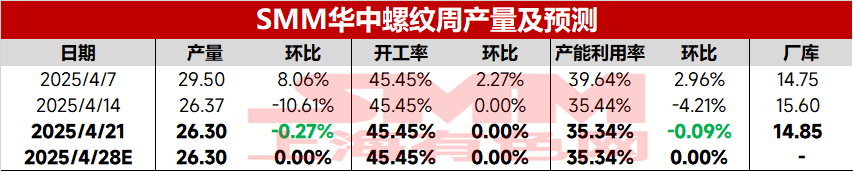

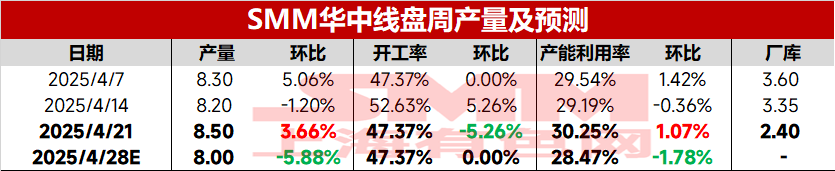

Operating Rate and Forecast of Building Material Production Lines in Central China Steel Mills

During the survey period (April 15-April 21), the capacity utilization rate of rebar rolling lines in Central China decreased slightly, while the operating rate of wire rod rolling lines declined, but the capacity utilization rate increased slightly.

Data source: SMM

During the survey period (April 15-April 21), the capacity utilization rate of rebar rolling lines in Central China decreased slightly.

Specifically, some electric furnace mills in Hubei extended their operating hours, but due to insufficient billets in some steel mills in Hunan, production was reduced, leading to a slight decline in rebar supply. In terms of in-plant inventory, as futures fluctuated upward, market sentiment improved, and agents increased purchases, resulting in overall destocking.

Next week, rebar production in Central China is expected to remain flat compared to this period, mainly because steel mills are still profitable, and there are no temporary maintenance plans in the short term, keeping the capacity utilization rate relatively stable.

Data source: SMM

During the survey period (April 15-April 21), the operating rate of wire rod rolling lines in Central China declined, but the capacity utilization rate increased slightly.

Specifically, some steel mills in Hubei adjusted their production structure on a weekly basis, temporarily halting wire rod rolling lines starting from the 19th. However, the actual operating days in the previous period were shorter than this period, leading to an increase in capacity utilization and a decline in the operating rate. In terms of in-plant inventory, overall inventory continued to decline due to active destocking by steel mills.

Next period, wire rod production in Central China is expected to decrease, mainly because steel mills under maintenance in Hubei have no production resumption plans, and the capacity utilization rate will shift from increase to decrease.

Click to view the SMM Metal Industry Chain Database

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)