》Check SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

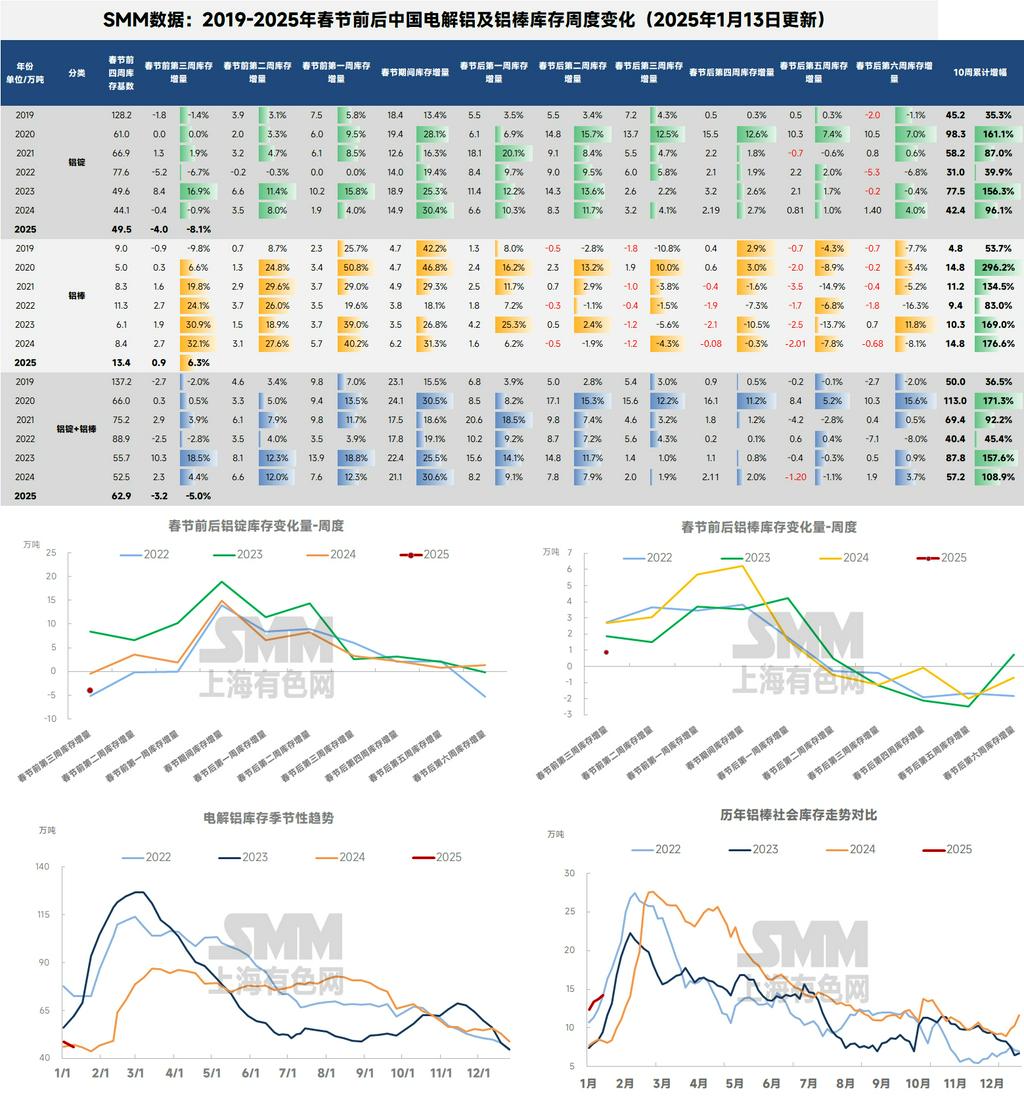

The recent counter-seasonal destocking of domestic aluminum ingots seems to be consistently reflected in the SHFE aluminum futures market.According to SMM statistics, as of January 16, 2025, the social inventory of domestic aluminum ingots stood at 440,000 mt, with 314,000 mt of domestically available aluminum inventory, down 15,000 mt from Monday and 19,000 mt from last Thursday. Notably, as of mid-January 2025, the current domestic aluminum ingot inventory has decreased by 1,000 mt compared to the 441,000 mt in the same period last year, marking a three-year low on a YoY basis. This has significantly boosted market confidence that post-Chinese New Year inventory buildup may fall short of expectations. Coupled with the unexpected cooling of the US core CPI announced last night, hopes for a US Fed interest rate cut within the year have been reignited. As of today's close, the most-traded SHFE aluminum 2502 contract closed at 20,300 yuan/mt, having surged to near the 60-day moving average during the morning session, with a short-term high refreshed at 20,425 yuan/mt, up nearly 500 yuan/mt WoW.

A closer look at the mid-week regional destocking of aluminum ingots reveals that out of the nationwide destocking of 15,000 mt, Gongyi alone accounted for 13,000 mt.Analyzing the latest situation of mainstream supplies nationwide, especially in Gongyi, SMM identifies two reasons for this week's destocking from the inflow side:

(1) Temporary suspension of railway shipments in Qinghai.According to an SMM survey, railway shipments in Qinghai have been disrupted due to pending confirmation of freight rate reductions. Negotiations are ongoing, awaiting the release of a new railway schedule after the 15th to finalize the rate reductions. Currently, shipments from Qinghai rely mainly on direct truck deliveries to downstream Gongyi, significantly impacting local inflow volumes. Despite the destocking, local circulating supply is not tight, leading to a continued rapid decline in spot prices.

