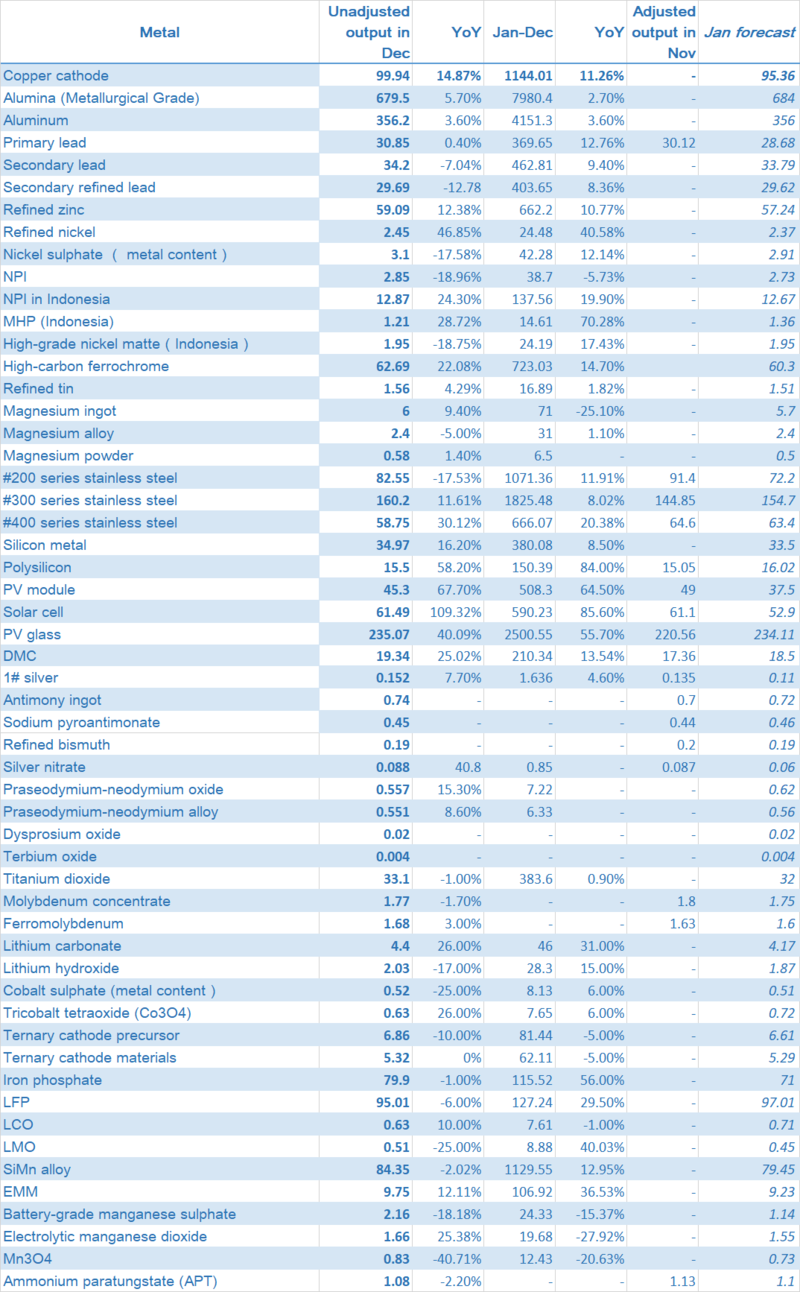

Copper cathode

SMM data showed that in December, China's copper cathode output was 999,400 mt, an increase of 38,600 mt or 3.86% from the previous month, and a year-on-year increase of 14.87%; but a decrease of 5,100 mt from the expected 1.0045 million mt. The cumulative output from January to December was 11.4401 million mt, a year-on-year increase of 1.158 million mt or 11.26%, and the annual increase was the largest in recent years.

Only one smelter conducted maintenance in December, two fewer than in November. This is one of the reasons for the increase in output. In addition, some smelters calculated their December output from November 26 to December 31, which normally counts to the 25th. This also resulted in the substantial increase in December output. However, the output of newly-started smelters was very low in December. This, coupled with the relocation of a smelter in south-west China and the tight supply of blister copper, made December output lower than market expectations. We believe that the average operating rate of copper cathode industry rose 0.21 percentage point month on month to 89.14% in December.

In January, several smelters that were newly started began to release output, but due to the statistical cycle factor, there are fewer days to be counted for the output in January. That will cause output to decline; the relocation of a smelter in the south-west will result in a decline in output. Therefore, the output statistics in January will be significantly lower than in December. Based on the production schedules of various companies, SMM estimates that domestic copper cathode production in January will be 953,600 mt, a month-on-month decrease of 45,800 mt or 4.58%, and a year-on-year increase of 100,300 mt or 11.75%.

Aluminium

According to SMM statistics, China’s aluminium output was 3.562 million mt in December (31 days), an increase of 3.6% YoY. Although domestic aluminium operating capacity increased slightly MoM in December, the electrolytic cells in Yunnan that were shut down previously no longer produced aluminium liquid. In December, the average daily domestic aluminium production dropped by more than 3,800 mt MoM to around 114,900 mt. In 2023, the domestic aluminum output totaled 41.513 million mt, a YoY increase of 3.6%. In December, the domestic aluminium liquid alloying ratio remained high, only some aluminium smelters in Inner Mongolia, Qinghai and other regions saw an increase in the proportion of ingots. Aluminium smelters in other regions mostly executed long-term aluminium liquid contracts, striving to complete the annual aluminium liquid alloying target. The proportion of aluminium liquid rose slightly. SMM estimated that the proportion of aluminium liquid alloying in the industry increased by 0.7 points MoM to around 74.1% in December. According to SMM aluminium liquid ratio data, the domestic aluminium ingot volume in December decreased by 20% YoY. The total amount of aluminium ingot produced in 2023 was approximately 12.06 million mt, a YoY decrease of 11.3%.

