On May 29, at the 2025 SMM (2nd) Rare Earth Industry Forum hosted by SMM Information & Technology Co., Ltd. (SMM), Su Zhanpeng, an analyst from SMM's Rare Earth Division, shared insights on the transformation of the NdFeB industry driven by policies, the restructuring of supply and demand, and strategies for enterprises to break through.

NdFeB permanent magnets dominate the permanent magnet materials market, with high-performance NdFeB leading the industry's development.

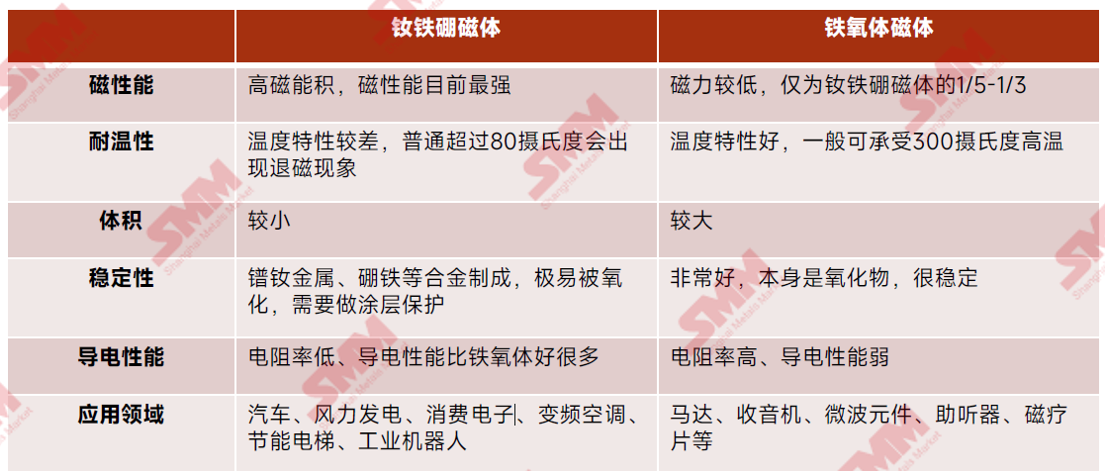

Overview of Magnetic Materials: Currently, magnetic materials are mainly divided into two categories: permanent magnet materials and soft magnetic materials. Permanent magnet materials possess enduring magnetism and are the most widely used magnetic materials. Among them, NdFeB alloys and ferrite permanent magnet materials hold significant positions in the technological field. On the other hand, although soft magnetic materials can be magnetized under the influence of an external magnetic field, their magnetism is unstable and easily lost due to external factors.

Compared to ferrite, NdFeB exhibits higher BH and coercivity, enabling it to provide stronger magnetic performance in a smaller volume. Meanwhile, NdFeB permanent magnets, with their high energy density and stability, are irreplaceable in high-end industrial, new energy, and consumer electronics applications, while ferrite, due to its performance limitations, is mostly used in low-power, low-cost, low and mid-end applications.

Overview of NdFeB Permanent Magnet End-Use Markets

The end-use markets for NdFeB permanent magnets are mainly concentrated in six areas: consumer electronics, NEVs, clean energy, new-type fields, energy-efficient elevators, and energy-efficient home appliances. Among these, emerging markets such as NEVs, energy-efficient home appliances, wind power generation, and industrial robots account for the majority of the market share.

In 2025, the increasing penetration of NEVs, the rise of emerging economies such as humanoid robots and the low-altitude economy, and the national subsidy policies in the home appliances and consumer electronics sectors will continue to inject new vitality into the future market of NdFeB. However, due to adjustments in the real estate market and technological breakthroughs in wind power raw materials, the demand for NdFeB in energy-efficient elevators and wind power generation has decreased.

Analysis and Forecast of NdFeB End-Use Demand

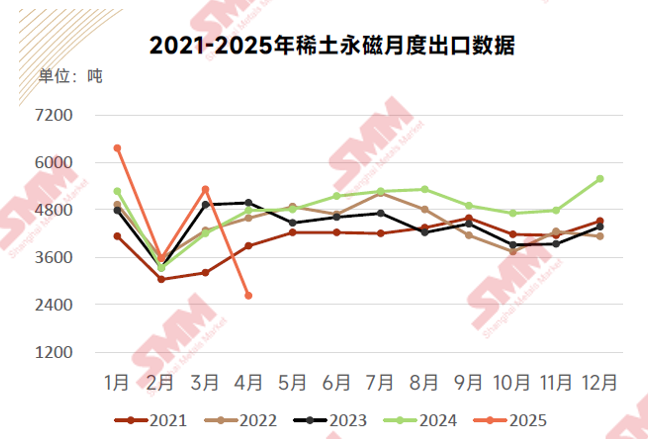

Affected by export controls, rare earth permanent magnet exports in April 2025 decreased by 45% YoY.

