SHANGHAI, Mar 3 (SMM) - This is a roundup of China's metals weekly inventory as of March 3.

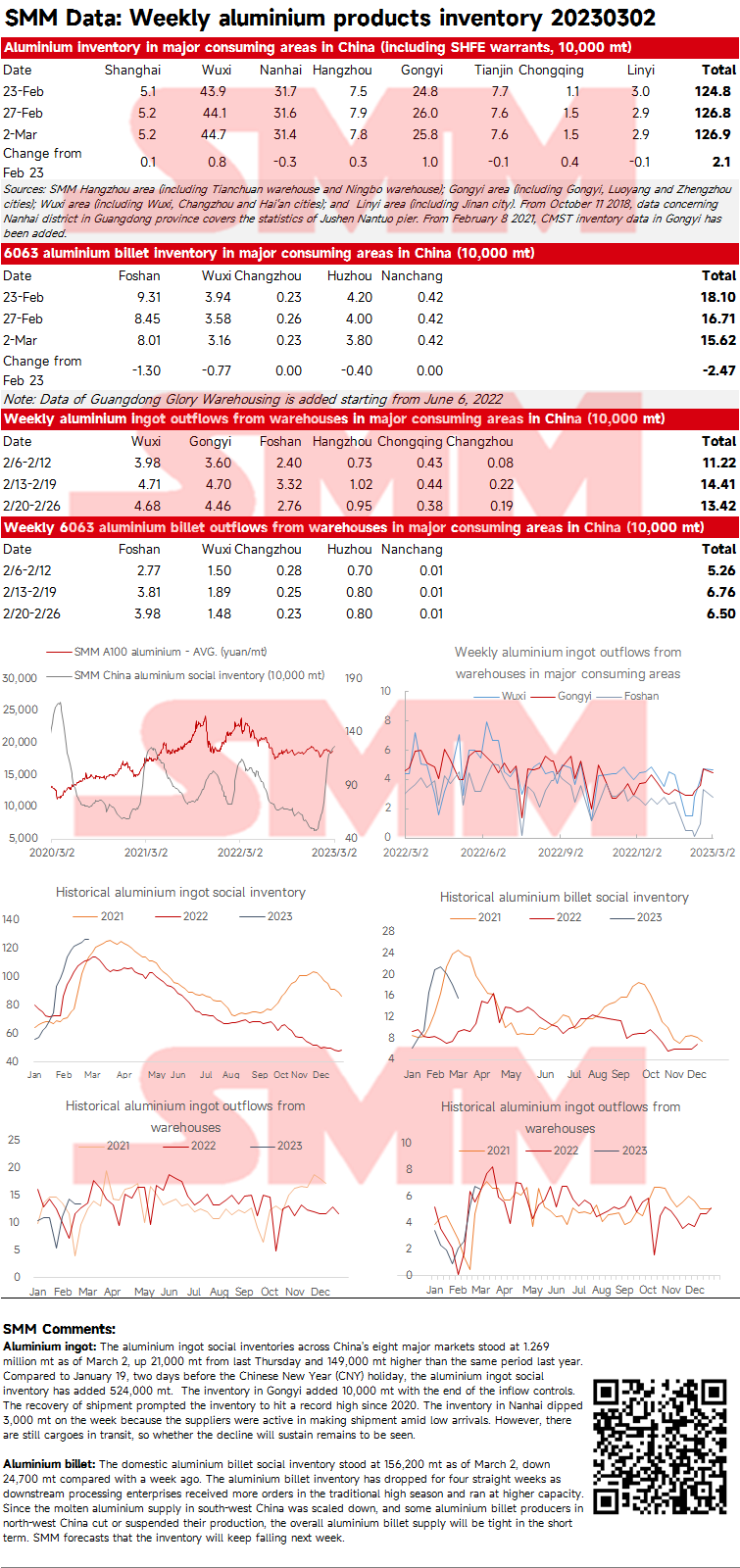

SMM Aluminium Social Inventory as of March 2

Aluminium ingot: The aluminium ingot social inventories across China's eight major markets stood at 1.269 million mt as of March 2, up 21,000 mt from last Thursday and 149,000 mt higher than the same period last year. Compared to January 19, two days before the Chinese New Year (CNY) holiday, the aluminium ingot social inventory has added 524,000 mt. The inventory in Gongyi added 10,000 mt with the end of the inflow controls. The recovery of shipment prompted the inventory to hit a record high since 2020. The inventory in Nanhai dipped 3,000 mt on the week because the suppliers were active in making shipment amid low arrivals. However, there are still cargoes in transit, so it remains to be seen whether the decline will sustain.

Aluminium billet: The domestic aluminium billet social inventory stood at 156,200 mt as of March 2, down 24,700 mt compared with a week ago. The aluminium billet inventory has dropped for four straight weeks as downstream processing enterprises received more orders in the traditional high season and ran at higher capacity. Since the molten aluminium supply in south-west China was scaled down, and some aluminium billet producers in north-west China cut or suspended their production, the overall aluminium billet supply will be tight in the short term. SMM forecasts that the inventory will keep falling next week.