Changes in capacity: In December, domestic aluminium operating capacity was largely stable. During the month, power supply and demand in southwest and other regions were stable. Xinjiang, Qinghai, Inner Mongolia and other regions experienced tight power loads due to cold weather, but aluminium industry was less affected. Only Sichuan, Shanxi and some companies carried out a small amount of maintenance, totaling approximately 30,000 mt. In terms of new capacity: In December, all the remaining new capacity of Inner Mongolia Baiyinhua was put into operation smoothly, and other new projects have no commissioning plans in the short term. As of the end of December, according to SMM statistics, the installed aluminium capacity in China was about 45.19 million mt, while the operating capacity was around 41.98 million mt, and the operating rate grew by 0.2 points MoM to 92.9%.

Production forecast: In January 2024, there is no severe power supply shortage in Yunnan and other regions. It is expected that aluminium production in the province may be largely stable. We have not heard of any large-scale maintenance or production plans among other enterprises. SMM predicts domestic aluminium operating capacity may stabilize at around 42 million mt by January. The average daily domestic aluminium production in January will remain stable. The total domestic aluminium production in January (31 days) is expected to be around 3.56 million mt, a YoY increase of 4.2%.

Alumina

SMM data showed that China’s metallurgical-grade alumina output stood at 6.795 million mt in December (31 days), and the daily average output was 219,200 mt/day, down 5,600 mt/day MoM. The total output in December was up by 0.7% MoM and 5.7% YoY. As of the end of December, the installed alumina capacity in China was 100 million mt, the operating capacity stood at 80.04million mt, and the average operating rate stood at 80.0%. In 2023, the domestic alumina output totaled 79.804 million mt, a YoY increase of 2.7%.

In terms of regions, in Shanxi, the province's operating rate in December was 69.2%, a sharp MoM decrease of 9.2%. Due to the upgrade of mine inspection and control policies in Shanxi in December, the ore supply tightness have intensified, affecting production. Therefore, the operating rate declined sharply MoM. In Henan, the operating rate was 61.9% in December, down 1.6% MoM. In December, some alumina refineries in the Sanmenxia maintained production cut since December. Some alumina refineries limited roasting capacity due to local heavy pollution weather warnings, and later resumed production in early January as the warnings were lifted. In Guizhou, the production of a few alumina refineries are still curbed by ore supply and cost issues. In addition, some alumina refineries resumed part of their capacity that was affected by production line maintenance in December. Therefore, the operating rate of Guizhou rose by 2.1% MoM to 84.5% in December. In Hebei, the operating rate in December increased by 6.2% MoM to 87.5%. This was mainly due to the maintenance of a large alumina refinery in November caused by insufficient steam supply due to equipment failure in the thermal power plant, involving annual production capacity of 2.4 million mt. The company had resumed production before December. In Guangxi, the operating rate in December was the same as November at 84.9%. In Shandong, the province's operating rate in December was the same as November at 93.6%. In late December, a large alumina refinery in Shandong had limited roasting capacity due to local heavy pollution weather warnings. Later, as the warnings were lifted, the company had resumed production in early January.

Forecast for January:According to SMM research, it is difficult for mines in Shanxi and Henan to resume production soon. The local ore supply shortage will continue to limit part of the capacity, and the overall operating rate may remain at a low level; In Guangxi, refineries that were affected by ore supply issues in December may find it difficult to return to full production shortly. The roasting capacities in Shandong and Henan that were previosuly subject to environmental protection policies have now resumed production. However, influenced by heavy pollution weather in north China, alumina refineries may face a new round of production controls. SMM estimates that the alumina operating capacity in China will be 220,500 mt/day in January 2024, and the total operating capacity will be around 80.50 million mt, up by 7.3% YoY.

Primary lead

In December 2023, the domestic refined lead production was 308,500 mt, a month-on-month increase of 2.42% and a year-on-year increase of 0.4%; the cumulative output from January to December 2023 increased by 12.76% year-on-year. Total production capacities of enterprises in the survey totalled 5.84 million mt in 2023.

According to research, following intensive maintenance in November, large-scale refined lead smelting enterprises resumed normal production in December, including major delivery brand enterprises in Henan, Yunnan, Jiangxi and other regions, thus bringing about a significant increase in output. During this period, medium and large smelters in Hunan implemented maintenance plans. This, coupled with the insufficient supply of raw materials such as lead concentrate, led to lower-than-expected output at smelters.

At the beginning of 2024, the number of refined lead smelters planning to carry out equipment maintenance in January has increased. For example, smelters in Hunan and Yunnan have suspended production for maintenance as planned. Meanwhile, some smelters in Henan, Guangdong and Jiangxi also undertook maintenance for a week due to equipment failures, which will cause a sharp decline in refined lead production in January. In addition, lead smelters in Qinghai will upgrade the equipment of the lead smelting system as planned, and the technical transformation will last for half a year. Insufficient supply of lead concentrate in Hunan, Yunnan and other regions, as well as the impact of cold weather in high-altitude areas in the north also reduced production. SMM estimates that the month-on-month decrease in refined lead production in January is expected to exceed 20,000 mt, and the output is estimated at 282,600 mt.

Secondary lead

The output of secondary lead in December 2023 was 342,000 mt, a decrease of 23.23% from November and a decrease of 7.04% year-on-year. The cumulative output of secondary lead from January to December 2023 was 4.6281 million mt, an increase of 9.4% year-on-year. The output of secondary refined lead in December 2023 was 296,900 mt, a decrease of 24.22% from November and a decrease of 12.78% year-on-year. The cumulative output of secondary refined lead from January to December 2023 was 4.0365 million mt, an increase of 8.36% year-on-year.

