SHANGHAI, Mar 31 (SMM) - This is a roundup of China's metals weekly inventory as of March 31.

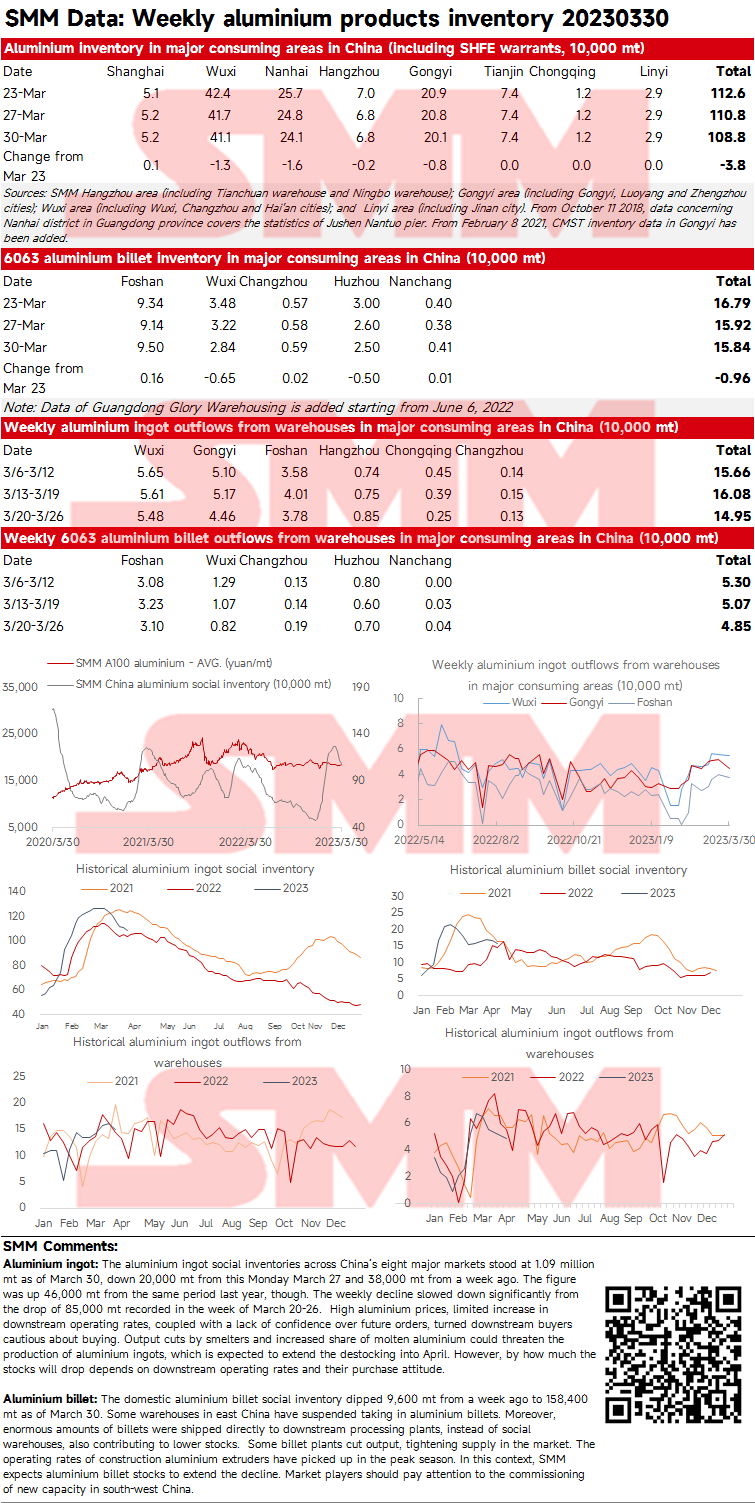

SMM Weekly Updates on China Aluminium Ingot and Billet Social Inventories as of March 30

