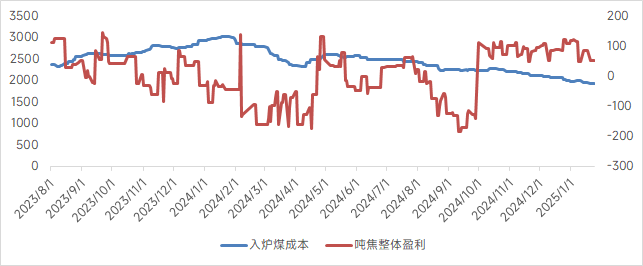

1. According to the SMM survey, coke profit per mt was 49.3 yuan/mt this week, and coke producers' profits continued to narrow.

From a price perspective, coke prices fell by 50-55 yuan/mt this week, exerting a strong negative impact on coke producers' profit per mt. From a cost perspective, the decline in coking coal prices was relatively small. For example, the price of low-sulfur primary coking coal remained at 1,400 yuan/mt, and the price drop for other coal types was also within 50 yuan/mt. As a result, the decline in coking costs was slow, and coke producers' profits shrank significantly.

Before the Chinese New Year, coke prices remained stable, while after the holiday, coke prices are expected to rise. However, coking coal prices are also expected to increase, which will raise coking costs and squeeze part of the profits of coke producers. After the holiday, coke producers may see a slight recovery.

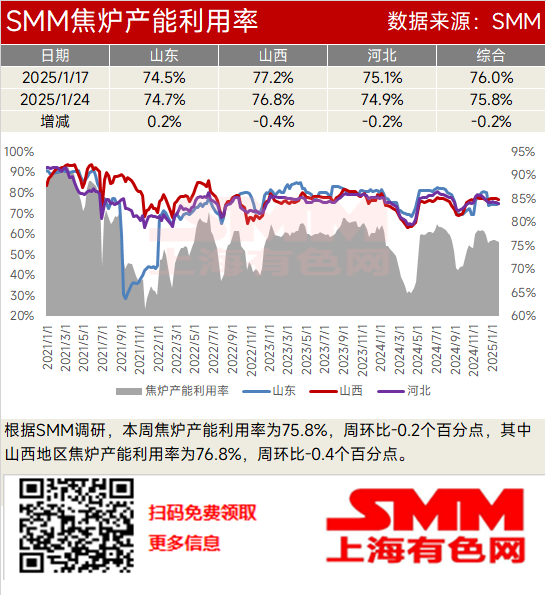

2. According to the SMM survey, the coke oven capacity utilization rate was 75.8% this week, down 0.2 percentage points WoW. In Shanxi, the coke oven capacity utilization rate was 76.8%, down 0.4 percentage points WoW.

From a profitability perspective, most coke producers saw their profits shrink but remained at the break-even point, which had a positive impact on production. From an inventory perspective, coke producers' inventories continued to build up, while downstream steel mills mainly purchased as needed and had largely completed pre-holiday raw material restocking. From an environmental protection perspective, environmental protection policies in Shanxi, Hebei, Shandong, and other regions were relaxed, leading to increased production by coke producers who had previously cut production due to environmental factors.

After the Chinese New Year, the risk of losses for coke producers is relatively small. Even if losses occur, they remain within the acceptable range for most coke producers, allowing them to maintain their original production levels. Coke supply is expected to remain stable. However, with steel mills continuing production and transportation capacity tightening during the holiday, coke restocking will become more challenging, leading to post-holiday restocking expectations in the market. Coke producers are unlikely to continue inventory buildup. In summary, coke oven capacity utilization rates are expected to remain stable.

