》View SMM Lead Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Database

SMM, January 24:

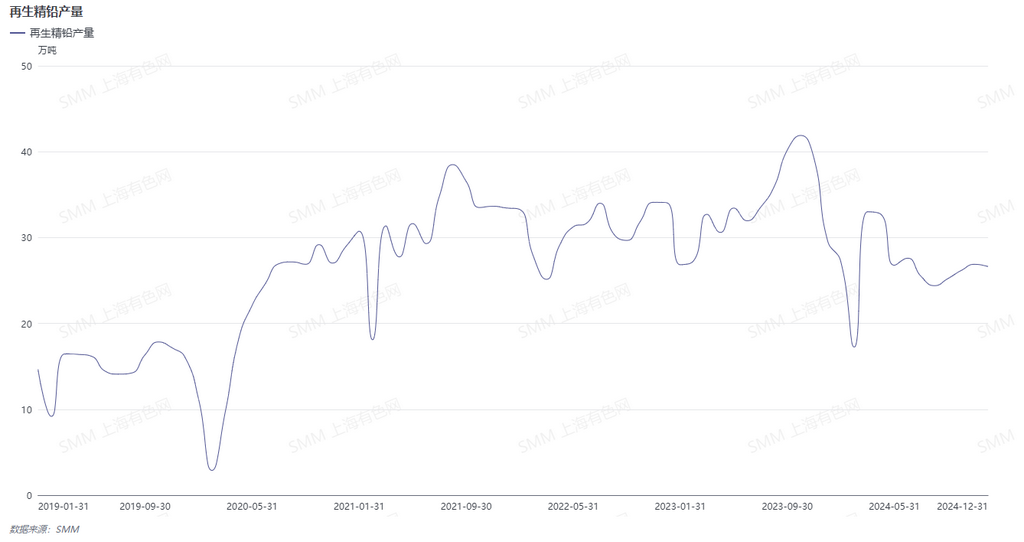

The production of secondary crude lead in January 2025 declined as expected, down 9.23% MoM and 8.57% YoY. Secondary refined lead production fell 13.36% MoM and 15.12% YoY. Frequent heavy pollution weather in December, coupled with secondary lead smelters cooperating with environmental protection-related controls by reducing or halting production, led to tightened supply.

In January, the festive atmosphere of the Chinese New Year gradually intensified, and downstream battery producers started their holiday breaks earlier than usual. Pre-holiday stockpiling demand was weaker than in previous years, making lead ingot transactions challenging. Under such market conditions, secondary lead smelters showed an increased willingness to reduce or halt production during the Chinese New Year break, with some smelters that had suspended production in December postponing their resumption dates until after the holiday. It is reported that the number of secondary lead smelters resuming production before the Lantern Festival is smaller than those resuming after the festival. Additionally, the post-holiday recovery progress of battery scrap recyclers will affect the restocking speed of raw materials for secondary lead smelters. If post-holiday battery scrap supply remains tight, it will also impact the recovery of secondary lead production. Overall, the probability of a significant surge in secondary lead production in February is very low, with the main increase likely to occur in March.