Aluminium ingot: The aluminium ingot social inventories across China’s eight major markets stood at 1.09 million mt as of March 30, down 20,000 mt from this Monday March 27 and 38,000 mt from a week ago. The figure was up 46,000 mt from the same period last year, though. The weekly decline slowed down significantly from the drop of 85,000 mt recorded in the week of March 20-26. High aluminium prices, limited increase in downstream operating rates, coupled with a lack of confidence over future orders, turned downstream buyers cautious about buying. Output cuts by smelters and increased share of molten aluminium could threaten the production of aluminium ingots, which is expected to extend the destocking into April. However, by how much the stocks will drop depends on downstream operating rates and their purchase attitude.

Aluminium billet: The domestic aluminium billet social inventory dipped 9,600 mt from a week ago to 158,400 mt as of March 30. Some warehouses in east China have suspended taking in aluminium billets. Moreover, enormous amounts of billets were shipped directly to downstream processing plants, instead of social warehouses, also contributing to lower stocks. Some billet plants cut output, tightening supply in the market. The operating rates of construction aluminium extruders have picked up in the peak season. In this context, SMM expects aluminium billet stocks to extend the decline. Market players should pay attention to the commissioning of new capacity in south-west China.

Copper Inventory across Major Chinese Markets Increased This week

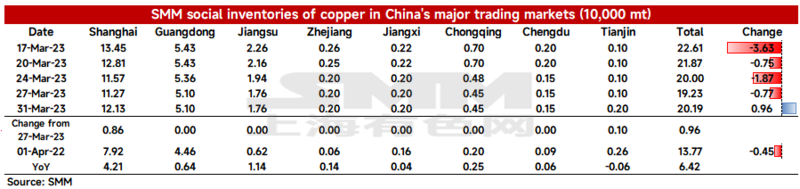

As of Friday March 31, SMM copper inventory across major Chinese markets stood at 201,900 mt, up 9,600 mt from Monday and 1,900 mt from last Friday. Total inventories added only 5,300mt from pre-CNY levels, snapping a destocking for four consecutive weeks. Compared with Monday, copper inventories increased across most regions. Total domestic inventories added 64,200 mt from 137,700 mt in the same period last year. Inventories in Shanghai were 42,100 mt higher than the same period last year, those in Guangdong were 6,400 mt higher, those in Jiangsu were 11,400 mt higher and those in Chongqing increased 2,500 mt.

In detail, the inventory in Shanghai grew 8,600 mt to 115,700 mt from Monday, and that in Tianjin increased 1,000 mt to 2,000 mt. Inventories in other regions changed little. Cash crunch at the month-end combined with continuous rise of copper prices weakened downstream buying interest. This can be reflected in the low daily average shipments from Guangdong. The influx of imported copper in Shanghai also accounted for higher inventory.

SMM understood that the customs clearance of imported copper will further increase next week, and the total supply is expected to increase compared with this week. In terms of consumption, the downstream purchasing enthusiasm at the beginning of the month will be stronger than this week, even as high copper prices will still restrain consumption. To sum up, SMM expects both supply and demand to increase next week. And inventory would grow further next week.

