》View SMM Lead Product Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to View the SMM Database

SMM, March 7:

Recently, lead prices have finally broken free from the rangebound fluctuations caused by the tug-of-war between bulls and bears. The weak performance of the US dollar index has driven a broad increase in base metals, coupled with the positive impact of domestic macro consumption policies, pushing the operating center of SHFE lead gradually upward. Additionally, multiple provinces and cities in north China have issued heavy pollution weather alerts, with secondary lead smelters in regions such as Shandong and Henan halting production, further supporting the rise in lead prices.

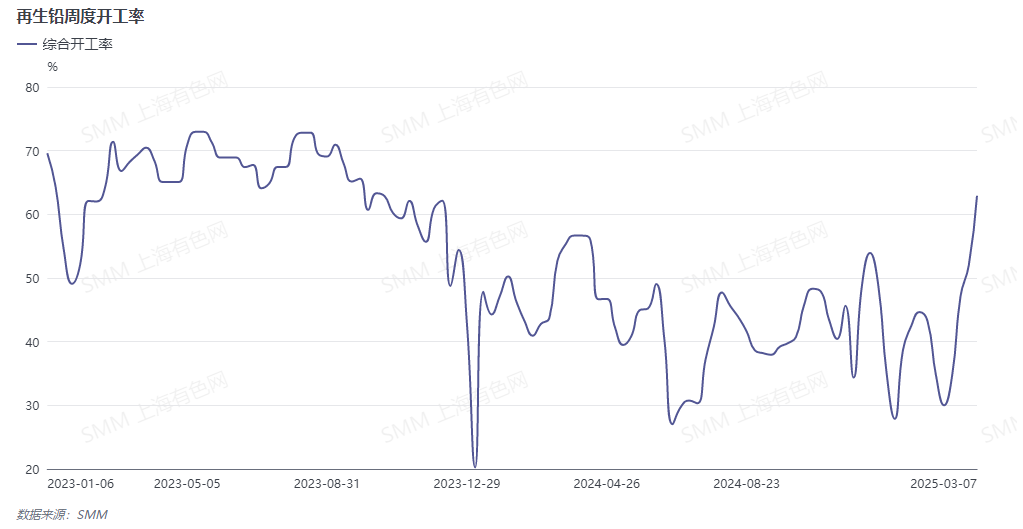

The resumption of production at secondary lead enterprises has entered a fever pitch. As of March 7, 2025, the weekly operating rate surveyed by SMM reached a one-and-a-half-year high of 62.91%.

After the February holiday, lead prices performed poorly, and recyclers exhibited a sentiment of panic selling due to fears of price declines. Meanwhile, most smelters had not yet resumed production, leaving those in operation with relatively ample raw material inventories. Following a wave of concentrated production resumption and amid the off-season for lead-acid battery scrapping, raw material inventories have significantly declined after more than half a month of consumption. Recyclers have shifted to a sentiment of holding back sales in anticipation of price increases, leading to a gradual reduction in arrivals at smelters.

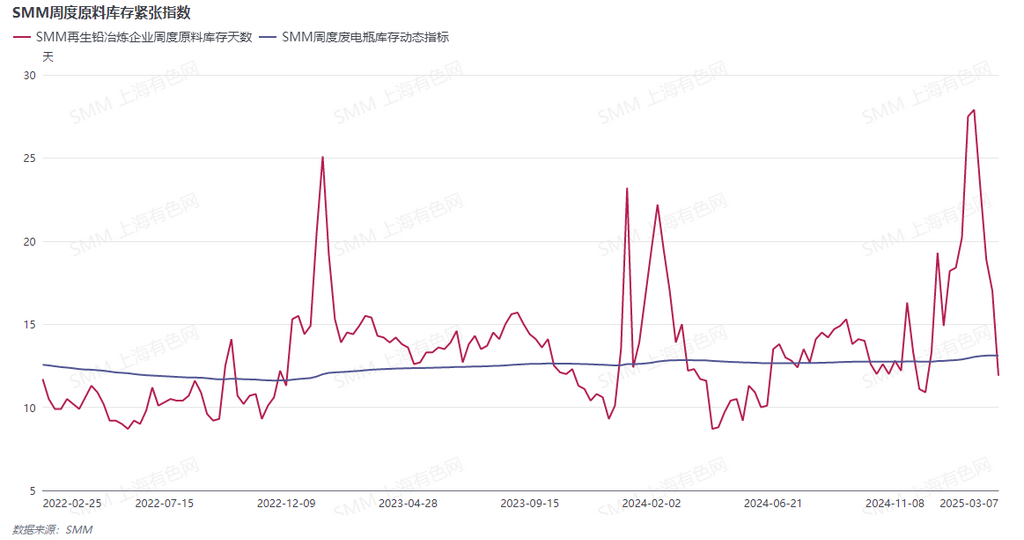

From the perspective of weekly days of raw material inventories at smelters, the current level is below the average. However, smelters have shown little willingness to restock by raising procurement prices for scrap batteries. The reason lies in their bearish expectations for lead prices in late March.

Currently, large-scale restocking has not occurred for three reasons: first, to avoid the devaluation of excessively high raw material inventories; second, to maintain existing profit margins; and third, in anticipation that recyclers will exhibit panic selling sentiment after lead prices decline, allowing smelters to restock at lower prices.

On the recycler side, despite being in the off-season for scrapping, the current sentiment of holding back sales in anticipation of price increases has led to a daily accumulation of scrap battery inventories, significantly tying up funds.

In this tug-of-war, smelters, facing continuously declining raw material inventories amid such high operating rates, must decide whether to implement production cuts or raise raw material procurement prices. Recyclers, on the other hand, face the pressure of deciding whether to sell promptly at market prices or continue holding back inventory in anticipation of price increases. Which side will concede first? Stay tuned for next week's SMM survey for more insights.