SHANGHAI, Jan 13 (SMM) - This is a roundup of China's metals weekly inventory as of January 13.

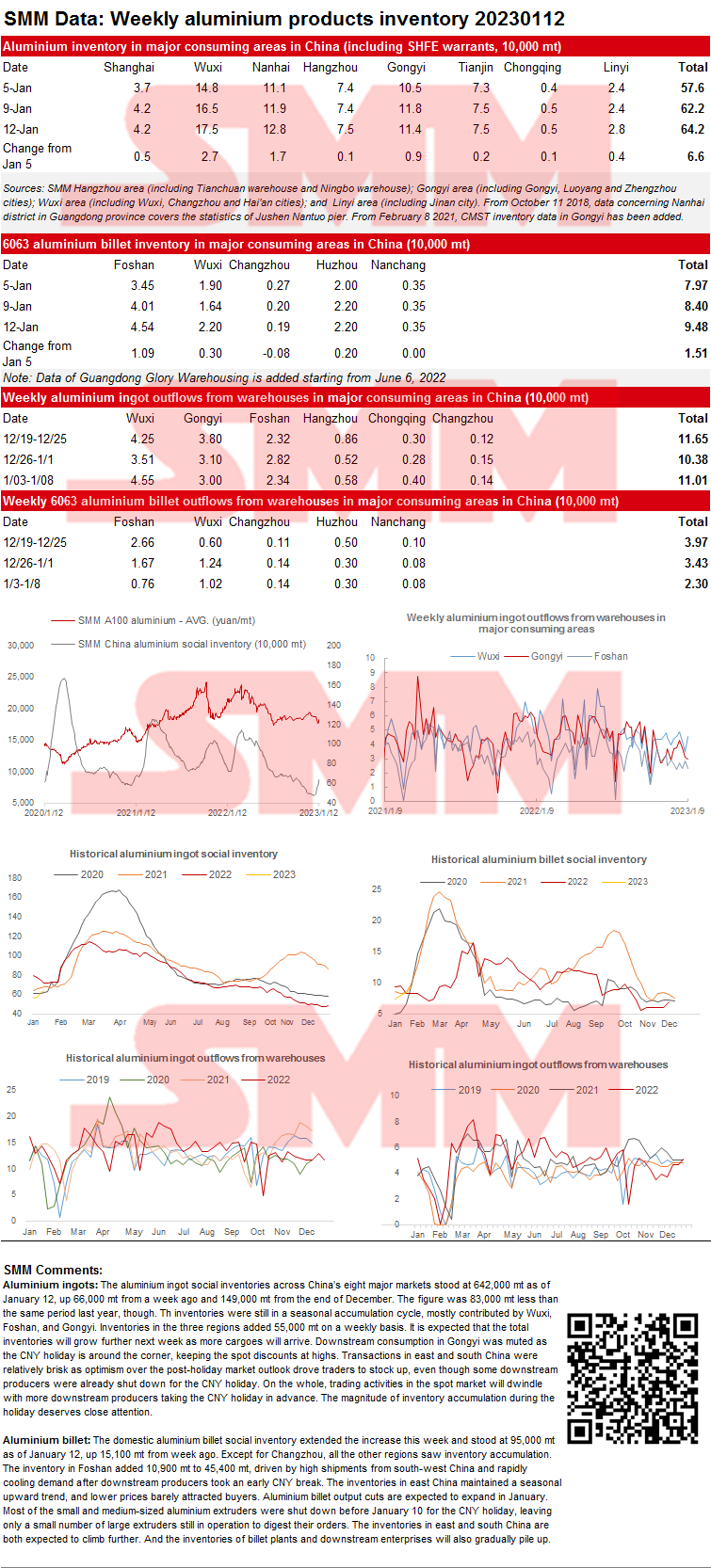

SMM Aluminium Ingot and Billet Social Inventories in China as of January 12

Aluminium ingots: The aluminium ingot social inventories across China’s eight major markets stood at 642,000 mt as of January 12, up 66,000 mt from a week ago and 149,000 mt from the end of December. The figure was 83,000 mt less than the same period last year, though. Th inventories were still in a seasonal accumulation cycle, mostly contributed by Wuxi, Foshan, and Gongyi. Inventories in the three regions added 55,000 mt on a weekly basis. It is expected that the total inventories will grow further next week as more cargoes will arrive. Downstream consumption in Gongyi was muted as the CNY holiday is around the corner, keeping the spot discounts at highs. Transactions in east and south China were relatively brisk as optimism over the post-holiday market outlook drove traders to stock up, even though some downstream producers were already shut down for the CNY holiday. On the whole, trading activities in the spot market will dwindle with more downstream producers taking the CNY holiday in advance. The magnitude of inventory accumulation during the holiday deserves close attention.