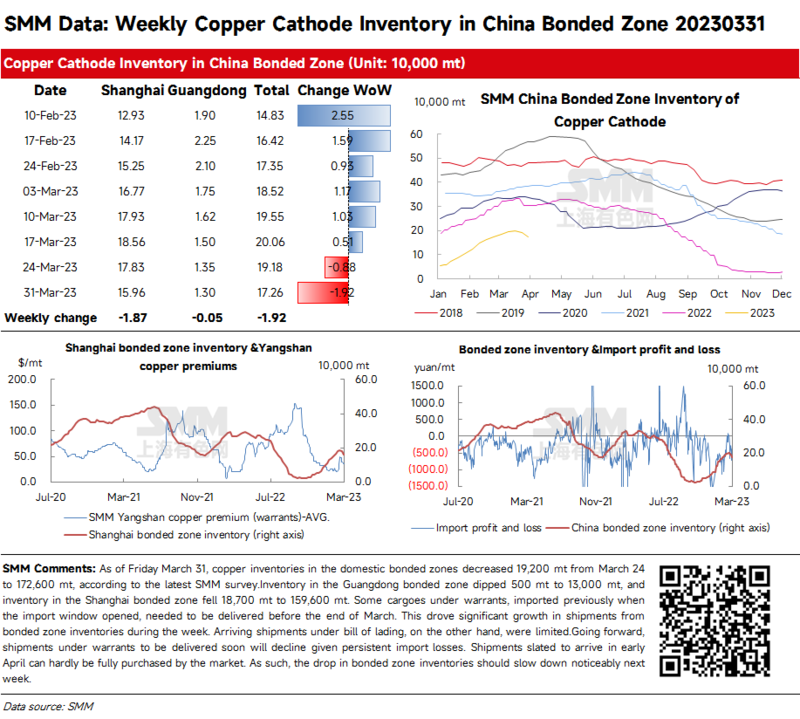

Copper Inventory in China Bonded Zone Fell Significantly This Week

As of Friday March 31, copper inventories in the domestic bonded zones decreased 19,200 mt from March 24 to 172,600 mt, according to the latest SMM survey. Inventory in the Guangdong bonded zone dipped 500 mt to 13,000 mt, and inventory in the Shanghai bonded zone fell 18,700 mt to 159,600 mt. Some cargoes under warrants, imported previously when the import window opened, needed to be delivered before the end of March. This drove significant growth in shipments from bonded zone inventories during the week. Arriving shipments under bill of lading, on the other hand, were limited. Going forward, shipments under warrants to be delivered soon will decline given persistent import losses. Shipments slated to arrive in early April can hardly be fully purchased by the market. As such, the drop in bonded zone inventories should slow down noticeably next week.

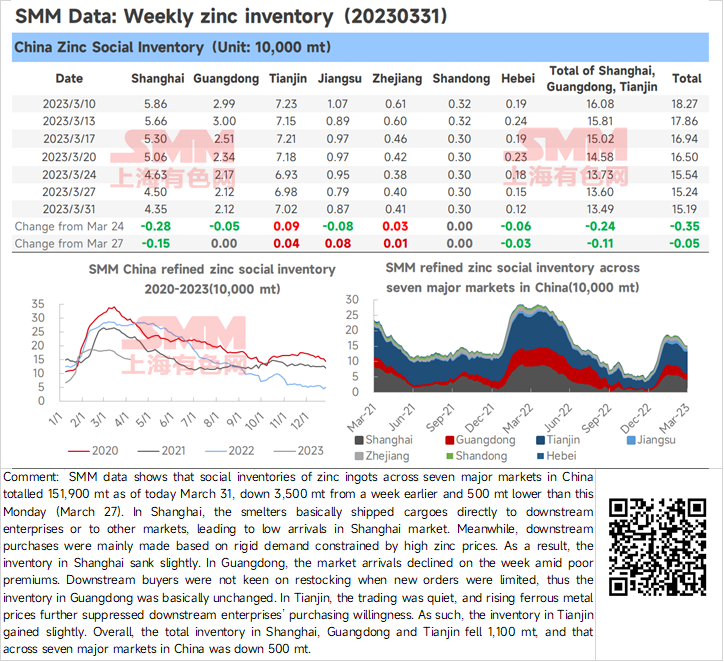

Zinc Ingot Inventory Down 500 mt from Monday

SMM data shows that social inventories of zinc ingots across seven major markets in China totalled 151,900 mt as of today March 31, down 3,500 mt from a week earlier and 500 mt lower than this Monday (March 27). In Shanghai, the smelters basically shipped cargoes directly to downstream enterprises or to other markets, leading to low arrivals in Shanghai market. Meanwhile, downstream purchases were mainly made based on rigid demand constrained by high zinc prices. As a result, the inventory in Shanghai sank slightly. In Guangdong, the market arrivals declined on the week amid poor premiums. Downstream buyers were not keen on restocking when new orders were limited, thus the inventory in Guangdong was basically unchanged. In Tianjin, the trading was quiet, and rising ferrous metal prices further suppressed downstream enterprises' purchasing willingness. As such, the inventory in Tianjin gained slightly. Overall, the total inventory in Shanghai, Guangdong and Tianjin fell 1,100 mt, and that across seven major markets in China was down 500 mt.

