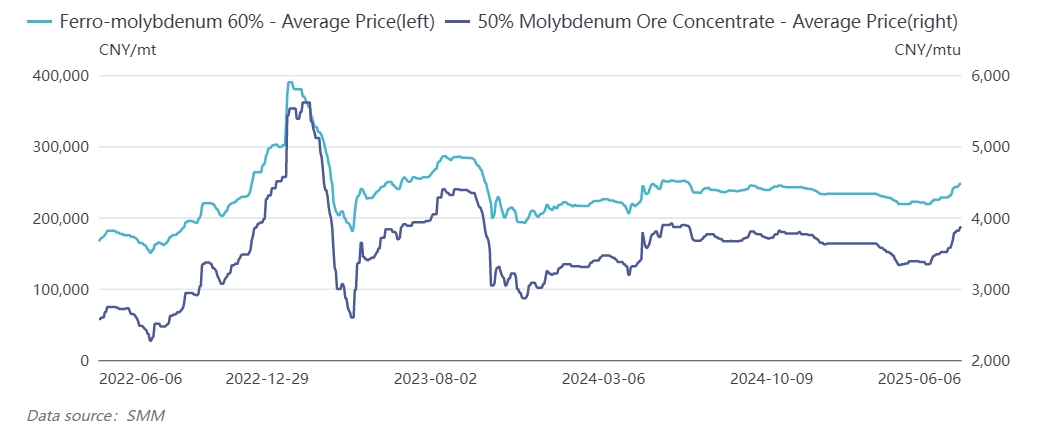

Entering June, the trend of the molybdenum market remains highly watched. At the beginning of the month, bidding prices of mainstream mines were successively finalized, with ore prices still maintaining a high upward trend. On June 4th, a mine in Jiangxi tendered and sold 45%-50% grade molybdenum concentrate at a transaction price of 3,865 yuan/ton-degree. Additionally, on June 6th, a mine in Henan sold 50% and above grade molybdenum concentrate offline at 3,870 yuan/ton-degree. As of June 6th, SMM's molybdenum concentrate quotation stood at 3,860-3,890 yuan/ton-degree, with an average price of 3,875 yuan/ton-degree, up about 7% from the beginning of the year and hitting a new high since February 2023. The downstream molybdenum iron (Mo60) price closed at 245,000-250,000 yuan/metric ton, with an average price of 247,500 yuan/ton, up about 6% from the start of the year. The high upstream prices have transmitted to downstream, and the prices of molybdenum metals and molybdenum chemical products have also shown an upward trend recently.

SMM believes that multiple positive factors have resonated, driving the strong price increase in this round of the molybdenum industry chain.

1. Coexistence of scarce mine resources and production capacity limitations

The overall growth of molybdenum concentrate slowed down in 2024, with the main increase coming from low-grade mines, while the growth of standard-grade mines overall slowed down. At the same time, the output of molybdenum concentrate from leading mines has decreased to varying degrees compared with the previous period. The output of some leading mines dropped significantly in 2024, leading to a further increase in the demand for market-circulating ore. According to SMM data, the domestic molybdenum concentrate output in 2024 was approximately 223,000 physical tons, a year-on-year decrease of 0.9%. In 2025, the expansion of molybdenum concentrate remains limited, and grade decline has become a common issue in the industry. SMM data shows that from January to May 2025, domestic molybdenum concentrate output was approximately 87,700 physical tons, a year-on-year increase of nearly 7%. Among them, the output of molybdenum concentrate in May decreased slightly month-on-month. The limited capacity release and grade decline of molybdenum mining enterprises at the raw material end have led to a "hard gap" in the raw material supply, which has strongly supported molybdenum prices.