(2) Reduced railway shipment efficiency in Xinjiang.According to an SMM survey, a large volume of aluminum products shipped from Xinjiang remains in transit, with no concentrated arrivals yet. The Spring Festival travel rush has extended transit times. Feedback from a Gongyi warehouse indicates that concentrated arrivals are expected to begin over the weekend, with inventory likely to increase by next Monday.

From the outflow side, SMM provides the following analysis:In addition to last week's factors:(1) Insufficient price difference between primary metal and scrap, leading to increased substitution of aluminum scrap with primary aluminum.

(2) Frequent cargo pick-up and outflows from warehouses by downstream buyers this week.Feedback from downstream indicates that the main reason is the limited inflow of aluminum ingots, coupled with factories gradually starting their holidays next week. Those who restocked at lower prices earlier have begun picking up goods. In central China, downstream restocking demand this week has exceeded expectations. Overall feedback includes: "Downstream orders on hand still exist. Some domestic orders were postponed due to earlier rush exports, and there are also temporary impacts from environmental protection measures. The substitution of aluminum scrap remains a factor, depending on order conditions. Overall, the use of aluminum scrap is higher than in 2023." SMM will continue to release the latest survey updates on the pre-holiday operating conditions of downstream sectors in central China. Stay tuned.

However, despite the recent favorable factors for destocking and the slight downward revision of post-holiday inventory buildup expectations, SMM believes that the overall supply pressure of domestic aluminum ingots before and after the Chinese New Year cannot be ignored. The off-season atmosphere for domestic aluminum demand persists, with most downstream sectors entering holiday mode by year-end. Meanwhile, aluminum prices have quickly rebounded above 20,000 yuan/mt, significantly dampening downstream purchasing interest. Subsequent outflows of aluminum ingots are likely to weaken. On the inflow side, with Xinjiang shipments having normalized for some time, in-transit volumes are expected to increase significantly in the two weeks before the holiday, potentially intensifying spot market pressure. The inventory buildup turning point may be confirmed in the short term.SMM expects that with the end of concentrated pre-holiday restocking and the rebound in aluminum prices, domestic aluminum ingot inventory may enter a continuous buildup phase in the second half of January. Pre-holiday inventory may rise to around 500,000 mt, with Q1 inventory peaks potentially reaching 850,000-900,000 mt. Although the Q1 peak forecast is lower than the previous estimate of 1-1.1 million mt due to the unexpected inventory performance since December's price correction, the post-holiday peak may still exceed last year's level due to a significant YoY increase in casting ingot production.

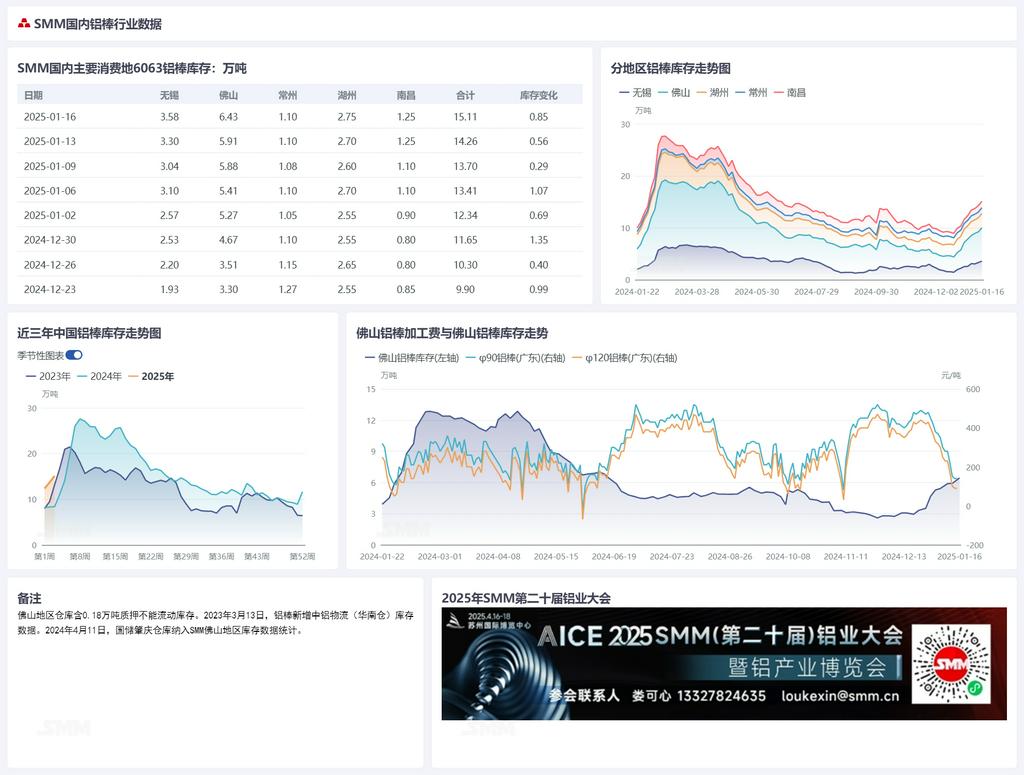

Turning to aluminum billet inventory, as downstream sectors gradually enter holiday mode, overall circulating supply remains ample, and aluminum billet transactions are expected to enter a phase of nominal pricing without actual trades.According to SMM statistics, as of January 16, domestic aluminum billet social inventory stood at 151,100 mt, with an additional buildup of 8,500 mt from Monday and 14,100 mt from last Thursday.On a YoY basis, the gap with the same period last year has widened further to 67,300 mt, remaining at a three-year high.SMM expects domestic aluminum billet inventory to continue building up in January, with pre-holiday inventory potentially reaching 180,000-200,000 mt and post-holiday peaks around 300,000-350,000 mt.