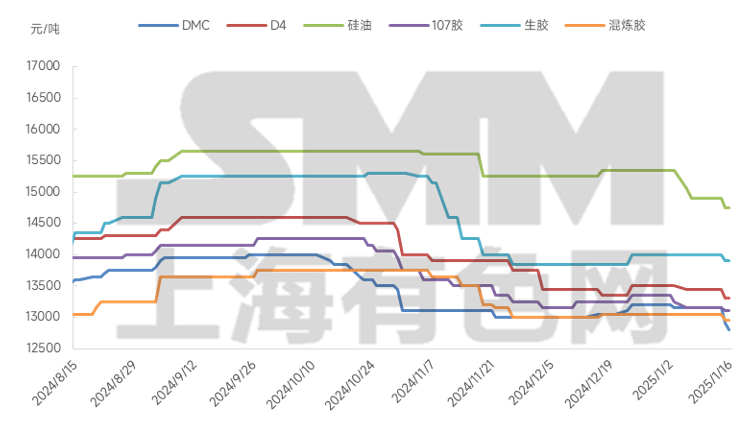

SMM, January 16: This week, the transaction center of silicone monomer enterprises' DMC dropped to 12,700 yuan/mt, but overall market quotations remained relatively stable. The low-price bidding atmosphere was more intense WoW. However, with logistics expected to halt soon, downstream enterprises mainly adopted a wait-and-see attitude in procurement. Some downstream enterprises have already pre-ordered post-holiday orders, leading to intensified competition for orders in the market this week, causing DMC transaction prices to decline rapidly.

Chart: Price Trend of Silicone Products

This week, domestic monomer enterprises lowered their DMC quotations. Shandong monomer enterprises maintained their DMC quotations at 12,800 yuan/mt this week, while other monomer enterprises generally reduced their quotations to 12,800 yuan/mt. However, according to SMM, actual transaction prices for most enterprises have declined, with the lowest market DMC transaction price reaching 12,500 yuan/mt. Although trading volume was limited, it reflected the market's transaction atmosphere and bidding sentiment. Additionally, the slight drop in the cost side of silicon metal and CH3CL prices recently provided support for monomer enterprises to offer slight concessions. However, this round of slight price decline was mainly driven by pre-orders for post-holiday demand, as pre-holiday just-in-time orders were relatively limited. This week, bidding sentiment in the market surged rapidly, and prices of various industry products generally declined, with raw rubber experiencing a significant price drop.

Regarding subsequent price forecasts, SMM believes that prices will remain stable before the holiday. With logistics expected to halt soon, spot prices are likely to remain stable. However, post-holiday pre-orders are expected to maintain a competitive landscape. Currently, as enterprises have sufficient orders on hand, their willingness to further reduce prices is relatively limited. DMC prices are expected to fluctuate between 12,500 and 12,800 yuan/mt.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)