Aluminium billet: The domestic aluminium billet social inventory extended the increase this week and stood at 95,000 mt as of January 12, up 15,100 mt from week ago. Except for Changzhou, all the other regions saw inventory accumulation. The inventory in Foshan added 10,900 mt to 45,400 mt, driven by high shipments from south-west China and rapidly cooling demand after downstream producers took an early CNY break. The inventories in east China maintained a seasonal upward trend, and lower prices barely attracted buyers. Aluminium billet output cuts are expected to expand in January. Most of the small and medium-sized aluminium extruders were shut down before January 10 for the CNY holiday, leaving only a small number of large extruders still in operation to digest their orders. The inventories in east and south China are both expected to climb further. And the inventories of billet plants and downstream enterprises will also gradually pile up.

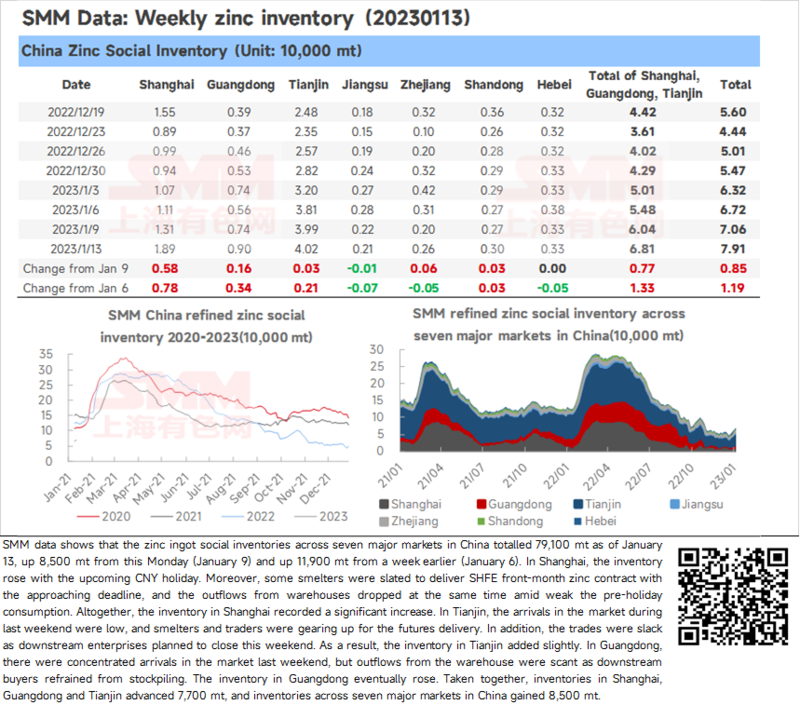

Zinc Ingot Social Inventory Gains 8,500 mt from this Monday

SMM data shows that the zinc ingot social inventories across seven major markets in China totalled 79,100 mt as of January 13, up 8,500 mt from this Monday (January 9) and up 11,900 mt from a week earlier (January 6). In Shanghai, the inventory rose with the upcoming CNY holiday. Moreover, some smelters were slated to deliver SHFE front-month zinc contract with the approaching deadline, and the outflows from warehouses dropped at the same time amid weak the pre-holiday consumption. Altogether, the inventory in Shanghai recorded a significant increase. In Tianjin, the arrivals in the market during last weekend were low, and smelters and traders were gearing up for the futures delivery. In addition, the trades were slack as downstream enterprises planned to close this weekend. As a result, the inventory in Tianjin added slightly. In Guangdong, there were concentrated arrivals in the market last weekend, but outflows from the warehouse were scant as downstream buyers refrained from stockpiling. The inventory in Guangdong eventually rose. Taken together, inventories in Shanghai, Guangdong and Tianjin advanced 7,700 mt, and inventories across seven major markets in China gained 8,500 mt.

