》View SMM Silicon Product Prices

》Subscribe to View Historical Price Trends of SMM Metal Spot Cargo

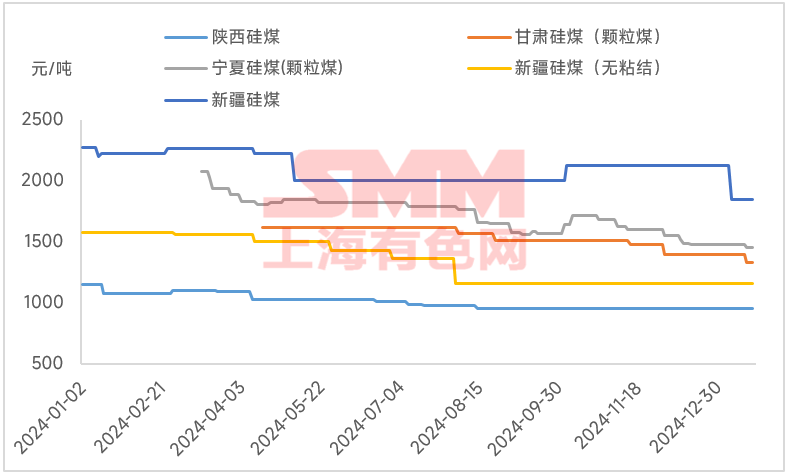

Entering January 2025, silicon coal prices in the raw material segment of silicon metal were the first to decline, starting with silicon coal in the Xinjiang region at the beginning of the month. Recently, silicon coal prices in Ningxia and Gansu regions have also seen varying degrees of reduction. The decline in silicon coal prices in multiple regions at the beginning of 2025 has slightly lowered the cost of silicon metal.

Currently, in the smelting process of silicon metal, silicon coal is a major carbonaceous reducing agent, especially in the all-coal smelting process. Fluctuations in silicon coal prices significantly impact the cost of silicon metal. Since 2025, the successive decline in silicon coal prices in multiple regions has been somewhat beneficial for silicon metal enterprises. However, as silicon metal prices have continued to operate below the cost line, the recent decline in silicon coal prices has not turned losses into profits but has only slightly reduced the losses of silicon metal plants.

Silicon coal prices in the Xinjiang region, which have long remained at high levels, saw a significant reduction at the beginning of this month under the pressure of weak operations and declining production by downstream silicon metal plants. Currently, prices are fluctuating around 1,800 yuan/mt, but they remain relatively high compared to granular coal prices in other regions. Recently, granular silicon coal prices in Ningxia and Gansu regions have also declined. The main reason for the recent price reduction in granular silicon coal in Ningxia and Gansu is the continued downward fluctuation of coking coal prices, which has loosened raw coal prices at the mine, reducing silicon coal costs and allowing silicon coal plants to offer further price concessions to downstream silicon plants. Moreover, many silicon coal plants in Ningxia and Gansu have indicated that subsequent prices will continue to adjust according to market trends. Silicon coal plants in Gansu have explicitly stated that if coking coal prices continue to decline, leading to lower silicon coal costs, they will consider further reducing silicon coal prices. Currently, granular silicon coal prices in Ningxia are at 1,360-1,550 yuan/mt, while in Gansu, prices are at 1,320-1,340 yuan/mt.

Based on the current coal consumption of 1.8 mt in the all-coal smelting process, we can calculate that the decline in silicon coal prices in Xinjiang, Ningxia, and Gansu regions during January 2025 could reduce silicon metal costs by 126-495 yuan/mt (data is for reference only; actual conditions depend on the specific regions of silicon coal chosen by each plant and the different ratios used by each plant). Additionally, as silicon metal plants have a certain procurement cycle for raw materials, the silicon coal currently used for production and smelting was mostly purchased before the price reduction, resulting in a lag in cost fluctuations.

![In the short term, ferrous metals are consolidating at lows, and close attention should be paid to steel mill maintenance situations [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/nDTpN20251217171748.jpg)