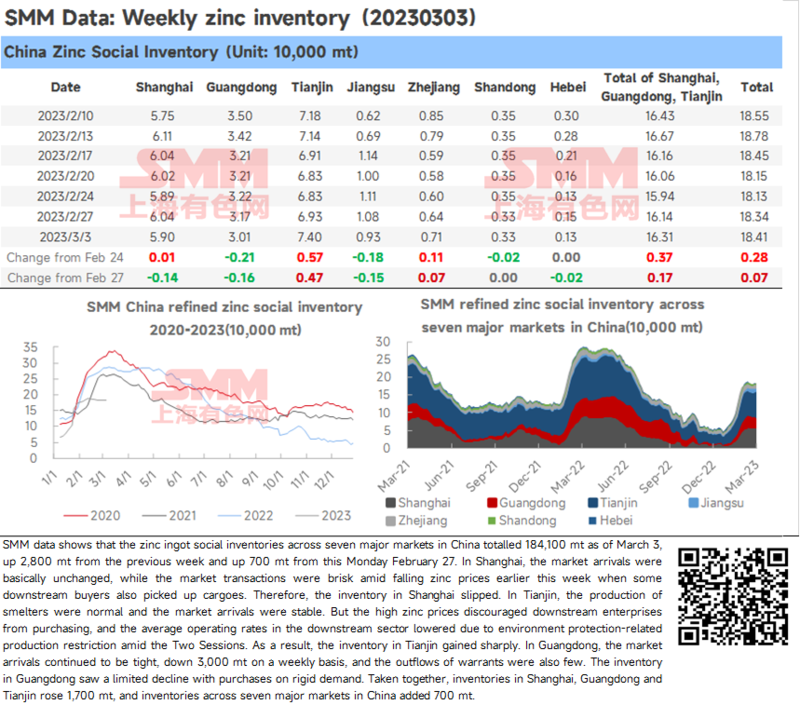

Zinc Ingot Social Inventory Up 700 mt from this Monday

SMM data shows that the zinc ingot social inventories across seven major markets in China totalled 184,100 mt as of March 3, up 2,800 mt from the previous week and up 700 mt from this Monday (February 27). In Shanghai, the market arrivals were basically unchanged, while the market transactions were brisk amid falling zinc prices earlier this week when some downstream buyers also picked up cargoes. Therefore, the inventory in Shanghai slipped. In Tianjin, the production of smelters were normal and the market arrivals were stable. But the high zinc prices discouraged downstream enterprises from purchasing, and the average operating rates in the downstream sector lowered due to environment protection-related production restriction amid the Two Sessions. As a result, the inventory in Tianjin gained sharply. In Guangdong, the market arrivals continued to be tight, down 3,000 mt on a weekly basis, and the outflows of warrants were also few. The inventory in Guangdong saw a limited decline with purchases on rigid demand. Taken together, inventories in Shanghai, Guangdong and Tianjin rose 1,700 mt, and inventories across seven major markets in China added 700 mt.

Silicon Metal Social Stocks Climb Slightly amid Weak Demand

SHANGHAI, Mar 3 (SMM) - Silicon metal stocks across China’s three major markets stood at 126,000 mt as of March 3, up 3,000 mt from a week ago. The growth was contributed by Kunming and Huangpu Port, while inventory at Tianjin Port increased by about 400 mt. The negotiations between upstream and downstream enterprises were in a stalemate. Silicon metal sellers lowered their quotations under selling pressure. The operating rates of silicon metal plants were high, while downstream buyers restocked on demand.

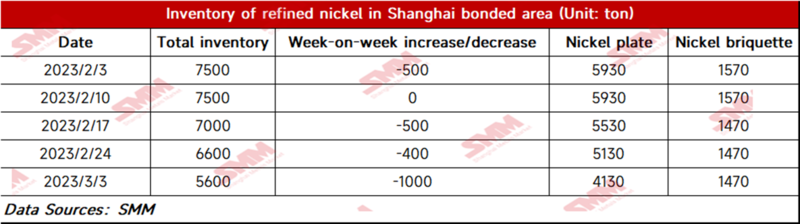

Bonded Zone Inventory of Nickel Drops Slightly from February 24

Bonded zone inventory of nickel dropped 1,000 mt to 5,600 mt WoW as of March 3, with the inventory of nickel briquettes and nickel plates standing at 1,470 mt and 4,130 mt respectively. Nickel plate inventory fell more in the week as the import window was still open and the spot transactions picked up slightly amid the dropping nickel prices. Nickel briquette demand from the stainless steel sector was low, thus the bonded zone inventory of nickel briquettes stood flat WoW this week.