According to research, secondary lead production fell sharply in December, a decrease of 94,900 mt from November. There are three main reasons for the decline in output in December: First, air pollution alerts in Hebei, Anhui, Hubei and Jiangxi caused refined lead smelters to reduce production or shut down in compliance with environmental protection controls; many smelters in Anhui Province, the main production area of secondary refined lead, shut down for a week, resulting in a severe decline in output. Second, the losses have led to secondary lead smelters reducing and suspending production, especially some smelters in Guangxi, Inner Mongolia, Hunan, Jiangsu and Guangdong. Third, the price of battery scrap was low at the beginning of the month. Due to tight battery scrap supply and traders' reluctance to sell, most smelters stopped production due to raw material shortages.

In January, secondary lead companies that suspended production due to environmental protection in December are expected to produce normally. However, many companies have plans to reduce and suspend production in the second half of January. Therefore, refined lead production is expected to fall by more than 4,000 mt in January. The current supply of the battery scrap market is temporarily abundant due to less consumption in December. However, after mid-January, the raw material inventory of smelters will be significantly reduced, and closures of battery scrap traders due to Chinese New Year holidays will affect the recycling volume of battery scrap. SMM expects that the tight supply of raw materials will also prompt some smelters to shut down for maintenance.

Refined zinc

SMM China's refined zinc output in December 2023 was 590,900 mt, an increase of 11,900 mt or 2.05% month-on-month, and a year-on-year increase of 12.38%, which is higher than our previous estimate. The cumulative output of refined zinc from January to December reached 6.622 million mt, a year-on-year increase of 10.77%. Domestic zinc alloy production in December was 102,900 mt, an increase of 9,600 mt from the previous month.

In December, the output of domestic smelters increased, mainly due to the new production capacity in Guangxi, and the restoration from maintenance and year-end output increase of smelters in Hunan, Shaanxi, Henan and Yunnan; output at smelters in Shaanxi, Gansu and Guizhou declined due to maintenance.

SMM predicts that domestic refined zinc production in January 2024 will drop by 17,500 mt month-on-month to 572,400 mt, a year-on-year increase of 11.96%. The decline in production in January is mainly due to the approaching CNY and higher cost and environmental protection issues which prompted some smelters in Guizhou, Sichuan, Anhui, Jiangxi and Guangxi to undertake maintenance. The output of smelters in Inner Mongolia, Yunnan and Hunan declined, and some companies closed for holidays. Some smelters in Yunnan, Guangxi, Shaanxi, and Gansu resumed maintenance and increased output, contributing to a certain amount of output growth.

Refined tin

SMM research shows December refined tin production was 15,685 mt, up 0.8% MoM and 4.29% from YoY. Annual total hit 168,938 mt, up 1.82% YoY. China's December tin ingot production was stable. Yunnan saw minor output changes due to one smelter's plan adjustment; other local companies continued to operate smoothly without any scheduled maintenance. Jiangxi smelters slightly outperformed, boosting output. An Inner Mongolia smelter maintained steady production. In Guangdong, environmental checks reduced one smelter's output. An Anhui smelter ramped up production after resuming operations, contributing to a notable output rise, while most other smelters stayed on track.

January's Yunnan smelting plans are set for stable refined tin output. Jiangxi expects a drop due to maintenance and raw material shortages. A Hubei smelter, closed since late October due to scrap shortages, likely remains shut until post-Spring Festival. Other smelters should keep steady production. January's tin ingot output is predicted at 15,175 mt, down 3.25% MoM but up 26.56% YoY.

Refined nickel

China's December 2023 refined nickel output was 24,500 mt, up 6% MoM and 40.57% YoY, matching SMM forecasts. A northwest smelter's push for year-end growth notably lifted production over November's. December's nickel production growth was spurred by a moderate price rebound and a dip in raw material costs, which allowed smelters who source raw material externally to make profits, prompting previously idle smaller factories to restart production.

China's refined nickel output is expected to hit 23,700 mt in January 2024, down 3% MoM. This is due to potential further price drops amid global stock and production pressures, risking losses if prices near production costs. Also, a smelter has scheduled lower early-year output.

NPI

China's December 2023 NPI output was 28,500 mt in nickel content and 692,800 mt in physical content, down 9.42% MoM and 9.65% YoY, aligning with forecasts. SMM research shows rising nickel ore prices in August left Chinese NPI plants with costly reserves. With NPI prices dropping fast, losses widened, ranging from 6.41% to 18.07%, causing some smelters to cut production or shut for maintenance.

China's January 2024 NPI output is forecasted at 27,300 mt nickel content, down 4.22% MoM. Costly nickel ore stockpiles keep production costs high. With the Spring Festival, plants plan cuts, and weak post-holiday stainless steel demand is foreseen, suggesting a continued dip in NPI production.

Indonesian NPI

Indonesia's December 2023 NPI production reached 128,700 mt in nickel content, up 1.06% MoM and 24.3% YoY. The annual total was 1,375,600 mt, up 19.9% YoY. This aligns with SMM's predictions, and in December, Indonesian medium and high-grade nickel ore premiums normalized. High-grade NPI smelting costs in Indonesia fell, and with December's NPI price rebound, Indonesian NPI plants' profits grew, contrasting with Chinese plants' narrowing losses. This let Indonesia keep normal scheduled production. New capacity in December boosted high-grade NPI output. January's production is expected to stay around 126,700 mt in nickel content, down 1.59% MoM.

Nickel sulphate

China's nickel sulphate output in December 2023 was 31,000 mt in metal content and 140,800 mt in physical content, down 14.32% MoM and 17.58% YoY. End-of-year order reductions and inventory cuts in downstream sectors led to less demand, affecting upstream factories. December saw weak inquiries and transactions for nickel sulphate, with low prices leading to poor profitability, causing salt factories to cut production.

