》Check SMM lead product quotes, data, and market analysis

》Subscribe to view historical prices of SMM metal spot cargo

SMM News on May 7:

Currently, the market is still in the off-season for lead-acid battery consumption. Recyclers indicate that the collection volume at stores is low, and there is fierce competition among peers. Secondary lead smelters report poor arrivals of scrap batteries, making it difficult to lower purchase quotes. Currently, the mainstream purchase price for scrap e-bike lead-acid batteries (excluding tax) ranges from 9,900 to 10,100 yuan/mt, with daily arrivals of a dozen trucks, resulting in relatively tight raw material inventory.

Additionally, downstream lead-acid battery producers have high lead ingot inventory, with raw material inventory lasting over 10 days being common. Coupled with limited sales orders for finished batteries, their willingness to purchase is low. This has led to difficulties in selling lead ingots, with primary lead being sold at a discount to the SMM 1# lead average price ex-factory, and secondary refined lead being forced to offer discounted quotes. Due to high costs, loss pressures have made secondary lead producers reluctant to sell, with few offering quotes.

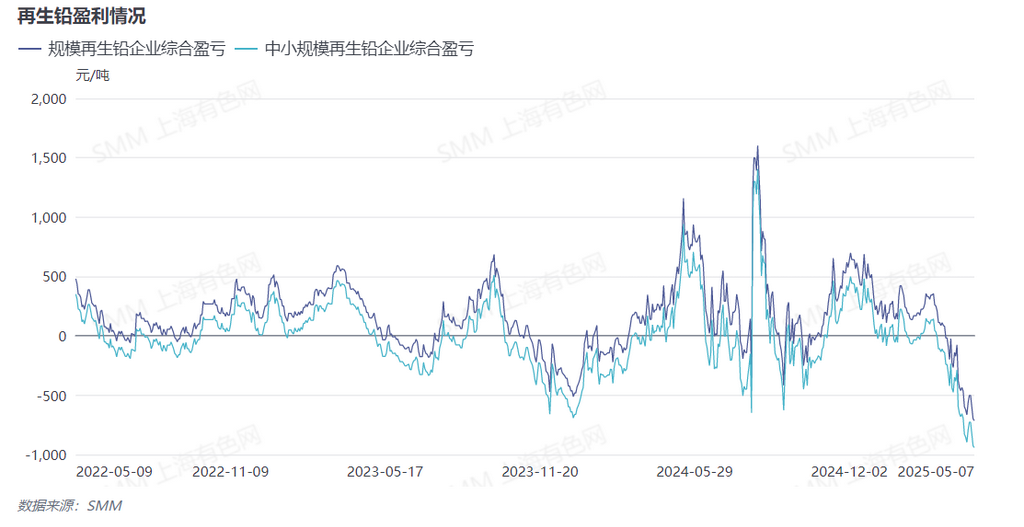

According to multiple secondary lead smelters, the current loss per ton of secondary refined lead is as high as 600-800 yuan/mt. Under these market conditions, production enthusiasm among enterprises is low, with many planning maintenance and shutdowns in May. Below are the planned details compiled by SMM for reference only.

From the chart above, it can be seen that due to unsatisfactory raw material arrivals, many enterprises are expressing expectations of production cuts. Despite plans for new capacity to come online in May, overall, it is still difficult to reverse the established trend of declining production in May.