》View SMM Aluminum Product Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

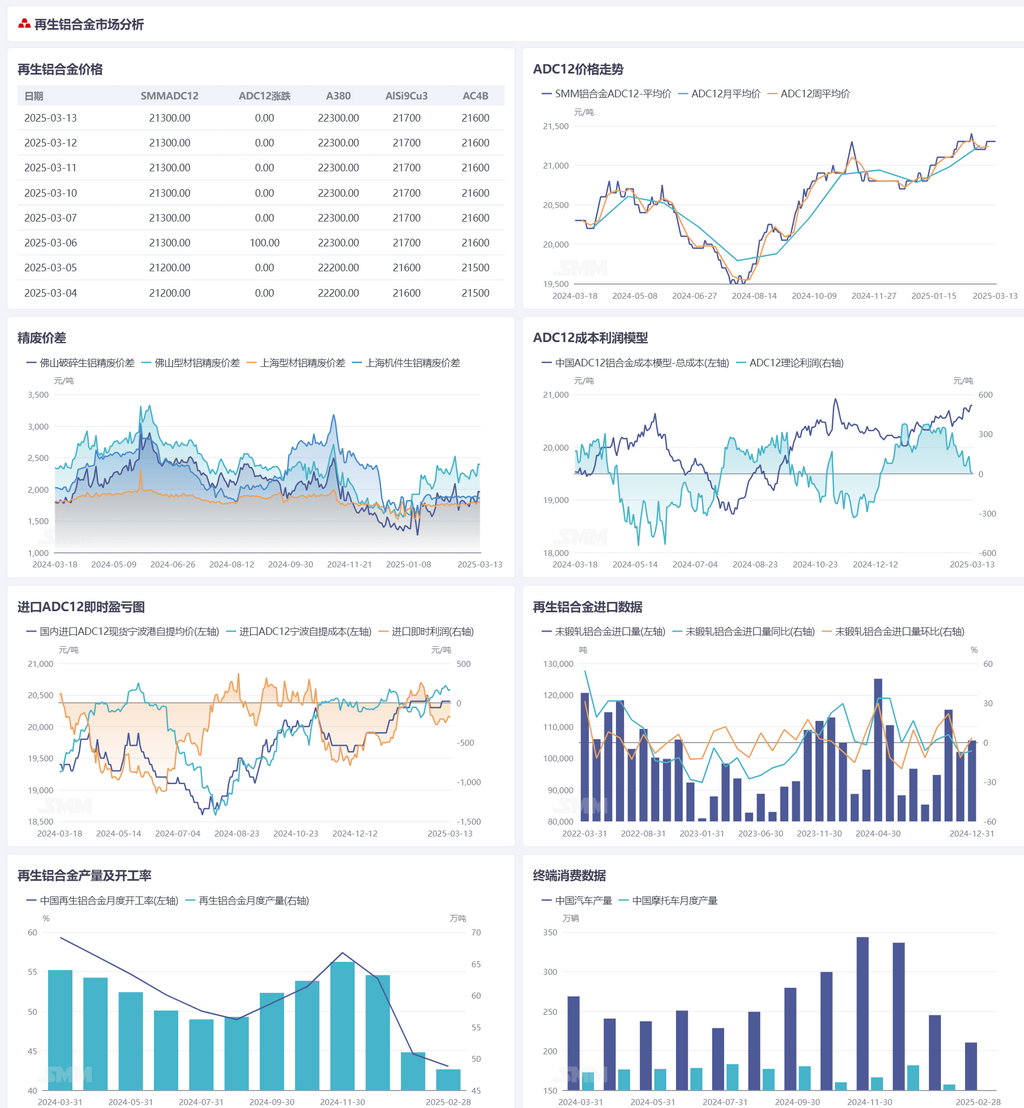

Secondary Aluminum Raw Materials:

This week, aluminum scrap prices fluctuated slightly along with primary aluminum, with the price center remaining high. The market mainly purchased on demand, and the price difference between primary metal and scrap widened. In terms of aluminum scrap supply, the operating rate of aluminum processing enterprises continued to recover, coupled with the stimulus of peak season demand recovery, leading to a short-term rebound in domestic new scrap supply. Regarding overseas aluminum scrap supply, the pattern of LME outperforming SHFE for primary aluminum remained unchanged, with overseas aluminum scrap prices staying relatively high. Upstream and downstream enthusiasm was generally moderate, making short-term supply increases unlikely. As of this Thursday, SMM A00 spot price was 20,910 yuan/mt, up 110 yuan/mt from last Thursday; Shanghai aluminum tense scrap price was 19,042 yuan/mt, up 109 yuan/mt from last Thursday; the price difference between Shanghai aluminum tense scrap and A00 aluminum widened by 1 yuan/mt from last Thursday to 1,868 yuan/mt; the price difference between Foshan aluminum extrusion scrap and A00 aluminum widened by 100 yuan/mt from last Thursday to 2,391 yuan/mt. In the short term, the domestic aluminum scrap market sees increases in both supply and demand. However, as aluminum scrap prices remain high, downstream demand has not grown significantly, leading to limited price fluctuations and a widening price difference between primary metal and scrap. The price difference is expected to fluctuate next week.

Secondary Aluminum Alloy:

This week, secondary aluminum alloy prices struggled to catch up. As of March 13, SMM ADC12 prices remained flat WoW at 21,300 yuan/mt. On the cost side, with the continued increase in market recycled material supply, raw material procurement pressure on secondary aluminum plants eased somewhat. However, due to the high-level fluctuations in primary aluminum prices, aluminum scrap prices generally rose, causing cost increases to outpace those of finished alloy ingots, further compressing theoretical profit margins for the industry. On the demand side, weak downstream consumption recovery remains the main constraint on current price increases. Die-casting enterprises saw limited order growth, while high aluminum prices led to cautious downstream purchasing sentiment, resulting in limited actual transactions. Supply side, secondary aluminum plant operating rates remained stable, but insufficient orders led to increased market supply, exacerbating price competition due to supply surplus. On the import side, overseas ADC12 prices remained high at $2,480-2,520/mt, with immediate import losses hovering around 200 yuan/mt. Overall, insufficient demand has caused ADC12 prices to encounter resistance in moving upward. Looking ahead to mid-to-late March, secondary aluminum prices are expected to continue a sideways movement. If end-use consumption recovery falls short of expectations and raw material supply remains ample, ADC12 prices may face downward pressure. In the near term, attention should focus on raw material circulation and the implementation effects of consumption-boosting policies.