》View SMM Silicon Product Quotes

》Order and View SMM Metal Spot Historical Price Trends

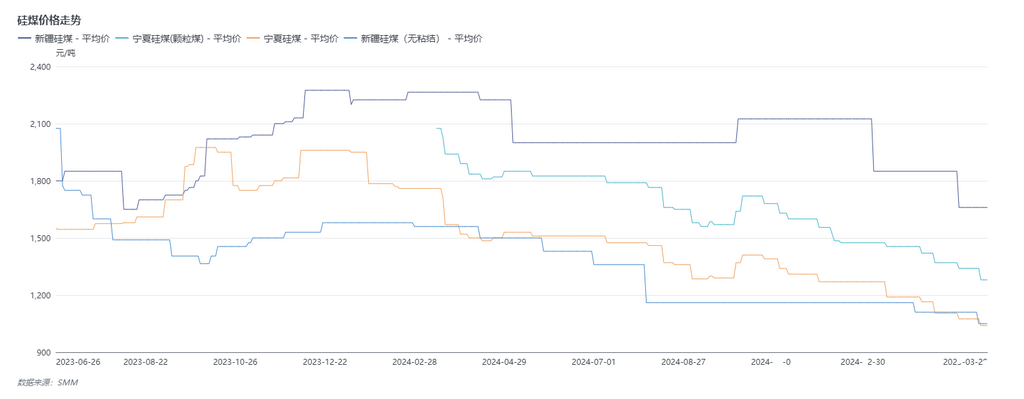

The silicon coal market has seen continuous price declines recently, with prices in many regions loosening and dropping throughout March. Driven by the already weak coal market environment this year, the demand for silicon coal has also been less than ideal. Under the dual impact of these weaknesses, silicon coal prices continue to fluctuate downward.

The recent price drop in silicon coal is more influenced by the weak market conditions of downstream silicon metal.

First, the price of the fifth silicon coal in Shaanxi, which has long been below 1,000 yuan, has further declined recently despite already being at a low level. The current mainstream market price has reached 800-900 yuan/mt, with some higher moisture content and slightly exceeding standards even reaching 740-750 yuan/mt. Under the impact of Shaanxi's low silicon prices, the non-caking silicon coal in Xinjiang, as a competing product, has also seen price adjustments recently, despite securing orders from major factories within the region due to transportation advantages. This price adjustment is the second in 2025, with the price of Xinjiang's non-caking silicon coal dropping to 1,050 yuan/mt.

In addition to the decline in non-caking silicon coal prices, the caking silicon coal in Ningxia has also seen price loosening recently. Ningxia's silicon coal mainly targets silicon factories in south-west China. However, due to the persistently weak silicon metal market this year, the resumption of production during the rainy season in south-west China has not been very active, leading to a significant lack of enthusiasm for raw material restocking this year. The weak downstream demand combined with the weak coal market environment has led to multiple price drops for silicon coal in Ningxia this year. Currently, the price of mixed coal from leading manufacturers has dropped to 1,030 yuan/mt, and granular silicon coal has dropped to 1,180 yuan/mt.

Currently, there are no significant signs of recovery in the downstream silicon metal market. Under the weak market conditions of downstream silicon factories, although the price of raw material silicon coal has fallen to a low level in recent years, there may still be some downside room.

![[SMM Iron & Steel] US Raw Steel Production Rises 8.8% YoY in Week Ending May 30, 2026](https://imgqn.smm.cn/usercenter/gmcdk20251217171720.jpg)