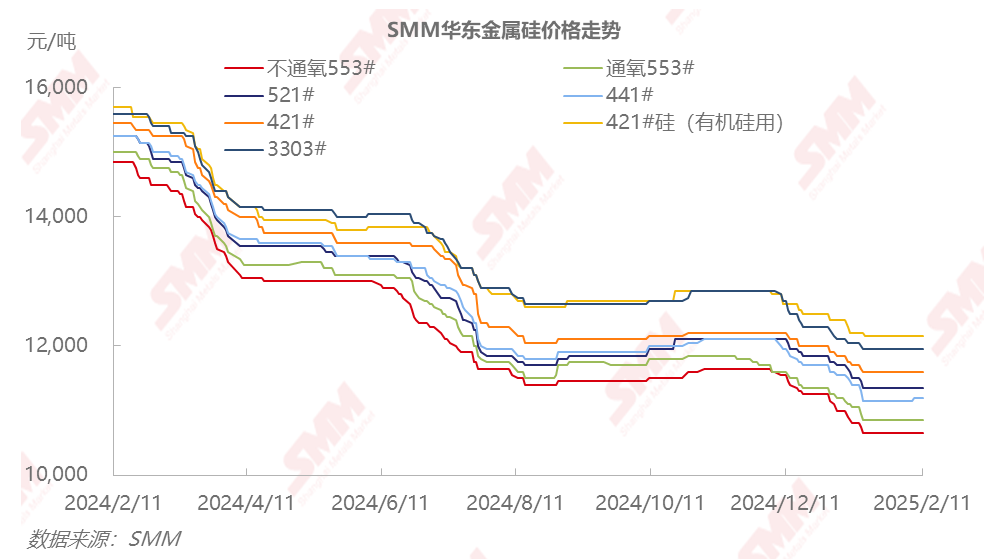

SMM February 16 News: In early January 2025, silicon metal prices continued to decline, stabilizing by late January. From January 28 to February 4, during the Chinese New Year holiday, the domestic silicon market was effectively closed. After the holiday, upstream and downstream enterprises gradually resumed operations, with inquiries from downstream and traders increasing, though transactions remained sluggish due to a wait-and-see sentiment. Post-holiday quotes from silicon suppliers were basically flat compared to pre-holiday levels. As of February 14, above-standard #553 silicon in east China was priced at 10,800-10,900 yuan/mt, down 100 yuan/mt MoM, while #421 silicon was priced at 11,500-11,700 yuan/mt, down 50 yuan/mt MoM.

Supply: According to SMM data, silicon metal production in January was 304,000 mt, a decrease of 28,000 mt or 8.3% MoM. The reduction in January was mainly concentrated in Xinjiang, Sichuan, and Yunnan regions. In Xinjiang, the decline was driven by production cuts from leading silicon enterprises, while in Sichuan and Yunnan, high costs during the dry season led to production cuts. In February, operating rates among silicon enterprises of varying scales showed mixed trends. Due to fewer production days in February, silicon metal supply is expected to drop to around 280,000 mt for the month. In March, national production is expected to increase MoM.

Demand: SMM data shows that polysilicon production in January was 94,400 mt, with no significant MoM change. February polysilicon production is expected to reach 93,000 mt, with minimal fluctuation compared to the previous month. Silicone production in January was 220,700 mt, down approximately 6,000 mt MoM. February DMC production is expected to slightly decline to 213,000 mt. In late February and March, some silicone monomer capacities are scheduled for regular maintenance, leading to a continued slight decline in silicone production in March, with limited impact on silicon metal consumption. March-April marks the traditional peak season for downstream silicone consumption. Coupled with silicone monomer enterprises' intention to stand firm on quotes, DMC prices are expected to strengthen from late February to early March. Aluminum alloy enterprises experienced a decline in operating rates in February due to the Chinese New Year holiday. Post-holiday, aluminum alloy enterprises may face short-term impacts from insufficient orders during the off-season for downstream die-casting enterprises, with gradual recovery expected in late February and March.

Bullish Factors: Rising DMC prices and post-holiday restocking demand

Bearish Factors: Slow inventory destocking and higher-than-expected increases in operating rates among northern silicon enterprises

SMM View: Based on market transactions during the two weeks following the Chinese New Year, export transactions performed relatively well, with alloy and silicone users primarily purchasing as needed. In January-February, the supply-demand balance for silicon showed slight destocking, with a two-month balance of approximately negative 30,000 mt. This marks the first destocking since May 2024 based on supply-demand balance data. In March, operating rates for silicone and polysilicon are expected to see slight changes, while aluminum alloy operating rates are expected to rise. On the supply side, some capacities under maintenance in northern regions are expected to resume production, while low operating rates in south China leave limited room for further supply reductions. Silicon metal supply in March is expected to increase MoM. Overall, maintaining the destocking pace in March appears challenging. The supply-demand dynamics provide weak upward momentum for silicon metal prices. The market will focus on changes in buyer-seller sentiment and any external unexpected factors that may disrupt the market.

For more detailed market information and updates, or if you have other inquiries, please call 021-51666820.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)