January's precursor scheduled production and nickel sulphate demand stayed weak, with profits still low, suggesting nickel sulphate continued scant supply. China's projected January 2024 nickel sulphate output is about 29,100 mt in metal content and 132,100 mt in physical content, down 6.71% MoM and 6.85% YoY.

Battery-grade manganese sulphate

China's December 2023 high-purity manganese sulphate production was about 21,600 mt, down 17.24% MoM. Ternary cathode material order execution was low, causing cautious precursor scheduled production. Year-end saw most ternary precursor producers focusing on de-stocking rather than increasing output. Demand for high-purity manganese sulphate kept falling. Most companies matched production to sales, with only a few companies planning to stockpile in advance and then concentrate on halting production in the following month, leading to reduced overall output.

January's ternary cathode precursor scheduled production and high-purity manganese sulphate demand are set to fall further, per SMM. With several high-purity manganese sulphate enterprises entering maintenance and focusing on inventory reduction, a major cut in production is expected, with an estimated January output around 11,400 mt, down 47.22% MoM.

Electrolytic manganese dioxide (EMD)

SMM reports China's December 2023 EMD production at 16,600 mt: 1,100 mt of LMO-oriented EMD, 10,300 mt alkaline battery EMD, 5,200 mt zinc-carbon battery EMD, down 8.68% MoM, up 25.38% YoY. Total 2023 production was about 196,800 mt, down 27.92% YoY. EMD production fell for LMO and alkaline types, except zinc-carbon. LMO market's weak demand cut its procurement, shifting firms to zinc-carbon EMD, resulting in an increase in the production of zinc-carbon EMD. Alkaline type dipped slightly as year-end inventory reduction took priority. Despite stable downstream demand, scheduled production remains cautious.

As the Spring Festival nears, some battery cell makers may slightly increase their alkaline manganese and zinc-carbon EMD orders. Yet, EMD firms could keep lower operating rates to cut stock, and the LMO market may stay weak. Overall, January's EMD production is estimated at around 15,500 mt.

Trimanganese tetroxide (Mn3O4)

SMM data shows China's December 2023 Mn3O4 production was 8,300 mt (4,700 mt electronic grade, 3,600 mt battery grade), down 8.59% MoM and 40.71% YoY. The total 2023 production was 124,300 mt, down 20.63% YoY. LMO cathode firms cut scheduled production, reducing demand for battery-grade Mn3O4. Electronic-grade Mn3O4 production stayed normal amid lukewarm end-market demand.

Entering January, the LMO market's prospects darken, likely leading to less production for LMO firms and a drop in battery-grade Mn3O4 output. Year-end inventory cuts by Mn3O4 companies might also slightly lower electronic-grade production. January's total Mn3O4 production is projected at about 7,300 mt.

High-carbon ferrochrome

December 2023 saw national high-carbon ferrochrome output in China dip to 626,900 mt, down 5.16% MoM, but up 22.08% YoY. Inner Mongolia produced 443,400 mt, down 0.36% MoM, while Sichuan's output fell sharply by 63.16% to 10,500 mt. In December, steel mills’ bid prices fell by 200 yuan/mt (Cr50%), pushing all domestic ferrochrome producers under long-term contracts into negative margins. Sichuan's dry season caused power shortages and ferrochrome factory shutdowns. In Inner Mongolia, less severe negative margins, long-term contracts, and delivery pressures meant a limited drop in ferrochrome supply.

January's high-carbon ferrochrome production is expected at 603,000 mt, down MoM. Bid prices from steel mills were stable. Due to strong stainless steel orders, and pre-holiday stocking, ferrochrome demand has firmed, tightening retail supply. Yet, with market supply still relaxed, price hikes are unlikely, keeping ferrochrome factories in negative margins and possibly reducing their operating rates further in January.

Stainless steel

SMM reports China's December 2023 stainless steel output at roughly 3.015 million mt, up 0.22% MoM and 4.40% YoY. By series: 200 series production was about 825,500 mt, down 9.68% MoM and 17.53% YoY; 300 series was around 1.602 million mt, up 10.60% MoM and 11.61% YoY; 400 series was about 587,500 mt, down 9.06% MoM but up 30.12% YoY. Indonesia's December output was about 410,000 mt, up 1.23% MoM and 46.43% YoY.

In December, as the year closed, stainless steel production at domestic mills varied. Equipment maintenance at some mills, especially for the 200 series, cut production by about 88,500 mt. Meanwhile, East China mills post-maintenance and year-end order boosts, particularly for the 300 series, raised production by 153,500 mt.

Short-term, ferrous sector rebound and winter stockpiling sentiment have warmed rebar and HRC demand, lifting prices. Some blast furnace process smelting steel mills have thus adjusted molten iron supply to stainless lines, mainly affecting 400 series production, with a national December output drop of 58,500 mt.

January's stainless steel spot market sales cycle may shorten due to the Spring Festival and weak demand, prompting production expectation adjustments by manufacturers. Estimated national stainless steel billet production for January is about 2.903 million mt, down 3.71% MoM. By series: 200 series is expected at 722,000 mt, down 12.54% MoM; 300 series at 1.547 million mt, down 3.43% MoM; and 400 series at 634,000 mt, up 7.91% MoM.

EMM

SMM data shows that China produced 97,500 mt of EMM in December, down 0.29% MoM but up 12.11% YoY. EMM output in 2023 totalled some 1.0692 million mt, up 36.53% YoY. The main reason for slight output slip in December was shutdown of some EMM plants in Hunan and Hubei. But meanwhile, there was production hike and restart of EMM plants in Guangxi and Guizhou. Demand: Crude stainless steel in China increased in December, of which output of 200 series kept dipping while that of 300 series hiked. Intensive bids from steel mills for January and February offered acceptable support for EMM demand.

In January, EMM plants will keep the operating rate of 70%, while some planned not to produce goods until after the Lunar New Year. Therefore, the overall EMM supply will switch to diminish. According to SMM survey, EMM output may be some 92,300 mt in January.