In April 2025, rare earth permanent magnet exports were affected by export controls, decreasing by 45% YoY and 51% MoM. However, the cumulative export volume from January to April increased by 2% YoY.

Due to the newly implemented export control measures in April, there has been a certain impact on export trade, resulting in a need for improvement in recent export conditions. With the smooth recovery of exports of magnetic materials that do not contain medium-heavy rare earth and the sequential approval of licenses for those that do, rare earth permanent magnet exports will show a trend of recovery, but it will be difficult to restore the original export volume in the short term.

China's NEV production in 2025 is expected to reach 17.89 million units, up approximately 29% YoY.

According to CAAM data, full-year 2024 NEV production and sales reached 12.888 million and 12.866 million units respectively, up 34.4% and 35.5% YoY. China's NEV market maintained growth momentum in 2024, with sales accounting for 40.9% of total auto sales. NdFeB demand from NEVs reached 57,000 mt, up 38% YoY.

In 2025, NEV policies will feature "central coordination + local refinement", promoting market penetration through consumption subsidies, technical support, and public sector pilots. NEV production is expected to maintain rapid growth, with China's output projected at 17.89 million units (up 29% YoY), market penetration likely exceeding 55%, and total NdFeB demand reaching 75,000 mt.

China's new wind power installations in 2025 are forecast at 87GW, up 8% YoY.

Per National Energy Administration statistics, China added 80.454GW of wind capacity in 2024 (up 6% YoY), with NdFeB demand at 9,735 mt (YoY growth rate down 21%). Due to cost constraints, the penetration rate of direct-drive motors has declined annually, leading to reduced NdFeB demand from China's wind installations in 2024.

As a key end-use sector for rare earths, although demand growth from wind power has slowed recently, it remains a major long-term driver for sustained rare earth demand. Projections indicate China will add 87GW of wind capacity in 2025 (up 9% YoY), requiring 8,341 mt of NdFeB.

China's 2025 air conditioner production is expected to reach 320 million units, up 18% YoY.

NBS data shows China produced 270 million air conditioners in 2024 (up 10% YoY), with NdFeB demand at 21,000 mt (YoY growth rate 26%). Since September 2024, government trade-in subsidies combined with promotional events like "Double 11" and year-end sales have boosted the home appliance market.

In 2025, the home appliance sector will demonstrate positive development trends driven by recovering demand, technological innovation, and policy support. Expanded trade-in subsidies will significantly boost air conditioner production and sales. Output is projected at 330 million units (up 25% YoY), generating 26,000 mt of NdFeB demand.

It is projected that the production of energy-efficient elevators will reach 1.41 million units in 2025, down 3% YoY.

According to the latest data from the National Bureau of Statistics (NBS), in 2024, the national production of elevators, escalators, and lifts was 1.458 million units, a 5.8% decrease YoY. The demand for NdFeB was 7,508 mt, with the YoY growth rate of demand declining by 6%. In 2024, the adjustment of the real estate market had a certain impact on the demand for new elevator installations.

In 2025, the demand for elevators in infrastructure, industrial sectors, and retrofitting projects in old residential communities is expected to grow significantly. In particular, the export market in countries along the "Belt and Road" initiative provides new growth opportunities for Chinese elevator enterprises. It is projected that the production of energy-efficient elevators will reach 1.41 million units in 2025, down 3% YoY, and the demand for NdFeB will reach 7,368 mt.

It is projected that the production of mobile phones will reach 1.85 billion units in 2025, up 10% YoY.

According to the latest data from the NBS, in 2024, China's mobile phone production was 1.68 billion units, up 7.3% YoY, and the demand for NdFeB reached 3,362 mt, up 7.3% YoY. In 2024, the "national subsidy" policy implemented by the state provided generous purchase subsidies to consumers, significantly stimulating market demand.

With the recovery of the mobile phone industry and technological innovation, the rare earth industry will gain new development opportunities. The increase in market demand for mobile phones will drive the expansion of capacity and technological progress in the rare earth industry. It is projected that the production of mobile phones will reach 1.85 billion units in 2025, up 10% YoY, and the demand for NdFeB is expected to reach 3,698 mt.

It is projected that the production of industrial robots in China will reach 941,000 units in 2025, up 55% YoY.

