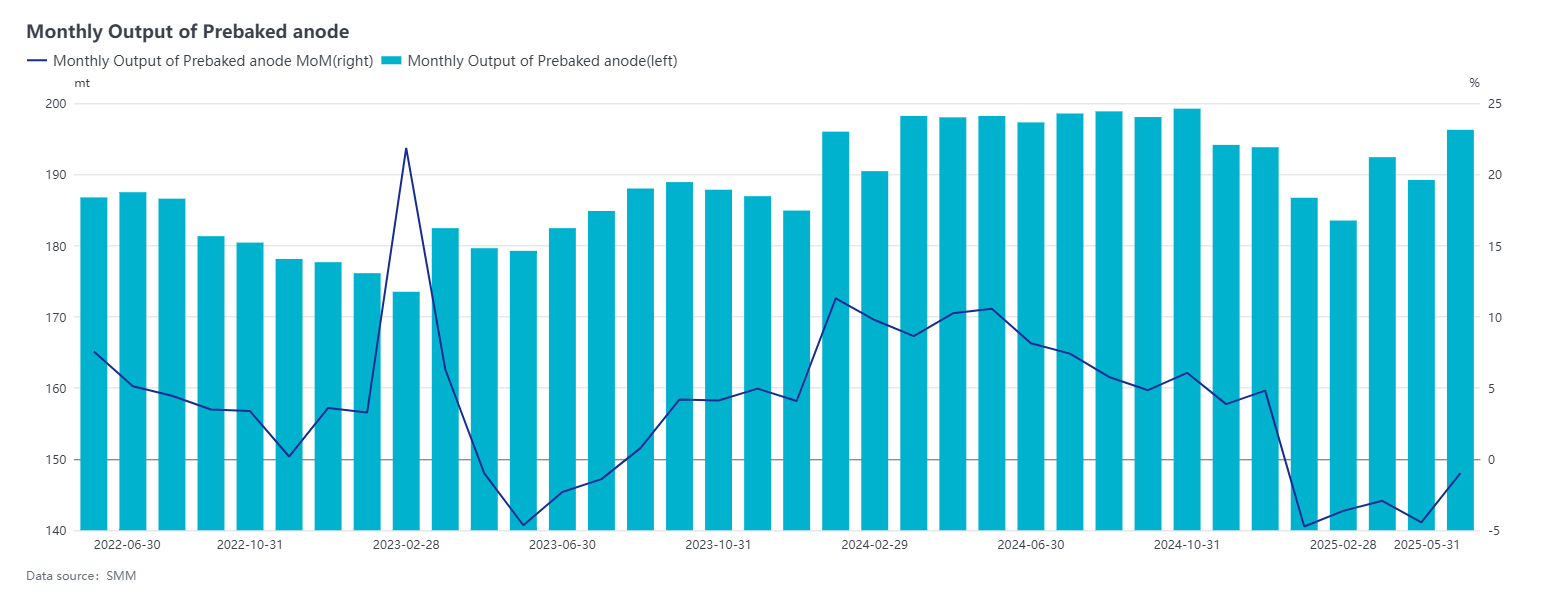

From the supply perspective, prebaked anode enterprises produce throughout the year according to orders. In May 2025, domestic prebaked anode enterprises operated steadily, with some enterprises increasing production due to the completion of maintenance; individual enterprises improved production through technological upgrades; and the commissioning of new projects in south-west China drove an increase in orders for prebaked anode green blocks in the region. This month, the transfer of aluminum electrolysis capacity from Shandong to Yunnan caused fluctuations in the demand for prebaked anode due to the capacity transfer. Additionally, with one more production day in May compared to the previous month, SMM data showed that the industry operating rate in May was 78.26%, up 2.81 percentage points MoM. The supply of prebaked anode remained stable with an increase, and the industry operating rate remained high.

From a demand perspective, China's aluminum industry in May 2025 demonstrated a parallel trend of capacity growth and structural adjustment. As of the end of May, the operating capacity of domestic aluminum smelters was approximately 43.91 million mt, with the industry's operating rate remaining flat MoM and increasing by 1.0 percentage point YoY to 96.1%. There were no new capacity additions, capacity replacements, or production cuts during the month, and the aluminum industry operated steadily overall. The second batch of projects relocated from Shandong to Yunnan is expected to be implemented in Q3, and SMM will continue to monitor changes in aluminum capacity. Entering June, the operating capacity of domestic aluminum smelters remained at high levels. Considering the progress of remaining new or replacement projects for the rest of the year, there are no short-term expectations for capacity commissioning. In overseas markets, although prebaked anode exports declined in April 2025, there were varying performances in segmented markets. Export orders to Malaysia, Indonesia, and Bahrain decreased significantly, primarily due to aluminum smelters depleting their existing inventories, leading to reduced demand for new orders. However, prebaked anode orders exported to Germany showed an increasing trend, closely related to the recovery of the European aluminum industry. As the European market recovers, increased demand has driven corresponding prebaked anode imports. According to SMM's survey, export orders performed well overall in 2025, with one of the main reasons being the continuous addition of new capacity and the resumption of production by some enterprises in overseas aluminum markets. This trend has boosted demand for prebaked anodes. Overall, the prebaked anode market in 2025 has demonstrated strong growth resilience, supported by dual demand from domestic and overseas markets.

Brief Commentary: A certain aluminum enterprise in Shandong has adjusted the benchmark tender price for prebaked anodes in June 2025, which remained flat MoM. Meanwhile, a major domestic prebaked anode sales company simultaneously lowered its sales pricing, with a MoM decrease of 142 yuan/mt. Despite varying performances in the raw material market, overall costs have declined. According to SMM data, as of June 6, the comprehensive cost of prebaked anodes in China fell to 4,670 yuan/mt, a significant decrease of 6.32% from May 9. The reduction in cost-side pressure has supported the industry's profitability. Based on a one-month production cycle, the profitability of the prebaked anode industry has significantly improved, with theoretical profitability increasing by approximately 350 yuan/mt MoM. Most prebaked anode enterprises are now in a state of marginal profitability. Entering June, domestic refinery maintenance and production resumptions coexist, with overall supply-side fluctuations remaining relatively small. However, with the continuous arrival of overseas petroleum coke and weak domestic demand, port inventories of petroleum coke have continued to rebound, resulting in a relatively abundant supply in the petroleum coke market. On the demand side, the operating rate of the prebaked anode industry is high, but enterprises' procurement enthusiasm is low, preferring a strategy of restocking at low prices. Meanwhile, orders in the anode material and graphite electrode markets are weak, and the previous stockpiling by glass and cement plants has been largely completed, leading to weakened demand. Therefore, the demand side remains generally sluggish. SMM expects petroleum coke prices to continue their downward trend in June, thereby exerting a sustained impact on the cost side of prebaked anodes. Considering the aforementioned factors, SMM expects prebaked anode prices to remain in the doldrums next month.