Silicon metal

China produced 349,700 mt of silicon metal in December, down 54,000 mt or 13.3% MoM but up 16.2% YoY, bringing total output from January to December 2023 up to 3.8008 million mt, up 8.5% YoY, according to SMM statistics.

The operating rate of silicon plants in Yunnan and Sichuan kept dipping in December, as silicon plants cut production starting late November, involving more than 50,000 mt of output. Despite production cuts/halts amid power rationing in northern Xinjiang, silicon metal production changed little in December, which boiled down to two reasons. One reason was that large silicon plants in Xinjiang made operating rate higher in early December, in spite of some restricted capacities in mid-to-late December. The other reason was that shutdown of some silicon plants in Yili occurring on December 26 exerting minimal impact on the output of the month.

In January, silicon plants in Sichuan and Yunnan will keep operating rate low, while some will cut production at the end of December or early January. In Xinjiang, restart date of silicon plants will be unknown. The operating rate of silicon plants in the rest regions will remain unaltered. In a word, there will be a question mark over domestic silicon supply in January, and the output is more likely to decrease.

Polysilicon

Scheduled polysilicon production in China was up 2.9% MoM at 155,000 mt in December, but it was 2,000-3,000 mt lower than expected, mainly due to shutdown of some plants for technical upgrade and power rationing policy in Xinjiang and Inner Mongolia. N and P-type materials continued to diverge. The proportion of N-type materials from major manufacturers basically remained above 50%. Scheduled polysilicon production may total 160,000 mt in January.

PV module

According to SMM statistics, PV module production in China in December was down 8.85% MoM at 45.3GW. Scheduled PV module production kept dipping in China. Global PV module inventory still exceeded 100GW. Weighed down by issues such as policies, electricity prices and land, downstream installation demand in December fell short of expectations. Market sentiment remained pessimistic. In January, scheduled PV module production will plummet to be less than 40GW.

Solar cell

The actual solar cell output in December was 61.1GW, including 31.87GW of P-type cells, down 14.45% MoM, and 30.23GW of N-type cells, up 20.01% MoM. Many cell makers chose to cut production or even suspended production of PERC cells, while N-type cell production kept hiking, lifting its proportion of total output to 48.68%, significantly exceeding expectations. PERC demand will drop in January. Meanwhile, with steep capacity rise, Topcon cell supply will outnumber demand. The proportion of scheduled N-type cell may hike to over 60% of the total output in January 2024.

PV glass

According to SMM statistics, the monthly PV glass output in China was up 6.58% MoM at 2.3507 million mt in December. A big part of the hike in output was because of ramp-up of new capacity. SMM believed that PV glass output will be largely stable in January 2024.

DMC

According to SMM statistics, China’s DMC production in December was some 193,400 mt, up 11.41% MoM. The operating rate of DMC plants inched up to 80.92% in December. The reason behind the output hike was high production enthusiasm, restart of DMC plants from maintenance and delayed plan of maintenance.

SiMn alloy

SMM data showed that SiMn alloy production in China in December totalled 843,500 mt, down 8.92% MoM and 2.02% YoY, bringing total output from January to December 2023 up to about 11.2955 million mt, up 12.95% YoY. SiMn alloy plants in northern China, like in Inner Mongolia, kept the operating rate stable, except for some due to power rationing. However, the actual output changed little. In Ningxia, weak costs and air pollution alert curbed SiMn alloy production. In southern China, a large output slip was felt from impact of falling price.

In January, SiMn alloy plants in areas with cost advantages such as Inner Mongolia will keep production stable, while SiMn alloy plants in other regions will have falling production enthusiasm due to issues of costs and logistics transportation. SiMn alloy output may keep dipping to some 794,500 mt in January amid delayed restart and production cutbacks.

Magnesium ingot

SMM data showed that China's magnesium ingot production in December was 60,613 mt, up 9.4% MoM but down 8.1% YoY, bringing total output from January to December 2023 up to about 709,000 mt, down 25% YoY.

The magnesium plants that were shut for semi-coke's rectification in the main production area resumed production in December. In addition, several large plants with larger capacity resumed production. In contrast, several large plants didn’t resume full production yet. The reason behind falling production of magnesium ingot plants was that profit erosions amid falling price to nearly break-even level tipped some magnesium plants into operating rate slide. Generally speaking, overall magnesium ingot output increased in December. Currently, magnesium price dipped to 20,000 yuan/mt. In addition, overseas demand not picked up yet. If the price slip remains, magnesium plants may reduce production. SMM predicted that magnesium ingot production will be reduced to 57,000 mt in January.

Magnesium alloy

According to SMM data, China's magnesium alloy production in December 2023 was 24,291 mt, down 5% MoM and 2.3% YoY, bringing total output from January to December 2023 up to about 310,000 mt, up 1.1% YoY.

With stable orders amid low magnesium ingot price, most major magnesium alloy plants operated as usual according to production plans. The reason for production reduction was that domestic economic downturn and muted demand set off shutdown of two magnesium alloy plants. Given the upcoming Chinese New Year, magnesium alloy demand will take time to pick up, leaving magnesium alloy plants with no plan of production resumption. SMM predicted that magnesium alloy production will remain at 24,000 mt in January.

Magnesium powder

SMM data showed that China's magnesium powder production in December was 5,788 mt, up 1.4% MoM, bringing total output from January to December 2023 up to 65,000 mt.

Magnesium powder market performed well in December, with most producers arranging tight production schedule and some in full swing. The person in charge of a large magnesium powder company said that sluggish domestic economy fed into poor profit of steel mills, making downstream buyers prudent. Affected by Houthi’s attack on merchant ships in Red Sea, magnesium powder whose exports accounted for a large proportion of total export in China witnessed a big rise in sea freight fees, which may tame overseas orders. SMM predicted that domestic magnesium powder output will dip to 5,000 mt in January.

