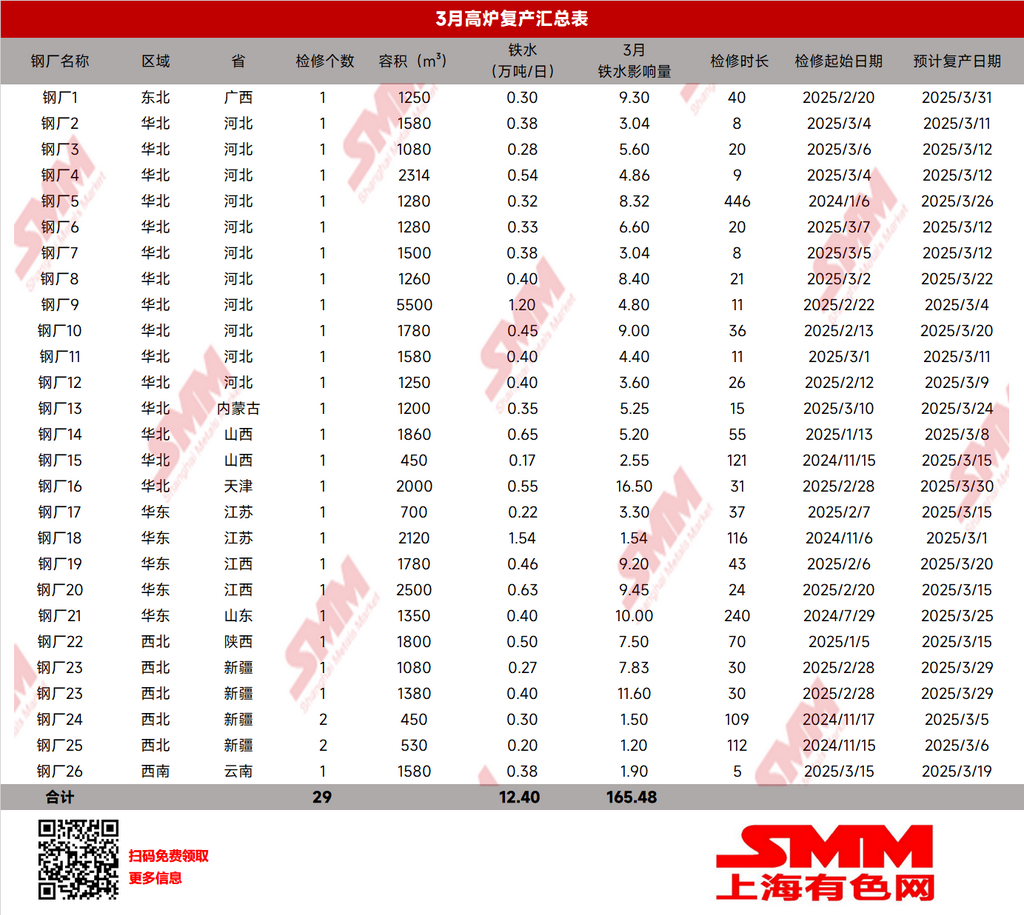

According to the SMM survey data, 17 blast furnaces underwent maintenance in March, resulting in a daily pig iron production reduction of 67,300 mt. The concentrated maintenance of blast furnaces mainly occurred in north China. Meanwhile, 29 blast furnaces resumed production, increasing daily pig iron production by 124,000 mt. The resumption of production was primarily concentrated in north and north-west China. Due to March having three more days than February, the impact from maintenance on blast furnaces in March showed little change MoM. SMM survey data indicated that blast furnace maintenance in March led to a net reduction of 6.59 million mt in pig iron production, only 20,000 mt higher than in February.

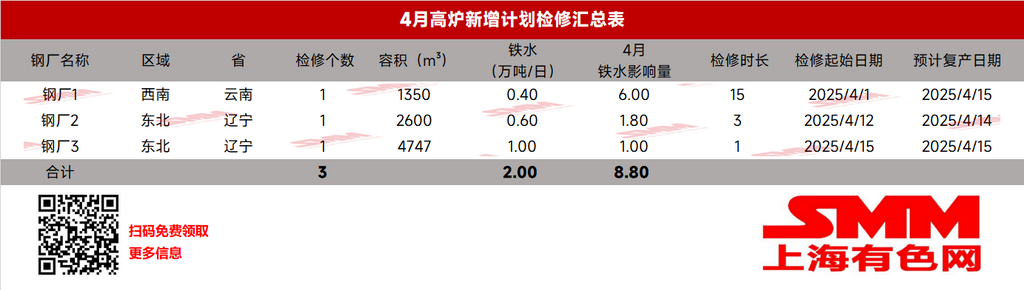

According to the SMM survey, as of now, three additional blast furnaces are scheduled for maintenance in April, reducing daily pig iron production by 20,000 mt. In contrast, 15 blast furnaces are planned to resume production, increasing daily pig iron production by 78,700 mt. Based on current data, the total pig iron production affected by blast furnace maintenance in April is expected to be 4.242 million mt, a significant decrease of 2.3437 million mt compared to March. Pig iron production in April is projected to continue growing. According to SMM's daily pig iron production estimate, the daily pig iron production of sample steel mills is expected to reach 2.463 million mt on April 30, up approximately 50,000 mt MoM.

April is traditionally a peak demand season, with current steel mill inventories relatively low YoY and production enthusiasm high. Although steel mill profits have slightly narrowed, they remain sustainable. Therefore, SMM expects limited blast furnace maintenance plans in April, with a focus on active resumption of production. SMM will continue to track the situation weekly.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)