SMM, February 28

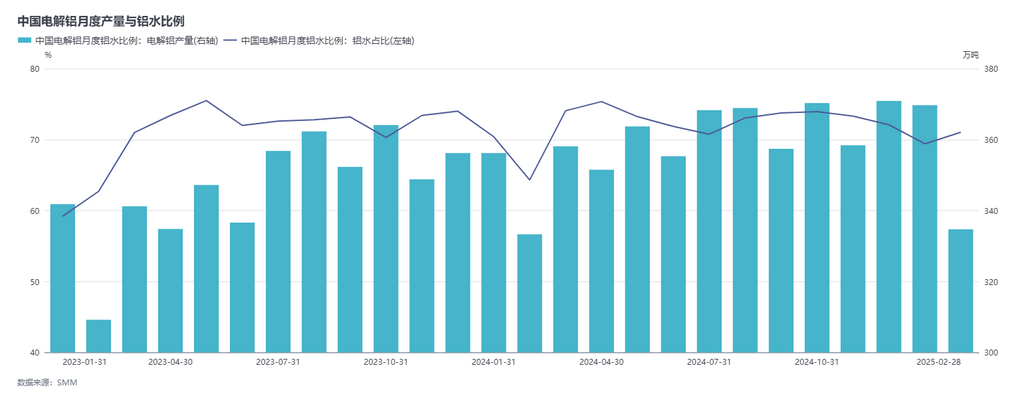

— According to SMM data, China's metallurgical-grade alumina production in February 2025 (28 days) decreased by 8.5% MoM but was up 10.4% YoY. As of February 28, China's existing metallurgical-grade alumina capacity stood at approximately 105.02 million mt, with operating capacity up 0.3% MoM and an operating rate of 86.1%. During the month, domestic alumina operating capacity showed mixed changes. On the new capacity side, production from previously commissioned capacity in Shandong supported this month's operating capacity and production. On the production cuts side, some alumina producers conducted maintenance due to a sharp decline in alumina prices while ore prices remained high, leading to a pullback in the operating rate. Currently, no large-scale production cuts are expected. In the short term, the alumina spot market is expected to remain in surplus, with prices likely to fluctuate around the cost line. Additionally, recent frequent news about domestic alumina exports suggests that China is expected to maintain a net export position.

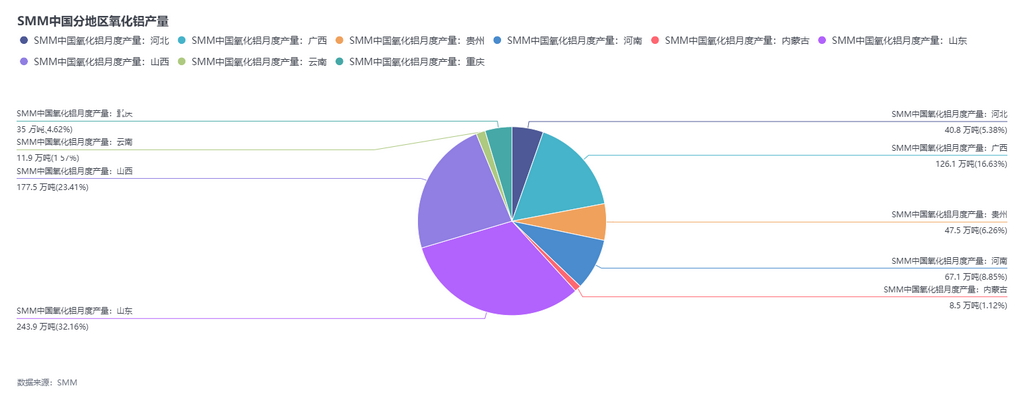

Forecast for Next Month: Feedback from multiple alumina refineries indicates adjustments in operating capacity in March. Apart from a capacity swap between old and new facilities by a company in Shandong, most adjustments involve short-term maintenance. Furthermore, new capacity in Guangxi is nearing commissioning, though the exact timeline remains uncertain. SMM will continue to monitor the situation. It is expected that China's metallurgical-grade alumina operating capacity in March will reach 90.03 million mt/year. Recently, demand for alumina exports and transfer to delivery warehouse has increased. Despite a significant pullback in alumina profits, the industry has not seen substantial production cuts. Market expectations suggest that additional alumina capacity will gradually come online, keeping domestic alumina supply pressure relatively small. Continuous attention is needed on changes in alumina capacity and export demand.

Forecast for Next Month: Feedback from multiple alumina refineries indicates adjustments in operating capacity in March. Apart from a capacity swap between old and new facilities by a company in Shandong, most adjustments involve short-term maintenance. Furthermore, new capacity in Guangxi is nearing commissioning, though the exact timeline remains uncertain. SMM will continue to monitor the situation. It is expected that China's metallurgical-grade alumina operating capacity in March will reach 90.03 million mt/year. Recently, demand for alumina exports and transfer to delivery warehouse has increased. Despite a significant pullback in alumina profits, the industry has not seen substantial production cuts. Market expectations suggest that additional alumina capacity will gradually come online, keeping domestic alumina supply pressure relatively small. Continuous attention is needed on changes in alumina capacity and export demand.

![[SMM Analysis] H1 2026 Overseas Secondary Aluminum Market Review & H2 Outlook: Supply Eases, Demand Leads](https://imgqn.smm.cn/production/admin/votes/imageslvDRc20240314085754.png)

![Geopolitical Conflicts Coupled with Inventory Destocking Drive SHFE and LME Aluminum to Drift Higher Short-Term [SMM Aluminum Morning Briefing]](https://imgqn.smm.cn/usercenter/yOYEC20251217171653.jpg)