Pr-Nd oxide

China's Pr-Nd oxide output in December was 5,922 mt, down 4.9% MoM. Much of the blame for the decrease was Jiangxi where output fell by 22%.

According to SMM research, suffering severe losses, most NdFeB scrap recyclers lowered operating rate. Some separation plants halted production for maintenance towards the end of 2023. Under this circumstance, Pr-Nd oxide output plummeted in December.

Pr-Nd alloy

China’s Pr-Nd alloy output in December was 5,574 mt, up 1.2% MoM.

Supported by a large buyer’s orders, the operating rate in Inner Mongolia increased by 3 percentage points MoM to 75%. According to SMM statistics, Pr-Nd alloy price fell to 540,000 yuan/mt in December, down 47,500 yuan/mt MoM. Pr-Nd alloy price kept dipping after New Year's Day. Traded price of Pr-Nd alloy dropped to 510,000 yuan/mt recently. Magnetic material companies who were in strong wait-and-see mood made few inquiries, keeping dragging down Pr-Nd alloy price. Low operating rate of magnetic materials makers will leave Pr-Nd alloy plants with limited incentive to produce goods in January. SMM will continue to pay attention to the start-up of new capacity in northern China.

Dysprosium oxide

China’s dysprosium oxide production in December was 203 mt, down 6.2% MoM. The dip was mainly reflected in Jiangxi.

According to SMM, there were shutdown of some separation plants for maintenance in Jiangxi in December. In addition, severe losses led local scrap recyclers to lower operating rate to 30%. Therefore, dysprosium oxide production in Jiangxi shrank by 24%. Sustained dysprosium oxide price slip made buying appetites low, thereby fuelling weak trading volume in the dysprosium oxide market.

Terbium oxide

China’s terbium oxide output in December was 38 mt, down 8.3% MoM. The dip was mainly reflected in Jiangxi.

According to SMM research, heavy losses led scrap recyclers to cut operating rate, thereby lowering domestic terbium oxide production. Muted demand and rolling price drop resulted in less terbium oxide transactions. With the end of maintenance of separation plants, terbium oxide output will rebound slightly in January 2024.

Molybdenum concentrate

SMM data showed that China's molybdenum concentrate output was 17,700 mt in December, unchanged MoM. In December, molybdenum ore mines still maintain high operating rate, mainly because robust demand served as a big driver for profit of molybdenum concentrates.

Shutdown of a molybdenum mine in Inner Mongolia and intensifying environmental and safety controls at some private molybdenum mines at the end of the year is expected to make a dent in molybdenum concentrate production in January.

Ferromolybdenum

According to SMM data, China’s ferromolybdenum output was up 3% MoM at 16,800 mt in December.

On the demand side, steel mills made an open bidding for 16,000 mt of ferromolybdenum in December, hitting a year-to-date high. As most smelters got their hands full already with orders for January 2024 in mid-to-late December, ferromolybdenum production increased. In addition, some smelters increased production amid capacity surplus, further pushing up ferromolybdenum output.

In January, year-end demand from steel mills may offer a big boost to the operating rate of ferromolybdenum smelters. It is expected that ferromolybdenum output in January will remain stable or keep hiking.

Silver

According SMM Statistics, China’s 1# silver output was 1,524.005 mt (including 1,069.005 mt of mineral silver), up 173.216 mt or 12.8% MoM and 7.7% YoY. Silver output in Jan-Dec 2023 totalled 16,364.475 mt. Most domestic silver smelters increased production in December 2023. At the same time, high silver price shored up selling appetites of raw material suppliers. Therefore, silver output hiked in December, in a bid to complete annual production target in 2023.

In January, the US ADP employment figure in December was 162,000 people, higher than the previous value of 101,000 people and an estimate of 115,000 people. The US unemployment rate was 3.7% in December, the same as the previous value and 3.8% lower than an estimate. The US’ seasonally adjusted non-farm payrolls in December was 216,000 people, higher than the previous value of 173,000 people and an estimate of 170,000 people. Negative news and strong US dollar index led to slight silver price slip.

Silver nitrate

Silver nitrate manufacturers with sales qualifications produced 880 mt of silver nitrate in December, up 0.9% MoM and 40.8% YoY. The output of the surveyed enterprises accounted for about 85% of the market. Therefore, China’s silver nitrate output totalled about 1,035 mt. The reason for mixed silver nitrate production was shrinking P-type solar cell demand and stable N-type solar cell demand were felt in the period of switching from P-type capacity to N-type capacity. Under this circumstance, P-type back silver powder makers and some P-type positive silver powder producers were most heavily affected. Producers who were able to produce N-type silver powder or P-type positive silver powder applicable to N-type had relatively stable demand, while the rest decreased demand. With more scheduled production of some producers, silver nitrate output in December remained normal or increased. In contrast, a few who had inventory or back-to-back orders and production lowered production. Therefore, silver nitrate output mixed in December. High silver price in December and rising proportion of silver powder imports required in N-type will still blunt silver nitrate production. Therefore, SMM expected silver nitrate production to decline in January.

Antimony ingot

According to SMM survey, China antimony ingot (including antimony ingot, converted crude antimony, cathode antimony, etc.) output in December was 7,432 mt, up 6.26% MoM. a large number of producers halted production. Some saw changeable output. In a word, antimony ingot output changed little. Production situation in recent months revealed that raw materials were further concentrated in the hands of some producers, making it difficult for many manufacturers to increase output. In detail, among the 33 survey respondents, 12 makers stopped production, down 2 MoM; 19 cut production, up 3 MoM; and 7 maintained normal production, down 1 MoM. SMM predicted that China’s antimony ingot production in January 2024 will largely remain stable amid rolling antimony ore supply tightness.

