SMM Alumina Morning Comment 4.1

Futures market: During the night session, the most-traded alumina 2505 contract opened at 2,937 yuan/mt, with a high of 2,957 yuan/mt, a low of 2,921 yuan/mt, and closed at 2,950 yuan/mt, up 14 yuan/mt, or 0.47%, with an open interest of 201,000 lots.

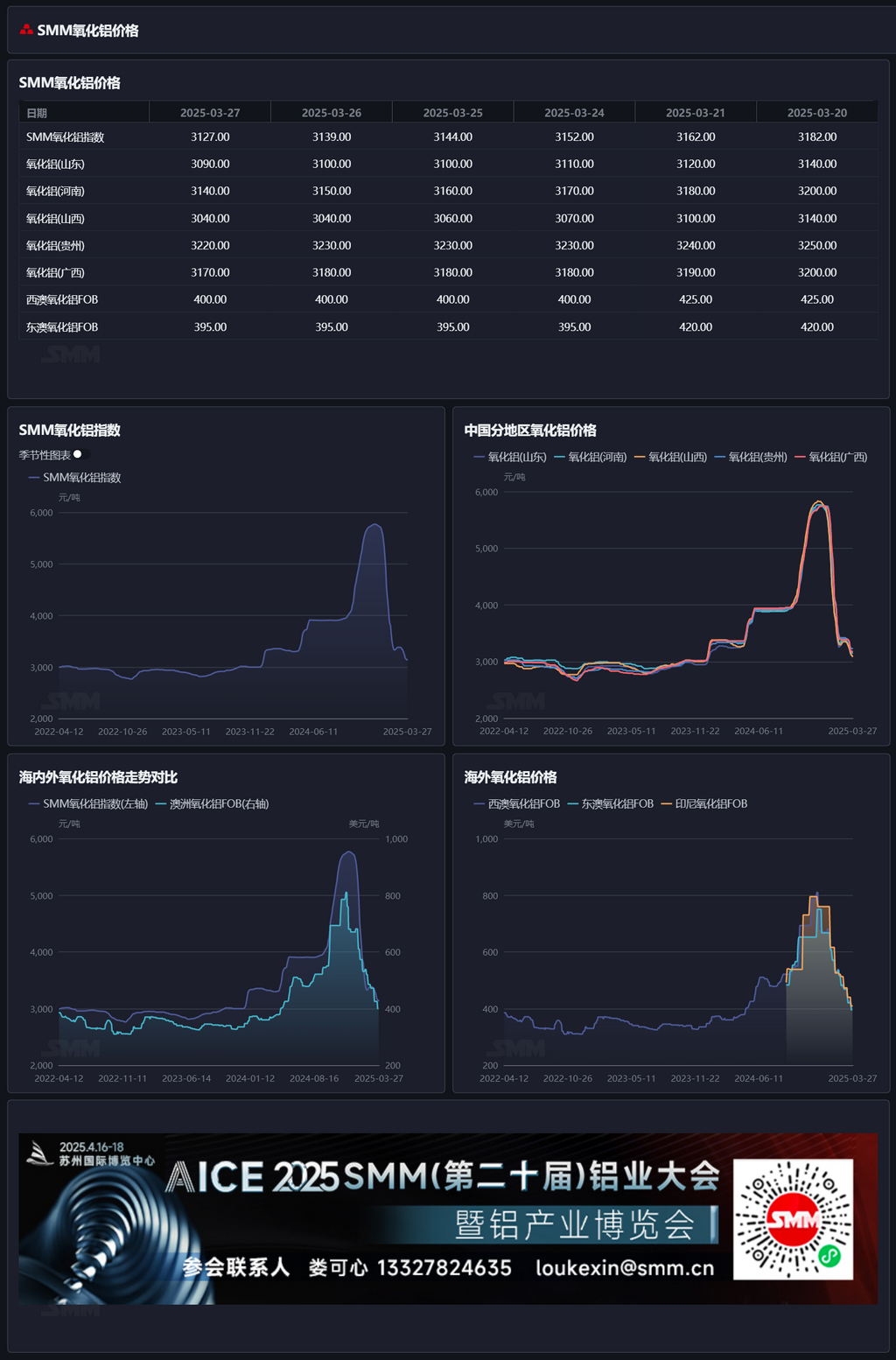

Ore side: As of March 31, the SMM imported bauxite index stood at $93.1/mt, flat from the previous trading day. The SMM Guinea bauxite CIF average was $91/mt, flat from the previous trading day. The SMM Australia low-temperature bauxite CIF average was $87/mt, flat from the previous trading day. The SMM Australia high-temperature bauxite CIF average was $81/mt, flat from the previous trading day.