2. Dual-wheel drive of demand from traditional and emerging fields

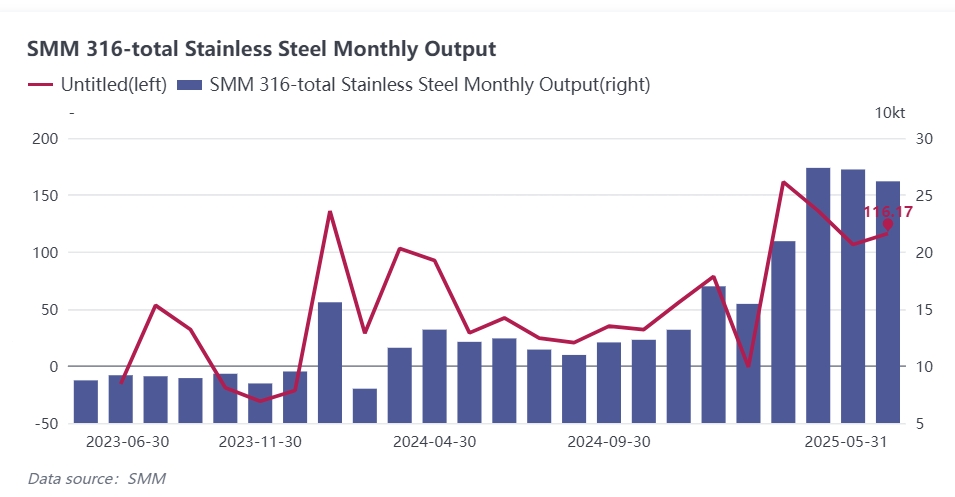

Molybdenum has advantages such as high strength, high melting point, corrosion resistance, and wear resistance, and is widely used in steel, petroleum, chemical, electrical and electronic technology, medicine, and agriculture. Approximately 80% of molybdenum's direct consumption is used in the steel industry in the form of roasted molybdenum concentrate or molybdenum iron and other molybdenum charge materials, while the rest is used in molybdenum chemicals and molybdenum metal products. In recent years, benefiting from the acceleration of global energy, nuclear power construction, petrochemicals, and infrastructure investment, demand has grown in fields such as pipelines, storage tanks, reactors, seawater desalination equipment, shipbuilding, nuclear power, and new energy, driving a year-on-year increase in domestic molybdenum-containing stainless steel production with a significant growth rate. SMM data shows that from January to May 2025, the domestic production of 316/316L stainless steel was approximately 1.172 million tons, a year-on-year increase of 96%. The growing demand for molybdenum-containing stainless steel has greatly driven the demand for products such as molybdenum iron. According to SMM calculations, the average monthly steel procurement volume of molybdenum iron from January to May reached 13,000 tons. In June, multiple steel mills in Jiangsu and Hebei released procurement volumes, and the transaction focus of molybdenum iron also followed an upward trend.

3. Promotion by industry policy factors

In February 2025, the Ministry of Commerce implemented export controls on strategic metals such as tungsten and molybdenum; at the beginning of June, multiple departments jointly deployed measures to prevent the illegal outflow of strategic minerals, with resource-rich provinces such as Guizhou taking the lead in responding. The policies aim to safeguard national security, and these measures have intensified expectations of a global molybdenum supply shortage. Export control policies have restricted the outflow of molybdenum-related products, making the domestic market supply relatively concentrated, enhancing domestic market control over molybdenum prices, and pushing up global molybdenum industry prices.

SMM Brief Comment: The molybdenum market has shown a rapid upward trend driven by multiple positive factors such as comprehensive supply-demand dynamics and policy factors. In the short term, under the combined influences of tight raw material supply, increased bullish expectations, and downstream just-in-time replenishment, the market remains in a phase of 供不应求 (supply falling short of demand), supporting the high-level operation of the molybdenum market. However, in the medium to long term, prices of products such as molybdenum iron have continued to rise since April, leading to poor profit margins for downstream steel mills. Some stainless steel mills have already reduced production in May, and as steel production gradually enters the traditional off-season, accumulating downstream pressures may suppress market growth space. In the future, it is still necessary to pay attention to changes in mine operations and downstream demand.

![Baiyin Nonferrous Group Co., Ltd. Copper Tendered 1 mt of Tellurium Ingots [SMM Report]](https://imgqn.smm.cn/usercenter/cgspx20251217171725.jpg)