》View SMM Metal Quotes, Data, and Market Analysis

》Order and View SMM Metal Spot Historical Price Trends

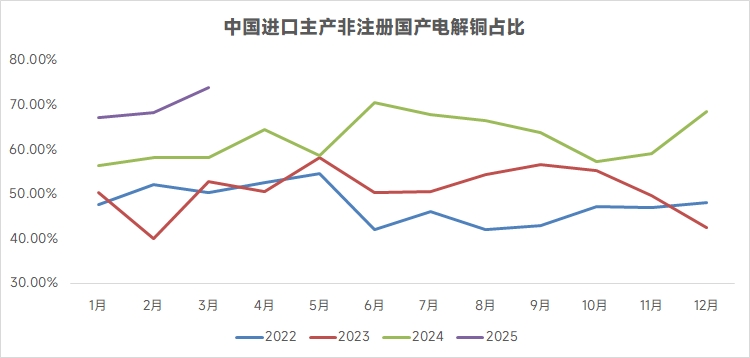

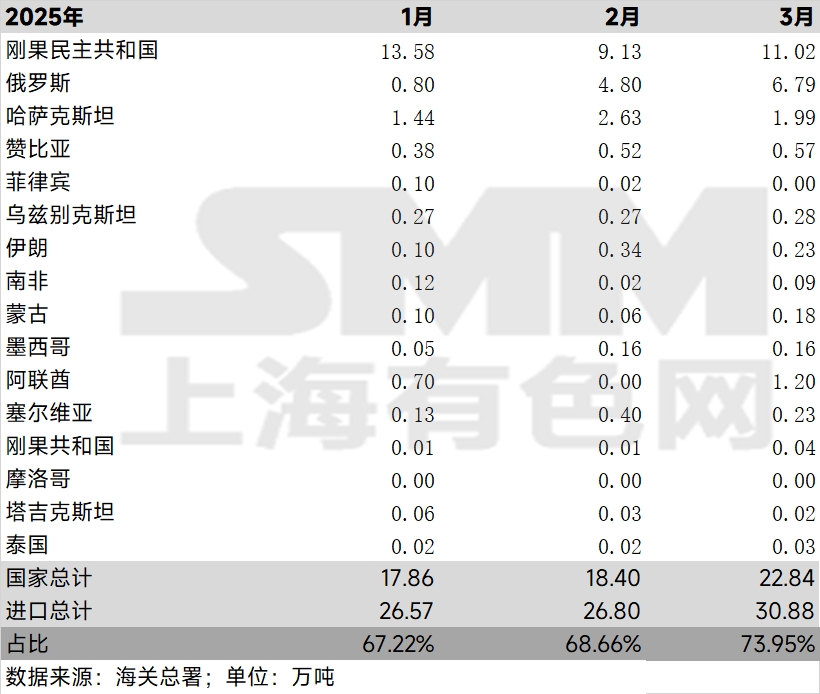

According to customs data, China's copper cathode imports in March 2025 reached 308,800 mt. SMM compiled data shows that imports from major non-registered copper cathode producing countries amounted to 228,400 mt, accounting for 73.95% of the total, the highest proportion since 2022.

By country, the highest import proportions in March were from the DRC and Russia, followed by Kazakhstan and the UAE. Notably, Russia's imports exceeded 60,000 mt in March. SMM learned that a significant amount of Russian copper will continue to flow into China, though the volume is not expected to exceed 60,000 mt per month. Future import volumes are not expected to grow, and the proportion of non-registered imports is likely to remain around 70%.

Non-registered imports continue to increase, yet their prices have been rising in the domestic trade market. What is the reason?

As the US siphons global copper cathode, shipments from Chile, Peru, and other countries to China have decreased, with a notable reduction in registered SX-EW brands arriving in China. Non-registered sources from Africa and Russia have served as substitutes. Meanwhile, secondary copper supply is tight, and as copper prices rise, downstream users favor lower-priced non-registered sources. Continued destocking of non-registered sources has driven their prices higher.

Observing the ongoing convergence of the price spread between non-registered and SX-EW copper, it has a guiding effect on the price difference between copper cathode and copper scrap. When the price spread between non-registered and SX-EW copper shows a trend of convergence/divergence, the price difference between copper cathode and copper scrap will also tend to converge/diverge; this guidance can be observed one week in advance.

》View SMM Metal Industry Chain Database

![Weekend Total Social Copper Inventory Increased, Regional Trends Diverged [SMM weekly data]](https://imgqn.smm.cn/usercenter/TlzAr20251217171709.jpg)

![Humanoid Robot and High-Efficiency Motor Demand Expectations Catalyze, Motor Sector Strengthens, Jiangxi Special Electric Motor Hits Daily Limit [SMM Quick News]](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)