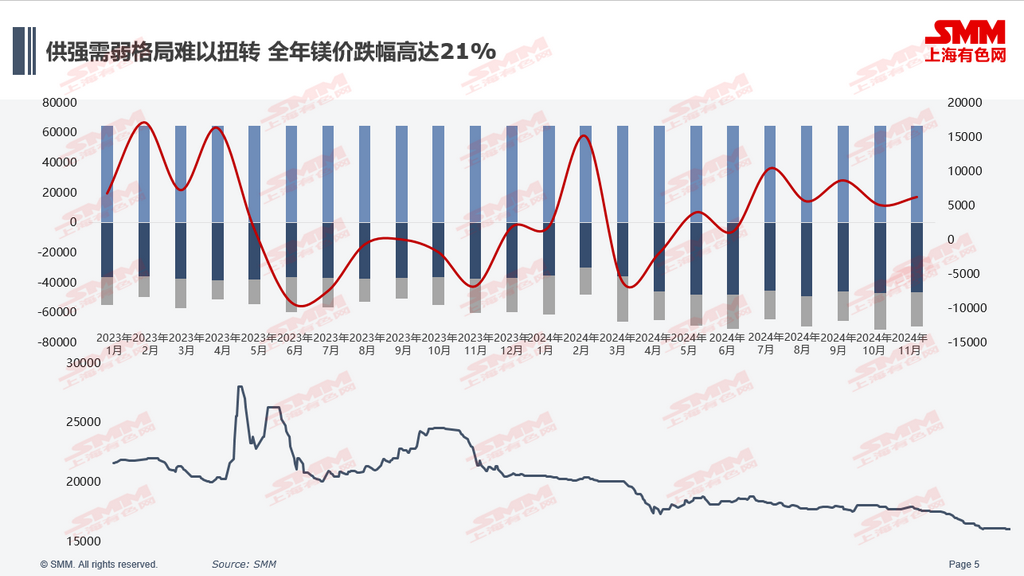

Reviewing this year's magnesium market, it can be summarized as short-term uncertainty but promising prospects for the future. Against the backdrop of carbon neutrality, lightweighting has become a crucial approach for the automotive industry to achieve energy conservation and emission reduction. Magnesium, being only two-thirds the weight of aluminum, has made the application of magnesium alloys in automobiles an important trend for weight reduction, bringing magnesium metal into the spotlight. However, under the guidance of weak current realities but strong expectations, magnesium plants showed unprecedented enthusiasm for resuming production. The concentrated and large-scale resumption of production by magnesium plants led to a supply-demand imbalance in the magnesium ingot market, resulting in a stepwise downward trend in magnesium prices in 2024.

Specifically, by the end of 2023, magnesium plants that had been shut down due to semi coke rectification gradually resumed production, leading to a steady increase in magnesium ingot supply. During the Chinese New Year period, magnesium plants that continued production contrasted sharply with downstream sectors that reduced or halted production, causing magnesium ingot inventory to rise rapidly. Correspondingly, magnesium prices began to plummet, dropping to 17,300 yuan/mt by the end of March.

The significant decline in magnesium prices increased production pressure on magnesium plants, prompting many to announce maintenance plans. In the short term, magnesium prices bottomed out and rebounded. However, the maintenance plans announced earlier by magnesium plants offset the original maintenance schedules for August and September, resulting in a weak supply and demand situation for magnesium prices in Q3. From the overall production data, production in Q2 and Q3 remained relatively stable, with minimal fluctuations.

In Q4, plants that had undergone maintenance gradually returned to full-capacity production. In October, magnesium ingot production increased to 84,000 mt, while magnesium ingot inventory in the Fugu region approached 60,000 mt, with overall inventory expected to exceed 80,000 mt. The supply-strong and demand-weak pattern reopened the downward channel for magnesium prices. As of today, magnesium prices have fallen to 16,000 yuan/mt, marking an annual decline of 14.3%. With magnesium prices breaking through the break-even line for magnesium plants, news of production cuts and halts began to spread in the market. However, supported by the previously accumulated magnesium ingot inventory, downstream sentiment remained pessimistic, leaving little upward momentum for magnesium prices.

