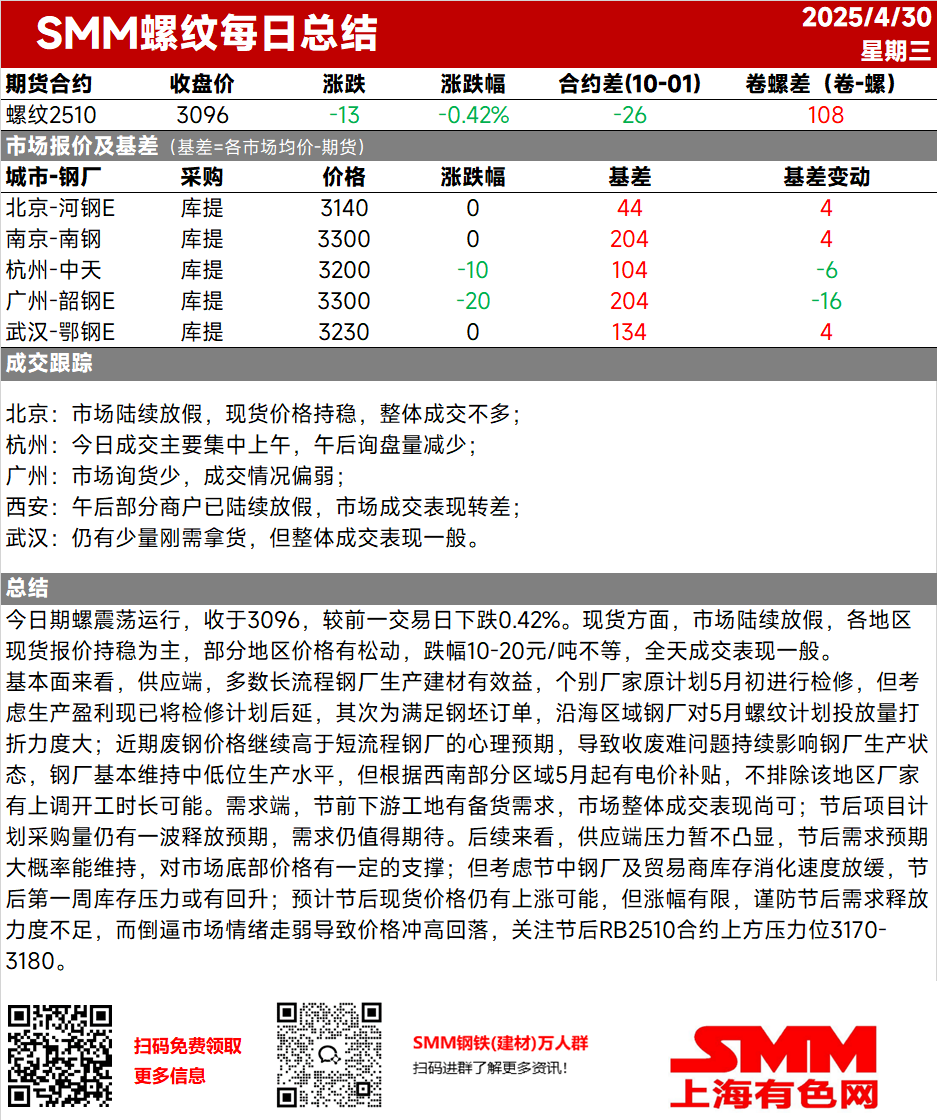

Today, rebar futures experienced volatile trading, closing at 3096, down 0.42% from the previous trading day. On the spot cargo side, as the market gradually entered the holiday period, spot cargo quotes in various regions were largely stable, with prices in some areas showing signs of loosening, with declines ranging from 10-20 yuan/mt. Trading volume throughout the day was moderate. From a fundamental perspective, on the supply side, most blast furnace steel mills found it profitable to produce construction steel. A few manufacturers had originally planned maintenance for early May, but considering production profitability, they have postponed their maintenance plans. Additionally, to meet billet orders, steel mills in coastal regions have significantly reduced their planned rebar output for May. Recently, steel scrap prices have continued to exceed the psychological expectations of EAF steel mills, leading to persistent difficulties in scrap collection, which has continued to affect the production status of steel mills. Steel mills have generally maintained a medium-to-low production level. However, given the electricity price subsidies expected in some regions of Southwest China from May onwards, it cannot be ruled out that manufacturers in these regions may increase their operating hours. On the demand side, downstream construction sites had stockpiling needs before the holiday, and overall trading volume in the market was moderate. There is still an expected wave of procurement volume planned for projects after the holiday, and demand remains promising. Looking ahead, supply-side pressure is not prominent for the time being, and demand expectations after the holiday are likely to be sustained, providing some support for the bottom price of the market. However, considering the slower digestion of inventory by steel mills and traders during the holiday, inventory pressure may rebound in the first week after the holiday. It is expected that spot cargo prices may still rise after the holiday, but the increase will be limited. Caution should be exercised against insufficient demand release after the holiday, which could force market sentiment to weaken, leading to a situation where prices jump initially and then pull back. Attention should be paid to the upper resistance levels of 3170-3180 for the RB2510 contract after the holiday.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)