This week, the stainless steel market exhibited a relatively active trend. Electronic trading prices remained stable with an upward movement, injecting positive signals into the market. Spot prices also saw a slight increase, and the trading atmosphere in the downstream market improved slightly compared to before, indicating a gradual recovery in market vitality.

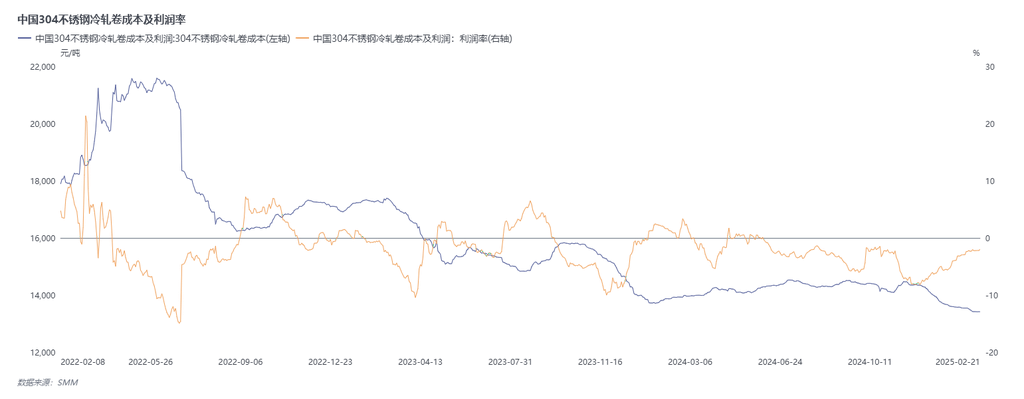

From the raw material perspective, price fluctuations of key raw materials such as high-grade NPI, imported nickel plates, and stainless steel scrap have a significant impact on stainless steel production costs. Among them, the freight-inclusive price of high-grade NPI approached 1,000 yuan/mt, while the price of imported nickel plates was 12,500 yuan/mt. These raw materials account for a large proportion of the total cost. Additionally, stainless steel production costs also include high-carbon ferrochrome costs, costs of other elements, smelting process costs, hot rolling process costs, pickling process costs, cold rolling process costs, as well as equipment depreciation costs and capital occupation costs. Taking cold-rolled products as an example, the full cost reached 14,800 yuan/mt, comprehensively reflecting the combined expenses of production, transportation, and other aspects.

From a long-term trend perspective, the two exhibit a clear negative correlation. As shown in the chart curves, when costs are at a high level, profit margins are often low or even negative. Taking data from February 21, 2025, as an example, the market price of 304/2B mill edge coils was 13,650 yuan/mt, while the cash cost was 14,043.98 yuan/mt, and the full cost was as high as 14,838.98 yuan/mt. This resulted in a profit value (cash cost) of -393.98 yuan/mt and a profit value (full cost) of -1,188.98 yuan/mt, with a profit margin (cash) of -2.81% and a profit margin (full) of -8.01%, fully indicating that the product is currently in a loss-making state where costs exceed selling prices.

Raw material price fluctuations act as the "conductor" of the market, directly influencing production costs and thereby having a profound impact on profits. When the prices of major raw materials such as high-grade NPI and imported nickel plates rise, the comprehensive procurement cost per mtu increases, leading to a significant rise in production costs. Under such circumstances, if product selling prices remain unchanged or the price increase cannot cover the rise in costs, the profit margin of enterprises will be significantly compressed, potentially leading to losses. Conversely, if raw material prices decline, production costs decrease, and the profit margin of enterprises is expected to expand.

Looking ahead to next week’s stainless steel market, stainless steel finished product prices are expected to remain stable or show a slight upward trend, and market transactions are anticipated to gradually increase. Although the cost side still provides some support for prices, the persistent oversupply situation, coupled with the difficulty in achieving significant short-term improvement in market demand, will undoubtedly limit the upside room for prices.

》Click to View SMM Stainless Steel Spot Historical Prices

》Click to View SMM Stainless Steel Industry Chain Database

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)