SMM February 13 News:

Price Review:

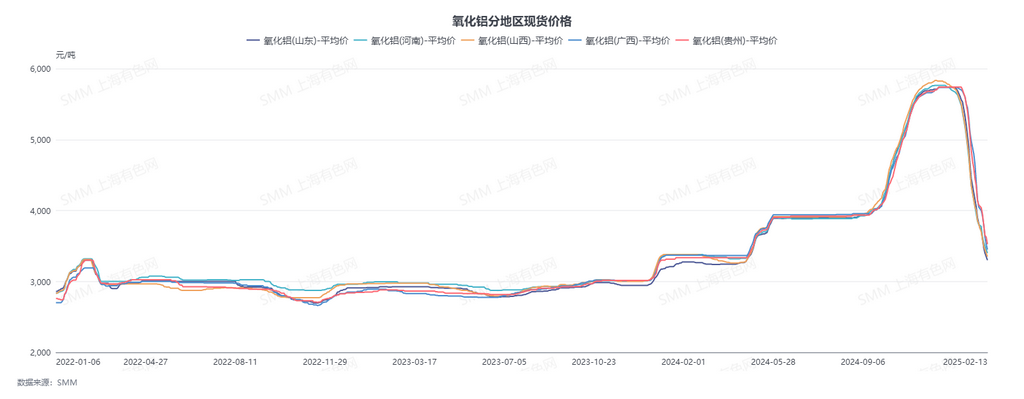

As of this Thursday, the SMM regional weighted index was 3,391 yuan/mt, down 411 yuan/mt WoW. Among them, Shan Dong reported 3,250-3,350 yuan/mt, down 425 yuan/mt WoW; Henan reported 3,350-3,450 yuan/mt, down 375 yuan/mt WoW; Shanxi reported 3,250-3,450 yuan/mt, down 350 yuan/mt WoW; Guangxi reported 3,400-3,500 yuan/mt, down 550 yuan/mt WoW; Guizhou reported 3,450-3,600 yuan/mt, down 515 yuan/mt WoW; Bayuquan reported 4,610-4,690 yuan/mt.

Overseas Market:

As of February 13, 2025, FOB Western Australia alumina prices were $538/mt, ocean freight rate was $19.70/mt, and the US dollar/yuan exchange rate selling price was around 7.31. This price translates to an ex-factory selling price of approximately 4,688 yuan/mt at major domestic ports, 1,247 yuan/mt higher than domestic alumina prices, keeping the alumina import window closed. This week, one new overseas alumina spot transaction was recorded: on February 11, 30,000 mt of alumina was transacted at $538/mt FOB Western Australia or $534/mt FOB Eastern Australia, with shipment scheduled for late March.

Domestic spot alumina prices continued to plummet, with the lowest spot transaction prices in northern China this week reaching around 3,200-3,300 yuan/mt. Considering freight and port miscellaneous fees, this translates to an FOB price of approximately $460-490/mt, lower than Australian alumina FOB prices, potentially gradually opening the export window.

Domestic Market:

According to SMM data, as of this Thursday, the national weekly operating rate of alumina decreased by 0.36 percentage points WoW to 86.94%. Among them, the weekly operating rate of alumina in Shandong remained flat WoW at 92.66%; in Shanxi, it decreased by 1.03 percentage points WoW to 79.57%; in Henan, it decreased by 0.71 percentage points WoW to 68.45%; and in Guangxi, it remained flat at 93.94%. During the period, aluminum smelters were relatively active in tendering and purchasing alumina, and spot transaction prices continued to decline. This week, spot transaction ex-factory prices for alumina in Henan were 3,320-3,550 yuan/mt; in Guizhou, 3,420-3,700 yuan/mt; in Guangxi, delivery-to-factory prices in Yunnan were 3,460 yuan/mt. Additionally, aluminum smelters in Xinjiang tendered for some spot alumina, with delivery-to-factory prices around 3,600-3,800 yuan/mt, while aluminum smelters in north-west China tendered for some spot alumina, with delivery-to-factory prices at 3,425-3,525 yuan/mt.

Overall:

Supply side, some alumina refineries in northern China reported maintenance this week, which may slightly impact alumina supply in the short term, with the weekly operating rate of alumina slightly decreasing by 0.33 percentage points. Demand side, some aluminum production capacity in Sichuan and other regions undergoing technological transformation or production cuts may gradually resume production, increasing demand for alumina. Cost side, due to the sharp decline in spot alumina prices, alumina refineries have significantly reduced their acceptance of high-priced bauxite, leading to a decline in bauxite quotations from holders and a drop in imported bauxite prices. Alumina production costs may decrease accordingly, but current spot alumina transaction prices in northern China are below the theoretical marginal cost of production. Overall, large-scale alumina production cuts have not yet occurred, and the spot alumina market remains relatively ample in supply. Spot transaction prices continue to decline and may maintain a downward trend in the short term.