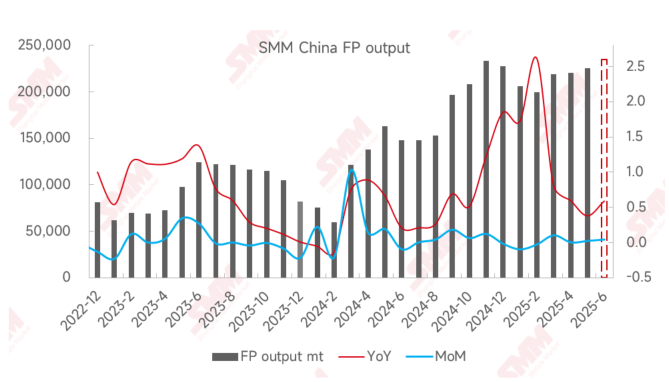

In May, the domestic iron phosphate market remained stable, with production up 2% MoM and surging 38% YoY. On the supply side, the resumption of production by integrated LFP enterprises drove an increase in self-supplied iron phosphate output. Enterprises with cost advantages in raw materials secured more orders with stable production lines, while those with stable prices maintained production levels similar to the previous month. On the demand side, downstream demand for LFP showed a rebound compared to April. In terms of costs, prices of industrial-grade MAP and phosphoric acid remained stable, while ferrous sulphate prices rose, keeping iron phosphate production costs at a high level.

As June approaches, marking the period for pushing for mid-year targets, enterprises will strive to capture market share through sales promotions and volume increases. Simultaneously, new capacities will gradually come on stream and undergo downstream validation. It is expected that iron phosphate production will increase by 4% MoM and 59% YoY in June, potentially intensifying market competition.