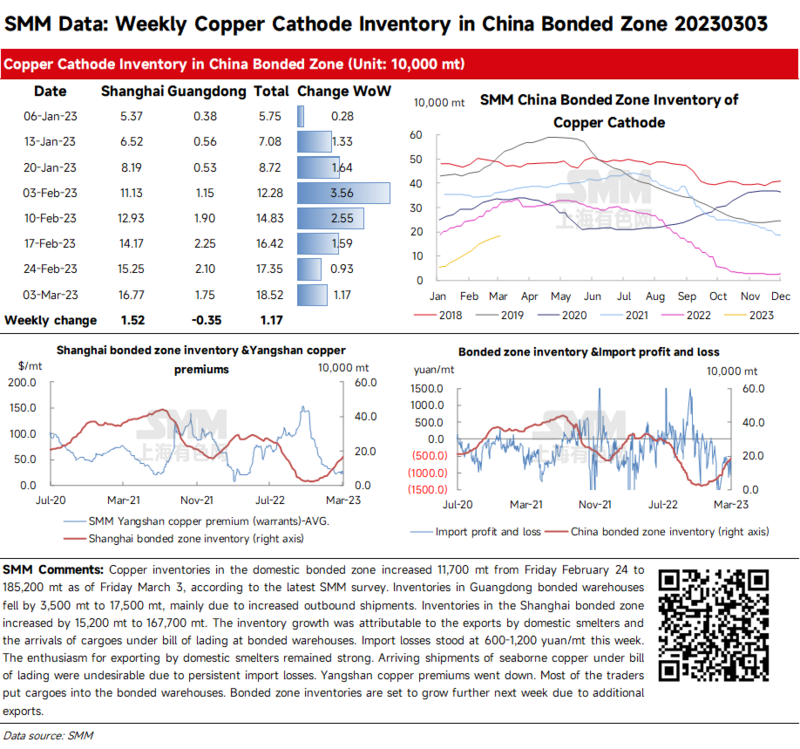

Copper Inventories in Chinese Bonded Zone Increased This Week

Copper inventories in the domestic bonded zone increased 11,700 mt from Friday February 24 to 185,200 mt as of Friday March 3, according to the latest SMM survey.

Inventories in Guangdong bonded warehouses fell by 3,500 mt to 17,500 mt, mainly due to increased outbound shipments. Inventories in the Shanghai bonded zone increased by 15,200 mt to 167,700 mt. The inventory growth was attributable to the exports by domestic smelters and the arrivals of cargoes under bill of lading at bonded warehouses.

Import losses stood at 600-1,200 yuan/mt this week. The enthusiasm for exporting by domestic smelters remained strong. Arriving shipments of seaborne copper under bill of lading were undesirable due to persistent import losses. Yangshan copper premiums went down. Most of the traders put cargoes into the bonded warehouses. Bonded zone inventories are set to grow further next week due to additional exports.

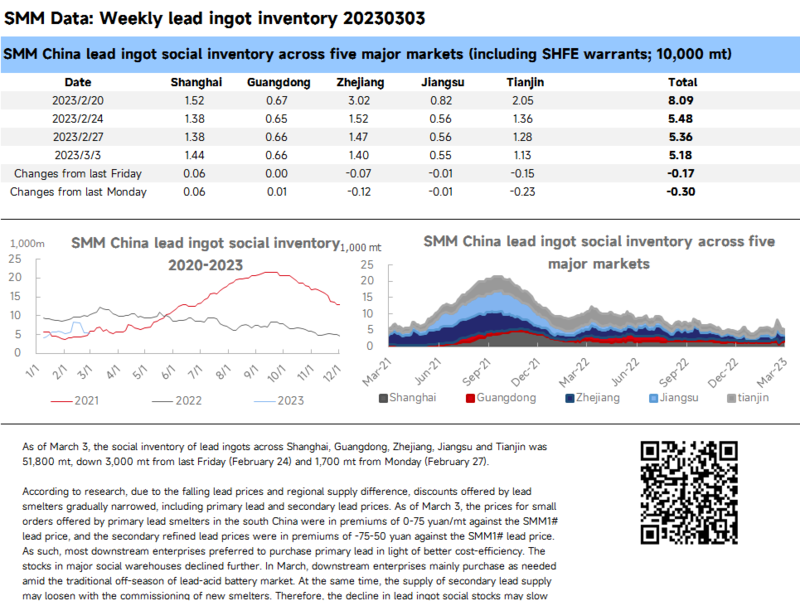

Tight Regional Supply and High Secondary Lead Prices Drives Lead Ingot Social Inventory to Decline

As of March 3, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 51,800 mt, down 3,000 mt from last Friday (February 24) and 1,700 mt from Monday (February 27).

According to research, due to the falling lead prices and regional supply difference, discounts offered by lead smelters gradually narrowed, including primary lead and secondary lead prices. As of March 3, the prices for small orders offered by primary lead smelters in the south China were in premiums of 0-75 yuan/mt against the SMM1# lead price, and the secondary refined lead prices were in premiums of -75-50 yuan against the SMM1# lead price. As such, most downstream enterprises preferred to purchase primary lead in light of better cost-efficiency. The stocks in major social warehouses declined further. In March, downstream enterprises mainly purchase as needed amid the traditional off-season of lead-acid battery market. At the same time, the supply of secondary lead supply may loosen with the commissioning of new smelters. Therefore, the decline in lead ingot social stocks may slow down.