》Lihat Harga Produk Timbal SMM, Data, dan Analisis Pasar

》Berlangganan untuk Melihat Harga Spot Logam Historis SMM

》Klik untuk Melihat Basis Data SMM

SMM, 10 Januari:

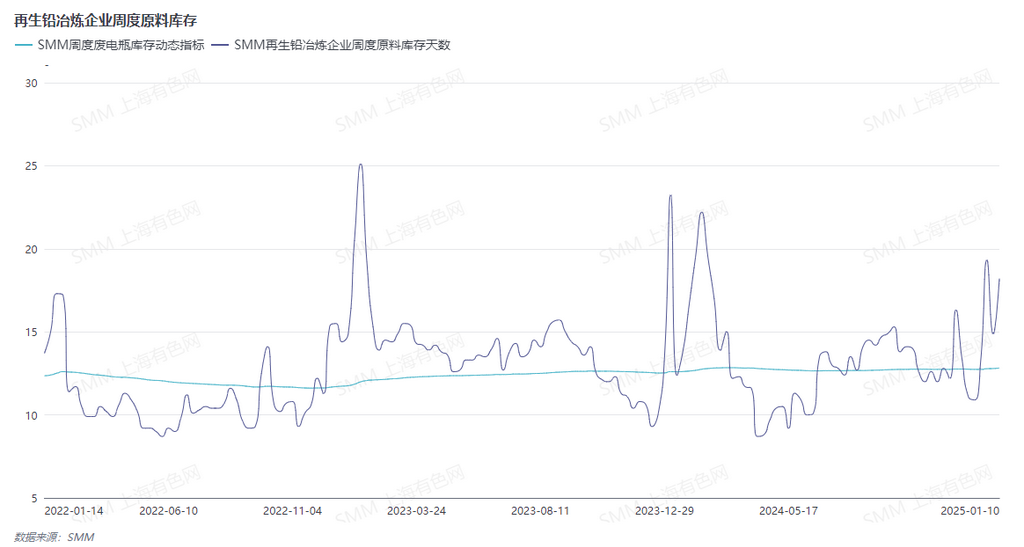

Dampak liburan Tahun Baru Imlek terhadap pasar timbal semakin meningkat. Pengumpul limbah baterai melaporkan bahwa beberapa toko telah berhenti menjual baterai bekas. Sementara itu, peleburan timbal sekunder sedang dalam fase penimbunan bahan baku. Namun, persediaan saat ini tetap melimpah. Data menunjukkan bahwa hari persediaan bahan baku minggu ini melebihi rata-rata historis sekitar lima hari, sehingga ketidakseimbangan pasokan-permintaan belum menjadi signifikan.

Perlu dicatat bahwa banyak produsen baterai kecil dan menengah di hilir menunjukkan keengganan untuk membeli baru-baru ini, menyatakan bahwa penimbunan ingot timbal mereka sebelum liburan pada dasarnya telah selesai dan mereka diperkirakan akan memulai liburan 3-5 hari lebih awal. Selain itu, penimbunan persediaan ingot timbal yang diantisipasi setelah liburan Tahun Baru Imlek dapat menekan harga timbal. Beberapa perusahaan hilir menyatakan kekhawatiran tentang potensi penurunan harga, yang membuat mereka menghindari pembelian ingot timbal secara berlebihan sebelum liburan. Beberapa produsen baterai hilir juga mencatat bahwa menimbun baterai baru lebih menguntungkan daripada menimbun ingot timbal. Saat ini, persediaan baterai baru mereka cukup untuk penjualan hingga Maret, dan mereka melakukan pengadaan ingot timbal secara tepat waktu. Jadwal liburan mereka diperkirakan sedikit lebih lambat dibandingkan perusahaan lain. Dari situasi transaksi ingot timbal saat ini, harga timbal menghadapi tekanan naik.

Bagi peleburan timbal sekunder, meskipun harga pembelian limbah baterai telah diturunkan, kedatangan tetap menjadi perhatian utama. Menurut SMM, meskipun persediaan bahan baku peleburan timbal sekunder saat ini sedang, jika kedatangan tetap ketat minggu depan, perusahaan mungkin terpaksa menaikkan harga pembelian atau memilih untuk menghentikan produksi dan melakukan pemeliharaan selama liburan. Di bawah pergerakan harga timbal yang stagnan saat ini, mengingat tingkat penurunan harga limbah baterai, beberapa peleburan sudah beroperasi dengan kerugian. Akibatnya, jumlah peleburan timbal sekunder yang menghentikan produksi untuk pemeliharaan selama liburan Tahun Baru Imlek ini mungkin meningkat secara signifikan dibandingkan tahun-tahun sebelumnya.

![SHFE Timbal 2608 Ditutup dengan Kenaikan Kecil, Mengakhiri Rentetan Kerugian Empat Hari; Pasar dalam Kelesuan dengan Dukungan di Bawah [Ulasan Kontrak Berjangka Timbal]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)

![Risiko Makro Masih Berlanjut, Pantau Perbaikan Fundamental; Harga Timbal Diperkirakan Mengalami Pemulihan Relatif [SMM Weekly Lead Market Forecast]](https://imgqn.smm.cn/usercenter/lIHfM20251217171721.jpeg)