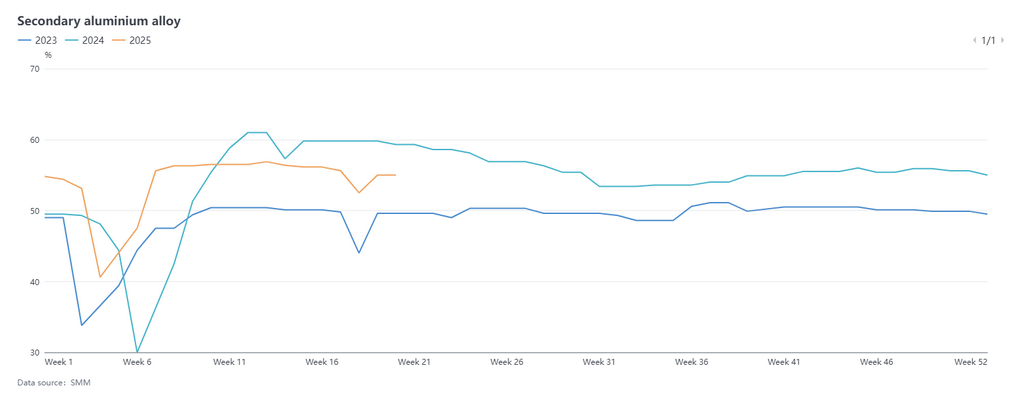

Secondary Aluminum Sector Operating Rate Stays Stable Amid Market Challenges

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM‘s internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or to learn more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

10 hours ago

Fed Governor Milan Pushes for Over 100 Basis Points Cut, Contradicts Barkin on Caution

Read More

Fed Governor Milan Pushes for Over 100 Basis Points Cut, Contradicts Barkin on Caution

Federal Reserve Governor Milan pointed out that it is necessary for the US Fed to cut interest rates by more than 100 basis points this year. At the same time, he is very much looking forward to the performance of Kevin Warsh as Fed Chairman. However, Richmond Fed President Barkin emphasized that monetary policy must remain cautious until inflation fully pulls back to the target level, thereby ensuring the stability of the labour market.

10 hours ago

10 hours ago

Democratic Senators Demand Delay in Fed Nomination Amid Criminal Investigation

Read More

Democratic Senators Demand Delay in Fed Nomination Amid Criminal Investigation

All 11 Democratic members of the US Senate Banking Committee jointly sent a letter to the committee's chairman, Tim Scott, requesting that all nomination processes for the prospective Fed Chairman, Kevin Warsh, be postponed until the criminal investigation into current Fed Chairman Powell and other board members is concluded. However, Scott stated that Warsh's confirmation was a done deal.

10 hours ago

10 hours ago

Fed to Keep Large Banks' Capital Levels Unchanged, Postpones Stress Test Reforms Until 2027

Read More

Fed to Keep Large Banks' Capital Levels Unchanged, Postpones Stress Test Reforms Until 2027

The US Fed has announced that it will maintain the capital levels of large banks unchanged during the upcoming stress test cycle (corresponding to the 2026 cycle). At the same time, the US Fed is planning multidimensional reforms to this annual test, aiming to enhance its transparency. The US Fed's Vice Chair for Supervision, Bowman, revealed that adjustments to the stress capital buffer requirements for large banks will be postponed until 2027. This move is intended to provide the US Fed with sufficient time to evaluate potential flaws that may be exposed in its testing models when assessing banks' financial conditions under simulated economic downturn scenarios.

10 hours ago

Related News

Fed Governor Milan Pushes for Over 100 Basis Points Cut, Contradicts Barkin on Caution

Feb 07, 2026 17:24

Democratic Senators Demand Delay in Fed Nomination Amid Criminal Investigation

Feb 07, 2026 17:23

Fed to Keep Large Banks' Capital Levels Unchanged, Postpones Stress Test Reforms Until 2027

Feb 07, 2026 17:23

Toyota Plans to Boost Hybrid and PHEV Production to 6.7M Units by 2028

Feb 07, 2026 17:22