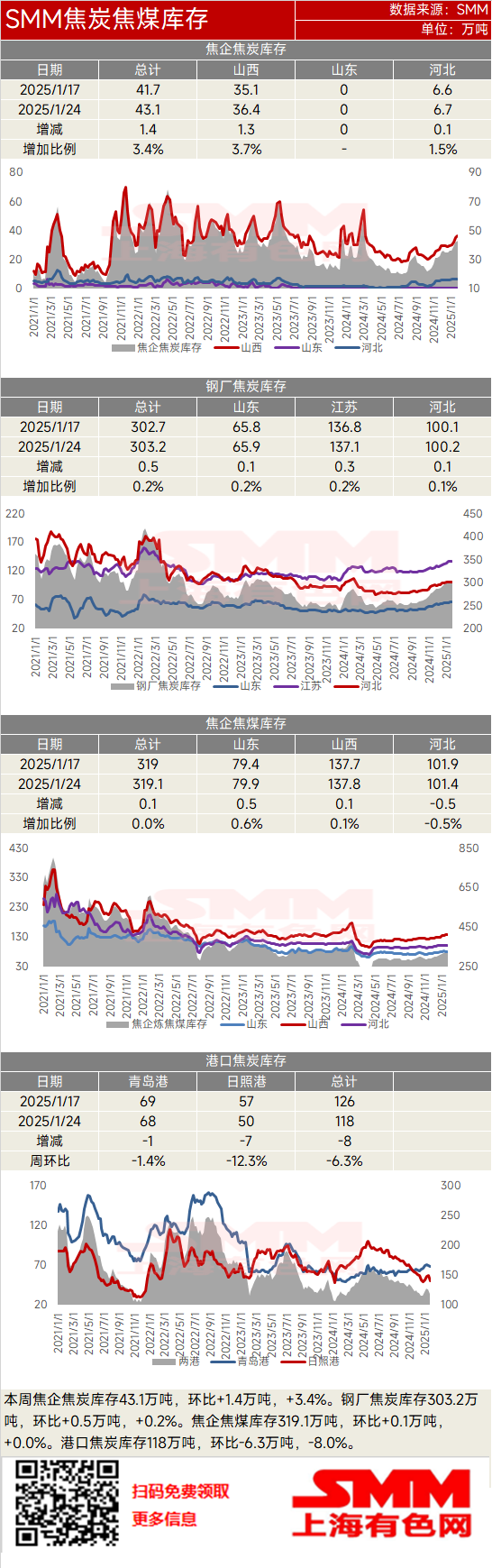

3. This week, coke producers' coke inventory stood at 431,000 mt, up 14,000 mt (+3.4%) WoW. Steel mills' coke inventory was 3.032 million mt, up 5,000 mt (+0.2%) WoW. Coke producers' coking coal inventory was 3.191 million mt, up 1,000 mt (+0.0%) WoW. Port coke inventory was 1.18 million mt, down 63,000 mt (-8.0%) WoW.

This week, coke producers' coke inventory continued to build up, while steel mills' coke inventory fluctuated rangebound. Most coke producers' profits remained at the break-even point, and production levels were stable, keeping coke supply at a relatively high level. Most steel mills had completed pre-holiday restocking and mainly purchased coke as needed. However, tight transportation capacity further increased the difficulty of coke restocking, weakening steel mills' willingness to purchase.

After the Chinese New Year, most coke producers are expected to maintain profitability. Even if losses occur, they will remain within the acceptable range for coke producers, ensuring stable production. During the holiday, transportation capacity will be even tighter, further reducing steel mills' purchasing activities and leading to continued consumption of their coke inventories. As steel mills deplete their coke inventories, post-holiday restocking demand is expected. Therefore, coke producers are likely to continue inventory buildup after the holiday, while steel mills' coke inventories are expected to decline.

This week, most coal mines have already closed for the holiday, leading to a continued contraction in coking coal supply. However, most coke producers' coking coal inventories have reached reasonable levels, and with tight transportation capacity, their willingness to purchase during the holiday is generally low. Online auction prices for coking coal showed mixed performance, further reducing coke producers' purchasing enthusiasm. Therefore, coking coal inventories at coke producers are expected to decline after the holiday.

This week, coke supply remained ample, and the market was in a holiday state. Most traders actively sold goods to increase cash reserves, leading to a decrease in port coke inventories. However, after the holiday, steel mills are expected to have restocking demand, and some traders may continue to stockpile during the holiday, potentially leading to an increase in port coke inventories after the holiday.

![[SMM Steel] Tata Steel partners with Hindustan Zinc for sustainable steel manufacturing](https://imgqn.smm.cn/usercenter/SEwWP20251217171716.jpg)