According to the latest data from the NBS, in 2024, the cumulative production of industrial robots in China was 608,000 units, up 41.4% YoY, and the demand for NdFeB was 12,147 mt, with a YoY growth rate of 41%. With the deepening implementation of the national "Intelligent Manufacturing 2035" action plan, combined with special government subsidies for robot industry clusters and the outbreak of emerging application scenarios, the acceleration of industrial automation transformation has been further promoted, leading to a continuous expansion in the demand for industrial robots.

2025 is regarded as the first year of mass production for humanoid robots, and the high growth prospects of this industry have created new growth opportunities for the rare earth permanent magnets market. It is projected that the production of industrial robots in China will reach 941,000 units in 2025, up 55% YoY, and the demand for NdFeB is expected to reach 18,828 mt.

Review and Forecast of NdFeB Supply

It is projected that China's rare earth mining quotas will remain unchanged in 2025.

On February 19, 2025, the Ministry of Industry and Information Technology (MIIT) issued the "Administrative Measures for the Regulation of Total Rare Earth Mining and Smelting and Separation" and the "Administrative Measures for the Traceability of Rare Earth Product Information."According to the "Administrative Measures for Total Volume Control", the scope of rare earth ore products in China explicitly includes imported ores from overseas, monazite by-product ores, etc. For the first time, imported resources have been incorporated into smelting and mining quotas for total volume control. It is projected that the rare earth smelting and separation quota will reach 350,000 mt in 2025.

On April 4, 2025, the state announced the implementation of export control policies for medium-heavy rare earth, which partially impacted the NdFeB market. Based on the analysis of the current market situation, SMM expects that rare earth mining quotas in 2025 may remain flat. This includes 251,000 mt of rock-type rare earth and 19,000 mt of ion-adsorption type rare earth.

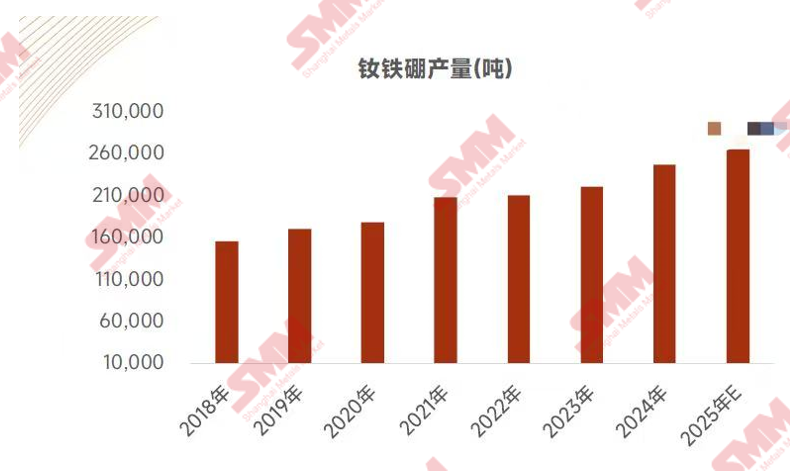

NdFeB production in 2025 will continue to rise due to supply and demand dynamics.

As the largest producer of rare earth permanent magnet materials, China has maintained a steady growth trend in both production and consumption of rare earth permanent magnet materials in recent years. In 2024, China's rare earth permanent magnet material production was approximately 246,500 mt, up 14% YoY. It is expected that production will reach 265,000 mt in 2025.

In 2025, several top-tier enterprises have expansion plans, including those in Zhejiang, Jiangxi, Inner Mongolia, Beijing, etc. However, due to the impact of export controls, rare earth permanent magnet exports have decreased, affecting NdFeB production and potentially delaying enterprise expansion plans.

China's Rare Earth Supply-Demand Pattern and Market Outlook

Monthly NdFeB Supply-Demand Balance and Future Projections

The supply-demand gap widened in November-December 2024, mainly due to the concentrated release of end-use demand at year-end, such as wind power projects pushing for annual installation targets at year-end. Downstream end-user production increased, leading to a surge in NdFeB demand. In January-February 2025, end-use demand decreased following the concentrated release in Q4 2024 and the approaching Chinese New Year, with magnetic material enterprises reducing their operations.

From April to July 2025, exports plummeted due to export controls. Additionally, May is a traditional off-season, and magnetic material enterprises took fewer orders due to end-use demand, resulting in lower supply. As end-use demand recovered in June, the supply-demand gap continued to widen. Starting from August 2025, export license approvals were gradually granted, leading to a rebound in exports. In September, influenced by the end-use market's advance stockpiling for production, demand surged.