Domestic suppliers’ reluctance to sell and some geopolitical factors may keep imported antimony ore tight in the first half of 2024. Under this circumstance, antimony ingots were mainly possessed by large manufacturers who had raw materials. Strong antimony ore made for high costs. Under this circumstance, bargaining power was gradually tilted towards resource holders. It is expected that antimony price may hike in January 2024.

Sodium antimonate

According to SMM's survey statistics, China's sodium antimonate output in December remained high of 4,470 mt, up 1.64% MoM, winding up last month’s drop.

In detail, among the 11 survey respondents, there was shutdown of 2 manufacturer, normal production of 2 producers and rising production of 4 producers and falling production of 3 producers. Given the general stockpiling around the Lunar New Year, sodium antimonate output inched up in December 2023, and may move up in January 2024. Manufacturers were optimistic about PV output hike in 2024, and PV demand may be robust. Therefore, SMM predicted that domestic sodium antimonate output may remain stable or keep rebounding in January 2024.

Refined bismuth

According to SMM's survey, China's refined bismuth production in December was 1,906.968 mt, down 4.5% MoM. In detail, among the 24 survey respondents, 6 makers stopped production in December, down 1 MoM. 5 producers slashed production. SMM predicted that it is more likely that refined bismuth production in China will remain stable in January 2024, or keep shrinking amid tight raw material supply.

Customs data showed that China's bismuth trioxide exports dipped to 368 mt in November 2023.

Titanium dioxide

According to SMM data, China's titanium dioxide output was 33,000 mt in December, down 1% MoM but up 17.7% YoY, bringing total output in from January to December 2023 up to 3.836 million mt, down 0.9% YoY.

Low Titanium dioxide was felt in a slack season. Responding to a rapid inventory hike, some titanium dioxide producers started carrying out maintenance. Titanium dioxide production dipped. Overseas buyers refilled stocks at bargain price tightened spot supply of titanium dioxide in December, leaving producers with no inventory pressure. Therefore, titanium dioxide makers may increase price. With forthcoming Lunar New Year, titanium dioxide producers may suspend production. SMM estimated titanium dioxide production at 320,000 mt in January 2024.

APT

SMM data showed that Chinese APT output was down 2.2% MoM at 10,800 mt in December.

In December, elevated tungsten concentrate price and downstream sectors’ cost pressure piled pressure on APT market, seeing its profit swinging from negative territory to low level. Under this circumstance, APT producers aimed to meet long term contracts, and barely refilled stocks. In addition, some halted production for several days to inventory stocks towards the end of the year. Therefore, APT output in December kept inching down.

In January, given year-end stockpiling may be weaker than expected, the operating rate of APT producers is unlikely to drop. It is expected that APT output may remain weak in January 2024.

Lithium carbonate

December saw domestic lithium carbonate production at 44,000 mt, up 2.08% MoM and 26.36% YoY. The 2023 total reached 460,000 mt, up 31.38% YoY. Production rose slightly for some spodumene-based lithium salt firms due to more processing orders, while certain lepidolite-based companies in Jiangxi boosted output substantially to clear year-end lepidolite inventories. New lithium salt enterprises also contributed to the modest production increase, collectively driving up December's lithium carbonate production.

Due to low temperatures impacting efficiency, salt lake lithium salt enterprises have cut production seasonally. Enterprises using recycled materials also see reduced output because of a drop in battery cell production waste leading to raw material scarcity and shrinking profit margins or even losses.

Starting January 2024, several spodumene-based lithium salt producers will enter maintenance in late January, slightly reducing output. Many small lepidolite-based smelters, already cutting orders since December with raw material cost issues, will close in mid-January for maintenance until after the Spring Festival, foreseeing continued output decline. Most salt lake enterprises will maintain stable production, with production ramp-up from a new Xinjiang enterprise. In contrast, battery scrap-based lithium salt producers, in the face of raw material shortages and cost issues, are likely to cut production. January's domestic lithium carbonate production is estimated at 41,700 mt, down 5.12% MoM but up 16.18% YoY.

Lithium hydroxide

China's December 2023 lithium hydroxide production was 20,330 mt, down 3% MoM and 20% YoY, amid weak market supply and demand. New production lines built by some manufacturers are still in the commissioning phase, causing slow industry capacity growth. Lithium hydroxide prices dropping below industrial-grade lithium carbonate prices keeps production profitability low, reducing the operating rates. With subcontracted orders ending, manufacturers' scheduled production is decreasing. As lithium carbonate prices stabilized in mid-to-late December, lithium hydroxide prices saw a slight uplift. Disruptions in the Red Sea route and domestic producers' pre-Spring Festival stockpiling spurred some demand, mildly boosting purchasing interest. Still, with high inventories and order uncertainty, cathode producers are buying cautiously, suggesting the oversupply may persist. SMM predicts China's January 2024 lithium hydroxide output at 18,720 mt, down 8% MoM and 12% YoY.

Cobalt sulphate

China's December cobalt sulphate production was 5,193 mt in metal content, down 10% MoM and 25% YoY due to slower demand recovery, causing inventory buildup and market oversupply. Despite lower product prices and the raw material inventory cycle, smelters faced losses, leading to continued production cuts and inventory reduction.

January may see a temporary cobalt sulphate demand spike due to improved orders for some firms, advanced production of February orders by ternary companies, and pre-holiday stockpiling, limiting production cuts. Expected January output is 5,109 mt in metal content, down 2% MoM and 19% YoY.

Tricobalt tetraoxide (Co3O4)

China's December Co3O4 production was 6,291 mt, down 5% MoM but up 26% YoY. The decrease is due to early demand fulfillment, with manufacturers clearing existing orders and few new orders coming in. Cobalt salt prices fell, reducing cost support and pushing Co3O4 prices down. This ongoing decline didn't boost sales, resulting in lower scheduled production at smelters.

January's low cobalt price is expected to boost market buying sentiment and, with pre-holiday restocking, Co3O4 orders will also impove, increasing smelter scheduled production. The forecasted output is 7,217 mt, up 15% MoM and 103% YoY.