Industry news:

- According to SMM, starting from April 1, a large alumina refinery in Shandong adjusted the purchase price of 32% ion-exchange membrane liquid caustic soda, lowering it by 15 yuan/mt from the base price of 810 yuan/mt. The ex-factory price under the two-ticket system is 795 yuan/mt (converted to 100% concentration, approximately 2,484 yuan/mt).

- It is reported that PT Indonesia Asahan Aluminium (Inalum), a state-owned aluminum producer in Indonesia, plans to start the second phase of construction of the Mempawah metallurgical-grade alumina refinery (SGAR) in West Kalimantan in 2025. Currently, the company expects to complete the feasibility study and final investment decision (FID) within 2024, as the basis for subsequent engineering, procurement, and construction (EPC) work. Inalum and the state-owned miner PT Aneka Tambang (Antam) have completed the first phase of the project, which is expected to achieve full production by the end of Q1 2025, with an annual capacity of 1 million mt. After the completion of the second phase, the total capacity will double to 2 million mt per year.

- On March 26, the SPIC Guinea Alumina Development Project (Phase II) alumina project was fully launched at 11:00 local time in Guinea (19:00 Beijing time). The project includes bauxite mining in the northern mining area, a 1.2 million mt/year alumina plant, and its supporting facilities.

- On March 26, the finished product construction and installation project of the Guangxi Fangchenggang Port Ecological Aluminum Industry Chain Project, undertaken by Minmetals 23rd Metallurgical Construction Co., Ltd., officially commenced. The project plans to build two 1.2 million mt/year alumina production lines, with a supporting red mud comprehensive utilization system, using the low-temperature, low-alkali concentration Bayer process. As a key project of the Western Land-Sea New Corridor, upon completion, it will form a complete industry chain of "overseas ore sources - alumina - aluminum-based new materials," which is of significant strategic importance for optimizing China's aluminum industry layout and improving the level of bulk solid waste resource utilization.

Basis report: According to SMM data, as of March 31, the SMM alumina index was at a premium of 146 yuan/mt against the most-traded contract's latest transaction price at 11:30.

Warrant report: As of March 31, the total registered volume of alumina warrants increased by 601 mt to 299,100 mt compared to the previous trading day. The total registered volume of alumina warrants in Shandong remained flat at 4,513 mt, in Henan at 25,800 mt, in Guangxi at 49,800 mt, in Gansu at 22,500 mt, and in Xinjiang increased by 601 mt to 196,400 mt.

Overseas market: As of March 31, 2025, the FOB alumina price in Western Australia was $377/mt, with an ocean freight rate of $21.40/mt, and the USD/CNY exchange rate selling price was around 7.26. This price translates to a domestic mainstream port selling price of approximately 3,092 yuan/mt, which is 258 yuan/mt higher than the domestic alumina price, keeping the alumina import window closed. Based on the latest FOB transaction price of $368/mt in Eastern Australia, the domestic mainstream port selling price is around 3,300 yuan/mt, only less than 200 yuan/mt higher than the SMM alumina price index. If overseas alumina prices further decrease and the rate of decrease exceeds that of domestic prices, the alumina import window may gradually open. On the export side, based on the latest spot transaction price of alumina in Shandong, the domestic alumina export cost is around $450/mt, higher than the overseas spot alumina price, keeping the export window closed.

Summary: Last week, the weekly operating rate of alumina was lowered again, with the national total operating capacity of metallurgical alumina reduced to 87.3 million mt/year, and the weekly operating capacity decreased by 700,000 mt/year MoM. However, the overall supply surplus in the alumina market has not yet reversed. According to SMM data, as of last Thursday, the total operating capacity of domestic aluminum was 43.88 million mt/year, translating to an alumina demand operating capacity of around 84.47 million mt/year, with theoretical demand increasing slightly but still below actual operating levels. On the supply side, domestic bauxite supply remains low, with limited increments. The increase in imported bauxite supply has driven the total domestic bauxite supply, and the supply-demand fundamentals of bauxite may become more relaxed than before, with bauxite prices likely to remain under pressure in the short term. Meanwhile, downstream aluminum plants reported that alumina procurement is mainly based on long-term contracts, and some plants that have stockpiled for winter are planning to actively reduce inventory. According to SMM statistics, alumina raw material inventory at aluminum plants decreased by 44,000 mt WoW. In the short term, alumina circulating supply is expected to remain relatively loose, and alumina prices may continue to operate under pressure. Subsequent attention should be paid to changes in alumina operating capacity.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]