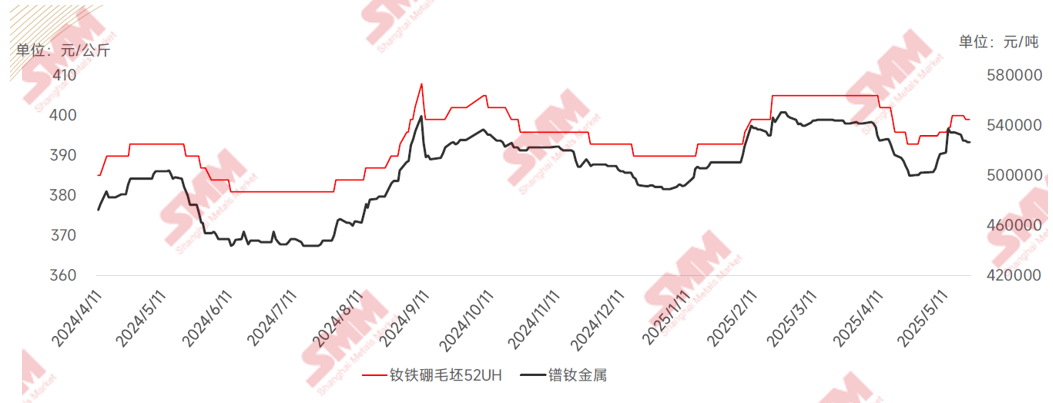

Review and Causes of NdFeB Price Trends from 2024 to 2025

Taking 52UH as an example, as of December 31, 2024, the price of 52UH blanks was reported at 390 yuan/kg, up 25 yuan/kg from 365 yuan/kg at the beginning of the year, representing a 6.8% increase.

As the most widely used blank grade in NEVs, the price of 52UH is influenced by end-use supply and demand and raw material prices, showing an overall upward trend. However, under the impact of the export control policy announced in April 2025, export orders decreased significantly, causing prices to pull back. With the implementation of policies and the increase in end-use demand, it is expected that prices will rise slightly in the later period.

Outlook for Rare Earth Development Trends in 2025

Demand Side:

1. Affected by export control policies, the exports of rare earth permanent magnets have significantly decreased. Despite the sequential approval of export licenses, it will be difficult to restore the original export volume in the short term.

2. In 2025, China's NEV industry will enter a critical stage of high-quality development, with significant breakthroughs expected in industry scale, technological innovation, market penetration, and other aspects.

3. In 2025, new installations of wind power will continue to grow due to the influence of green transformation and low-carbonization. However, due to technological iterations in raw materials, the demand for NdFeB in onshore wind power projects will decrease. Nevertheless, with the development of offshore wind power, the demand for NdFeB will surge. In the long run, it will remain the main driving force for the sustained growth of rare earth demand.

4. In 2025, the home appliance industry will show a positive development trend driven by the recovery of market demand, technological innovation, and policy support, leading to a continuous increase in the demand for NdFeB.

5. In 2025, energy-saving elevators will be affected by adjustments in the real estate market, but the demand for elevators in infrastructure, industrial sectors, and the installation of elevators in old residential communities will increase significantly, resulting in a relatively small decrease in the demand for NdFeB.

6. In 2025, with the recovery of the mobile phone industry and technological innovation, the increase in mobile phone market demand will drive the expansion of capacity and technological progress in the rare earth industry.

7. The application of humanoid robots in manufacturing, healthcare, services, security, and other fields continues to expand, and is expected to become a new growth point for rare earth downstream demand. This trend will become more pronounced in 2025 and the coming years.

Supply Side:

1. The rare earth mining quotas for 2025 have not yet been issued. Affected by export control policies and combined with the current market situation, it is expected that the mining quotas for 2025 will remain flat YoY.

2. The implementation of the "Administrative Measures for the Regulation of Total Rare Earth Mining and Smelting and Separation" and the "Administrative Measures for the Traceability of Rare Earth Product Information" will enhance the transparency of the circulation of rare earth products. Additionally, for the first time, overseas rare earth ores will be included in the smelting and separation quotas, facilitating macroeconomic regulation. The smelting and mining quotas will increase.

3. Affected by export controls, the exports of rare earth permanent magnets are restricted. However, driven by the increase in domestic end-use market demand, the production of NdFeB will increase, and the production of NdFeB in 2025 will increase slightly.

》Click to view the special report on the 2025 SMM (2nd) Rare Earth Industry Forum