SMM News on May 22:

Price Review:

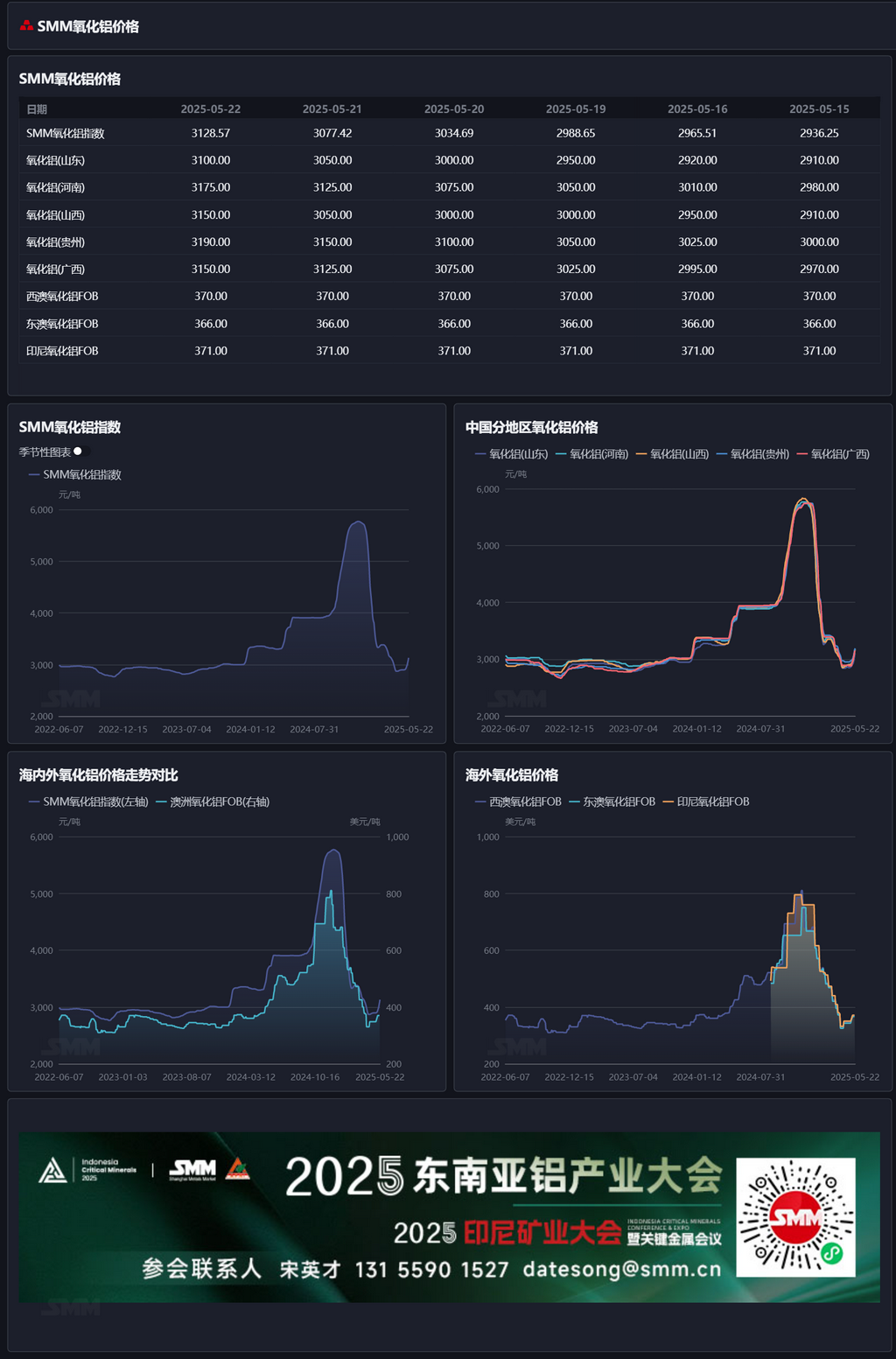

As of Thursday this week, the SMM alumina index stood at 3,128.57 yuan/mt, up 192.33 yuan/mt from last Thursday. In Shandong, prices were reported at 3,050-3,150 yuan/mt, up 190 yuan/mt from last Thursday; in Henan, prices were at 3,150-3,200 yuan/mt, up 195 yuan/mt from last Thursday; in Shanxi, prices were at 3,150-3,200 yuan/mt, up 220 yuan/mt from last Thursday; in Guangxi, prices were at 3,100-3,200 yuan/mt, up 180 yuan/mt from last Thursday; in Guizhou, prices were at 3,150-3,230 yuan/mt, up 190 yuan/mt from last Thursday; in Bayuquan, prices were at 3,210-3,290 yuan/mt.

Overseas Market:

As of May 22, 2025, the FOB Western Australia alumina price was $370/mt, with an ocean freight rate of $21.40/mt. The selling price of the USD/CNY exchange rate hovered around 7.22. This price translates to approximately 3,274 yuan/mt for the external selling price at major domestic ports, which is 146 yuan/mt higher than the domestic alumina price. The alumina import window remained closed. No new overseas spot alumina transactions were inquired about this week.

Domestic Market:

According to SMM data, as of Thursday this week, the total installed capacity of metallurgical-grade alumina nationwide was 109.22 million mt/year, with a total operating capacity of 85.21 million mt/year. The national weekly alumina operating rate increased by 0.99 percentage points WoW to 78.01%, mainly due to the completion of maintenance and production cuts at some enterprises, leading to a rebound in operating capacity. Specifically, the weekly alumina operating rate in Shandong remained unchanged from last week at 89.30%; in Shanxi, it decreased by 3.6 percentage points WoW to 72.40%; in Henan, it remained unchanged from last week at 52.50%; in Guangxi, it increased by 4.57 percentage points WoW to 89.44%.

During the period, spot alumina transaction prices rose significantly compared to the previous period. By region: some alumina was procured through tender by aluminum plants in Xinjiang, with delivery-to-factory prices around 3,400-3,450 yuan/mt; 4,000 mt of alumina was traded in Henan at 3,000-3,100 yuan/mt; 20,000 mt of alumina was traded in Shanxi at 3,150-3,200 yuan/mt; 5,000 mt of alumina was traded in Guangxi at 3,050-3,200 yuan/mt; 5,000 mt of alumina was traded in Guizhou at 3,150-3,230 yuan/mt.

Overall:

This week, some enterprises in north China underwent maintenance, while some alumina refineries in south China completed maintenance, leading to a rebound in operating capacity. On the whole, the national alumina operating capacity increased by 1.09 million mt MoW this week. In the near future, some new alumina enterprises are expected to conduct planned maintenance, while some enterprises are anticipated to resume their operating capacity after completing maintenance. Overall, the operating capacity is expected to continue to rebound slightly. Affected by the supply-side disruptions in the bauxite market, bauxite prices have risen, and the cost-supporting effect on alumina is expected to strengthen. Coupled with the fact that the short-term fundamentals have not shifted to a surplus situation, there is still upward momentum in prices. However, given the recovery in supply, the rise in alumina prices may encounter resistance, and alumina prices are expected to hold up well in the short term.