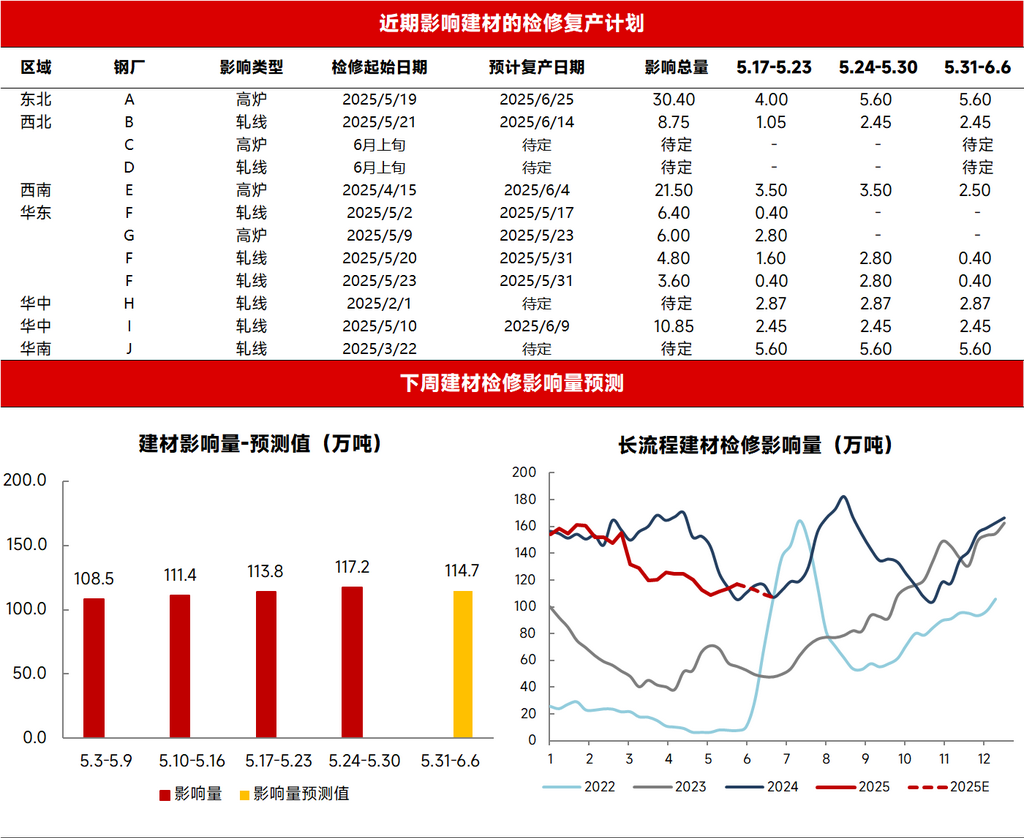

According to the SMM survey, the impact from maintenance of building materials continued to increase this week (May 24-30). Multiple steel mills extended their blast furnace and rolling line maintenance as scheduled. The impact from maintenance of building materials reached 1.172 million mt, up 34,000 mt WoW.

Source: SMM

Recently, as the Sino-US tariff trade fervor has faded and demand in the construction industry has continued to weaken, prices of raw materials and finished steel products have fallen to varying degrees. The decline in finished steel prices has outpaced that on the cost side, leading to a contraction in the production profit margin of rebar and affecting steel mills' production enthusiasm. According to the SMM survey, individual steel mills in south-west China have postponed their blast furnace maintenance and production resumption schedules, while some rolling lines in east China have remained shut down this week, resulting in a slight increase in the impact from maintenance of building materials this week.

Looking ahead, downstream demand is currently in the traditional transition phase between the "off-season" and "peak season". With the wheat harvest season starting in the north, construction progress in the industry has been slow, and purchasing pace has slowed down. It is expected that spot prices of building materials will remain under pressure in the short term. However, considering the approaching Dragon Boat Festival, it cannot be ruled out that there will be periodic stockpiling behavior in end-use demand, driving prices to stop falling and begin to rebound. Prices of iron ore and coke on the cost side may trend weaker, and it is expected that steel mills' gross margins will continue to fluctuate around 100 yuan. According to the SMM survey, most steel mills are maintaining normal production rhythms. Only two steel mills in north-west China plan to conduct blast furnace maintenance in June, leading to a decrease in iron output and the shutdown of building material rolling lines. Additionally, due to the long-term periodic shutdown of rolling lines at some steel mills in east China, it is expected that the impact from maintenance of building materials next week will not change significantly compared to this week.

Source: SMM

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)