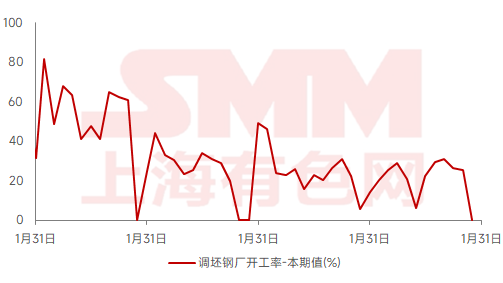

【SMM Operating Rate of Steel Mills Using Externally Purchased Billets】According to the SMM survey, as of January 24, the operating rate of steel mills using externally purchased billets, which mainly produce construction steel, was 0%, down 25.29 percentage points MoM and 5.71 percentage points YoY.

1In January, national construction steel prices first declined and then rebounded. On January 9, the rebar price was 3,327.3 yuan/mt, marking the lowest price of the month. Later, stimulated by macro news, the futures market strengthened, and spot construction steel prices bottomed out.

Cost side, the seventh round of coke price cuts was implemented, but coke supply remained relatively sufficient, and steel mills received adequate deliveries. It is expected that steel mills will not strongly suppress coke prices before the holiday, and coke prices are likely to remain stable with a weak trend in the short term. Supply side, as the Chinese New Year approaches, EAF steel mills have gradually entered the holiday period, with most resuming operations after the tenth day of the lunar new year. Although blast furnace steel mills have resumed production, the overall supply level remains low, with relatively small supply-side pressure. Steel mills using externally purchased billets have already entered the annual holiday. Additionally, due to previous fluctuations in finished steel prices and average profits, some of these mills have taken an early holiday. In January, the operating rate of steel mills using externally purchased billets decreased by 25.29 percentage points MoM and 5.71 percentage points YoY. Demand side, with the Chinese New Year holiday approaching, most downstream construction sites have stopped work and gone on holiday, and traders have gradually left the market. The trading atmosphere is sluggish, and overall transaction performance is poor.

In summary, as the Chinese New Year approaches, market participants are gradually leaving, and steel spot prices show relatively small fluctuations. The fundamentals are in a weak supply and demand pattern. However, the recent macro sentiment is relatively positive, and the market still holds certain expectations for post-holiday policies and demand recovery. It is expected that steel mills using externally purchased billets will gradually resume operations in February, with their operating rate likely to increase.

Chart-1: Operating Rate Trend of Steel Mills Using Externally Purchased Billets, 2020-2024

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)