Ternary cathode precursor

China's December ternary cathode precursor production was about 68,586 mt, down 2% MoM and 10% YoY. The 2023 total was 814,388 mt, down 5% YoY. As the year ended, some firms shipped more to hit targets, leading to increased production. Businesses also cut inventories, with December shipments exceeding production. Overseas demand in December was steady with slight growth as some manufacturers moved January orders to December. Domestic cathode demand was weak, causing inventory build-up. The share of mid-to-low nickel precursors dipped slightly, while that of high-nickel ones marginally rose, driven by stable export demand.

For January 2024, cathode material production is set to slightly drop by less than 1%, with precursor demand weakening as some manufacturers moved their procurement to December. Supply-side strategies for ternary cathode precursors are split. Some manufacturers cut production due to early shipments and weak demand, while others, expecting nickel and cobalt price lows and February's holiday, moved February production to January. January's estimated production in China is 66,094 mt, down 4% MoM but up 14% YoY.

Ternary cathode material

China's December 2023 ternary cathode material production was 53,181 mt, 5% down MoM and flat YoY. The 2023 total was 621,115 mt, down 5% YoY. In December, some cathode material suppliers that serve digital and power battery sectors used low-price shipments to maintain annual sales volumes. Power battery cathode manufacturers also reduced prices to compete for market share, challenging smaller producers. This led to a market split: financially strong enterprises sustained shipments, while smaller ones stopped production to clear inventory. EV market cathode production mirrored sales, generally declining as battery factories cut year-end stocks. A few firms bucked the trend, boosting production by advancing January export orders and through a minor rise in domestic orders. The share of mid-to-low nickel cathode materials fell, while that of high-nickel cathodes rose slightly.

In January 2024, the digital and EV batteries markets remain divided. Smaller producers keep reduced output or stay closed, whereas top firms in certain segments ramp up for February's demand, with scheduled production set to stay stable for now. January's ternary product orders in the EV market have exceeded low expectations. Demand rose due to December's low point and normal procurement after inventory digestion, shipping delays prompting overseas stockpiling, and better-than-expected domestic December car sales, slightly boosting ternary cathode demand. Leading battery cell factories see stable ternary product demand with a small rise in mid-to-high nickel cells while low-nickel cathode demand stays constant. Some second-tier factories expect a slight increase in mid-nickel battery cell demand. However, factories focused on overseas markets face weaker demand amid slower vehicle sales and product iteration issues.

On the supply side, January may see higher finished ternary cathode product stocks as some manufacturers boost production to cover February's holiday and maintenance downtime, pre-consuming February demand. Yet, expectations of falling lithium prices could alter downstream demand, risking order cuts from battery factories in January. China's production of ternary cathode materials in January 2024 is projected at 52,852 mt, down 0.62% MoM but up 30% YoY.

Iron phosphate

China's December iron phosphate output was 79,900 mt, down 24% MoM and 1% YoY, yet 2023 output was up 56% YoY. Lower LFP demand reduced iron phosphate production and sales. December saw LFP firms slow operating rates amid weak demand, cutting iron phosphate procurement. This forced producers to reduce or stop production, keeping inventories low and supply down. Despite stable raw material prices, negative profit margins dampened production incentives for iron phosphate businesses.

In January 2024's off-season, iron phosphate firms are likely to keep cutting operating rates. China's forecasted iron phosphate production for the month is 71,000 mt, down 11% MoM but up 14% YoY.

LFP

China's December LFP production was 95,010 mt, down 17% MoM and 6% YoY, but the full-year output rose 30% YoY. Weakened demand reduced LFP production. Falling primary raw material prices spurred destocking, prompting essential LFP purchases by battery cell companies. December saw key raw material prices like lithium carbonate and iron phosphate drop, lowering LFP manufacturing costs. LFP producers in December aligned production with sales, exercising caution with their scheduled production due to concerns about downstream order cancellations. These companies prioritized inventory reduction, maintaining production only to meet essential demand. Battery cell companies, especially in EV and energy storage, aiming to clear stock, extended delivery times and ordered less LFP material.

Q1 2024 is the industry's off-season with low LFP demand and market pessimism. The market is slow, and many LFP firms plan to begin their Spring Festival breaks 1-2 weeks early. Logistics limits during the festival cause January stockpiling. Estimated China's January 2024 LFP output is 97,310 mt, up 2% MoM and 51% YoY.

LCO

China's December LCO production was 6,326 mt, down 9% MoM but up 10% YoY. Declining Co3O4 and lithium carbonate prices reduced costs. In December's LCO off-season, downstream demand was weak, sparking fierce competition for orders, especially in the mid-to-low voltage segment, with frequent price cuts to win business. LCO manufacturers aimed to reduce stock, increase sales, and recover funds, leading to reduced production due to the dim demand outlook.

Downstream battery cell makers typically make long-term orders with occasional spot buys. January's pre-Spring Festival production push, considering cathode factories' 1-2 week February break, is expected to boost January scheduled production to prepare February stocks. The forecast for January is 7,092 mt, up 12% MoM and 125% YoY.

LMO

China's December 2023 LMO output was 5,113 mt, down 26% MoM and 25% YoY. Lithium carbonate spot prices, vital for LMO production, started stabilizing later in the month, offering better cost support for LMO cathodes. Year-end saw battery cell makers cutting costs and clearing inventory, pressuring LMO procurement prices. LMO producers with scant low-cost lithium carbonate reserves struggled to take orders, leaving only a few with cheap raw material stocks able to maintain production.

In January, few battery cell makers planned to stockpile before the festival, wary of lithium carbonate price stability and cautious about inventory levels. With some factories halting for maintenance, LMO demand looks set to keep falling. January's LMO production is estimated at 4,495 mt, down 12% MoM and 72% YoY.