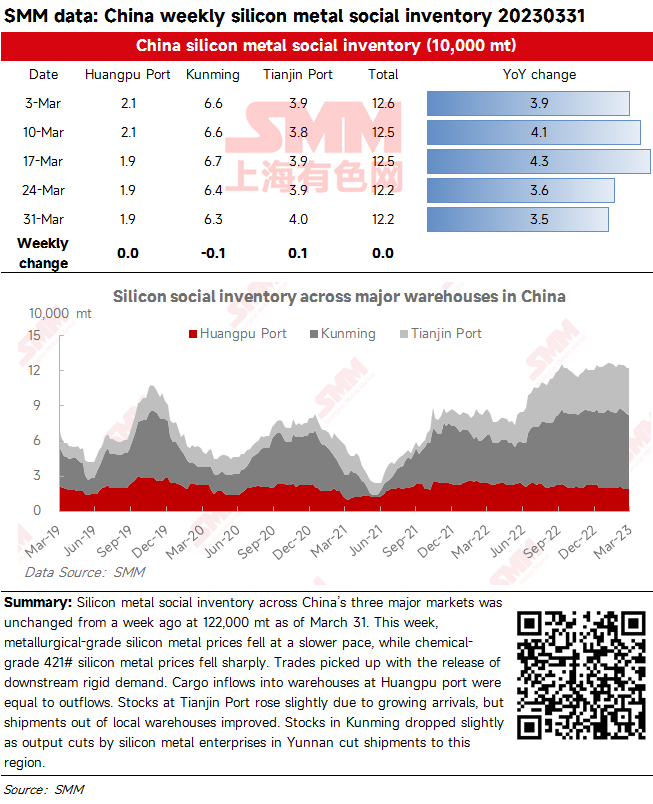

Silicon Metal Stocks Are Changed from A Week Ago, But Diverge by Region

SHANGHAI, Mar 31 (SMM) – Silicon metal social inventory across China’s three major markets was unchanged from a week ago at 122,000 mt as of March 31. This week, metallurgical-grade silicon metal prices fell at a slower pace, while chemical-grade 421# silicon metal prices fell sharply. Trades picked up with the release of downstream rigid demand. Cargo inflows into warehouses at Huangpu port were equal to outflows. Stocks at Tianjin Port rose slightly due to growing arrivals, but shipments out of local warehouses improved. Stocks in Kunming dropped slightly as output cuts by silicon metal enterprises in Yunnan cut shipments to this region.

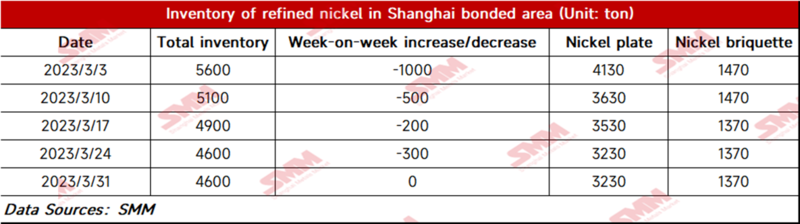

Pure Nickel Bonded Zone Inventory Remains Flat from Mar 24

As of March 31, bonded zone inventory of nickel stood flat WoW at 4,600 mt. The inventory of nickel briquettes was 1,370 mt, and that of nickel plates was 3,230 mt. SHFE/LME zinc price ratio fell due to the domestic and overseas futures prices. The downstream companies were not active in restocking. The spread between nickel briquette and nickel sulphate shrank on the fall in pure nickel prices, but the new energy sector did not release any nickel briquette demand.