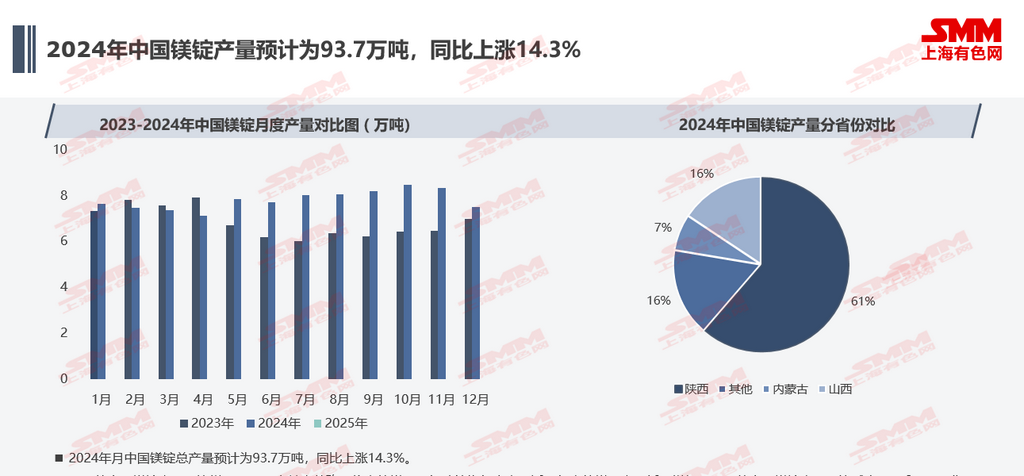

Reviewing China's magnesium ingot supply in 2024, production is expected to reach 937,000 mt, up 14.3% YoY. The increase in China's magnesium ingot production in 2024 mainly stems from the resumption of production by magnesium plants in the Fugu region. According to the 2024 provincial comparison of China's magnesium ingot production, Shaanxi is expected to account for 61% of total magnesium ingot production, up from 50%.

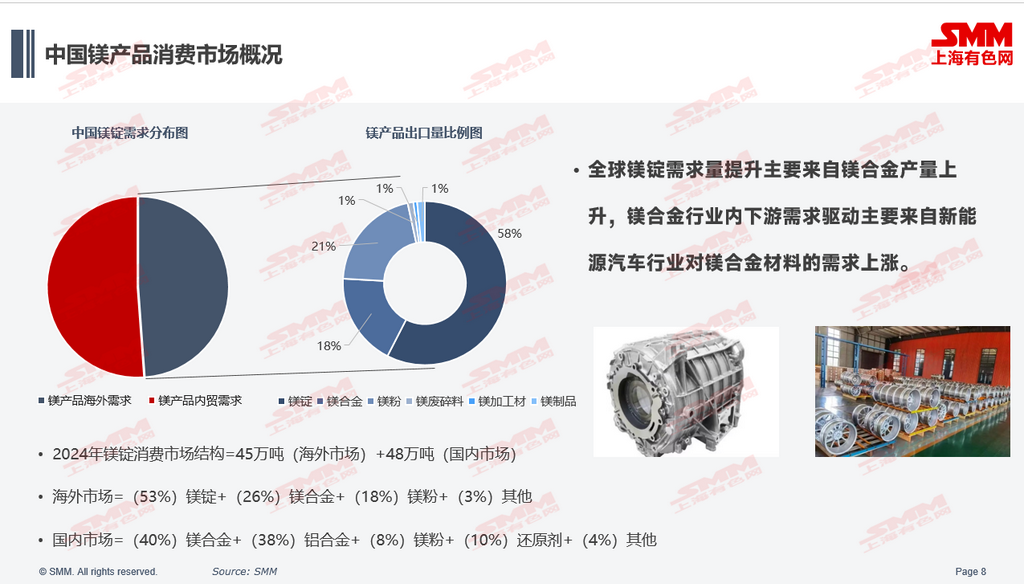

From the perspective of domestic and international demand, the structure of the magnesium ingot consumer market in 2024 can be roughly described as 450,000 mt for the overseas market and 480,000 mt for the domestic market. Looking at the overseas market, magnesium ingots account for 58% of the total export volume of magnesium products in 2024, followed by magnesium alloys and magnesium powder.

In the domestic magnesium ingot market, magnesium alloys hold the largest share at 40%, followed by aluminum alloys at 38%, with desulfurizers and reducing agents accounting for 8% and 10%, respectively. Magnesium ingots are used as additives in aluminum plants, steel mills, and titanium plants, and the demand changes in these three sectors are closely related to the demand conditions of aluminum plants, steel mills, and titanium plants. Growth potential in these three areas is limited. The global increase in magnesium ingot demand mainly comes from the rise in magnesium alloy production, with downstream demand in the magnesium alloy industry primarily driven by the growing demand for magnesium alloy materials in the NEV industry.