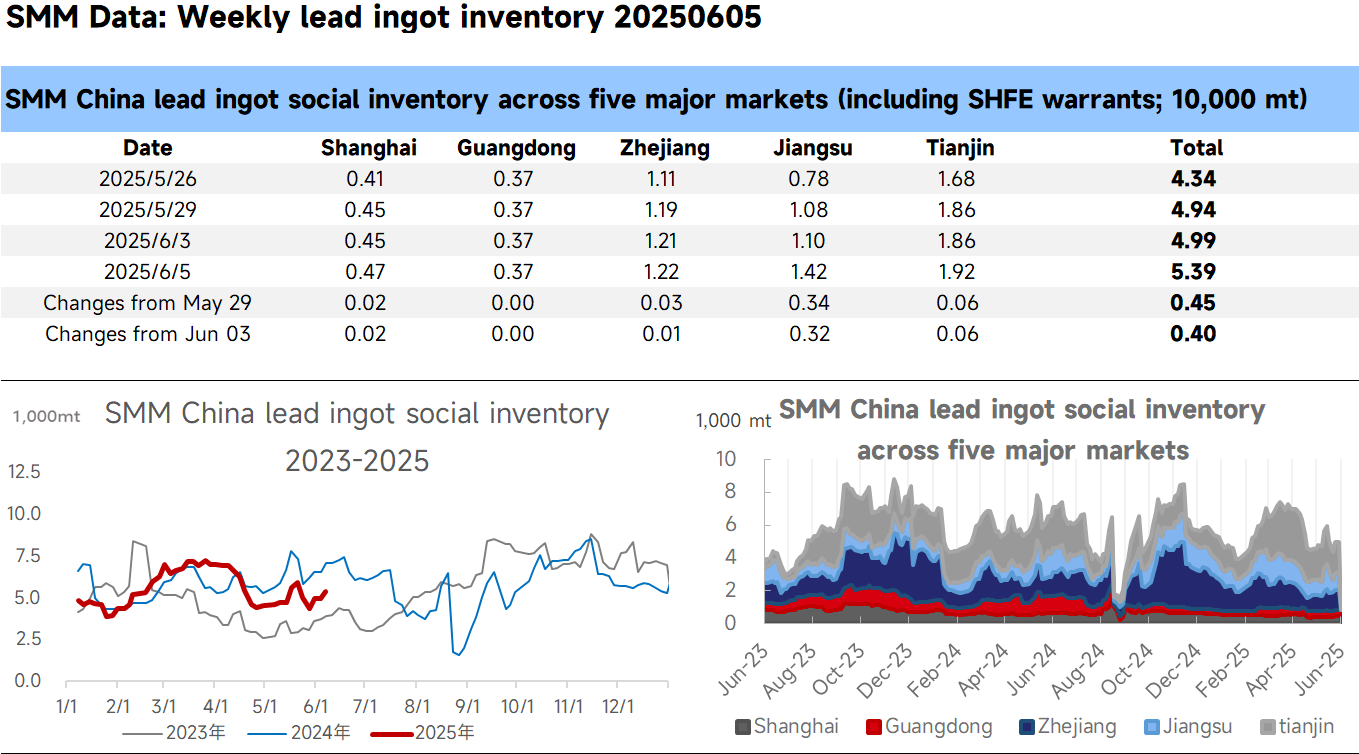

SMM News on June 5: According to SMM, as of June 5, the total social inventory of lead ingots across five locations tracked by SMM reached 53,900 mt, an increase of 4,500 mt from May 29 and an increase of 4,000 mt from June 3.

This week marks the first week after the Dragon Boat Festival holiday. Lead smelters and traders have been actively selling, with suppliers in Hunan province generally expanding discounts for shipments. Quotations were at discounts of 60-40 yuan/mt against the average price of SMM 1# lead ex-factory. In Henan province, suppliers' quotations were at discounts of 200-180 yuan/mt against the SHFE lead 2507 contract ex-factory. After conversion, the spread between futures and spot prices for lead in both regions has reached or even exceeded 200 yuan/mt. The widening spread between futures and spot prices has prompted suppliers to transfer inventory to delivery warehouses, leading to a further increase in the social inventory of lead ingots. The off-season trend in the lead-acid battery market in June persists, with downstream enterprises mostly in a state of production cuts and being cautious about raw material procurement. Some enterprises engaged in buying the dip during the period when lead prices fell early in the week. Therefore, except for a significant increase in lead ingot inventory in Jiangsu province, inventory growth in warehouses in other regions has been limited. Additionally, next week is the week before the delivery of the SHFE lead 2506 contract, and there is still an expectation of suppliers transferring inventory to delivery warehouses, so the social inventory of lead ingots will continue to rise.