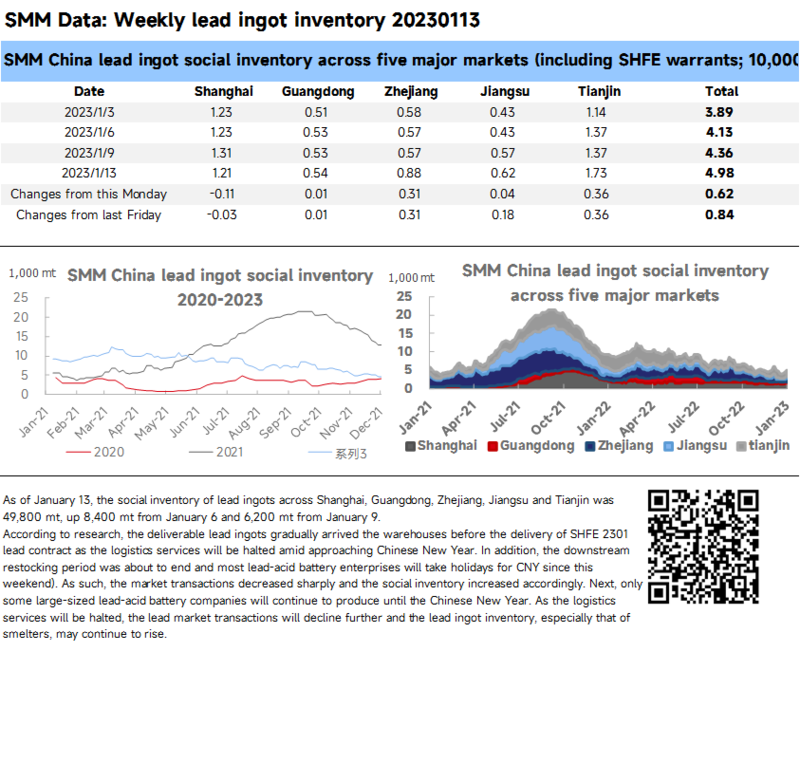

Social Inventory of Lead Ingot Increased Sharply amid the Approaching Delivery of SHFE 2301 Lead Contract and the Chinese New Year

As of January 13, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 49,800 mt, up 8,400 mt from January 6 and 6,200 mt from January 9.

According to research, the deliverable lead ingots gradually arrived the warehouses before the delivery of SHFE 2301 lead contract as the logistics services will be halted amid approaching Chinese New Year. In addition, the downstream restocking period was about to end and most lead-acid battery enterprises will take holidays for CNY since this weekend). As such, the market transactions decreased sharply and the social inventory increased accordingly. Next, only some large-sized lead-acid battery companies will continue to produce until the Chinese New Year. As the logistics services will be halted, the lead market transactions will decline further and the lead ingot inventory, especially that of smelters, may continue to rise.

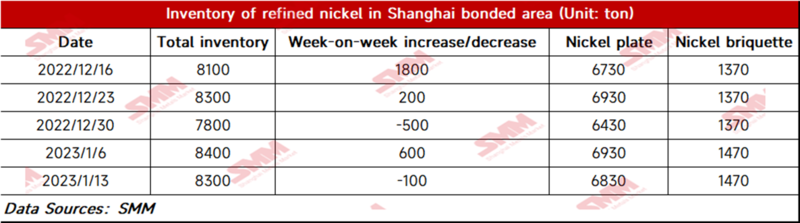

Bonded Zone Inventory of Nickel Drops Slightly from January 6

As of January 13, bonded zone inventory of nickel dropped to 8,300 mt, with the inventory of nickel briquettes and nickel plates of 1,470 mt and 6,830 mt respectively. The import window has been closed for two months. LME nickel prices dropped this week, pushing up the SHFE/LME nickel price ratio. The spot imports could gain profits. According to SMM research, some imported pure nickel has been cleared and shipped to the Chinese market.

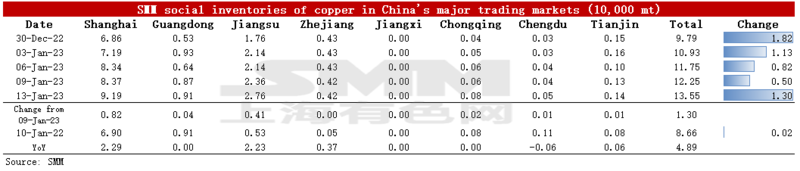

Copper Inventories in Major Chinese Markets Add 13,000 mt from Monday

As of Friday January 13, SMM copper inventory across major Chinese markets stood at 135,500 mt, up 13,000 mt from Monday and 18,000 mt from last Friday. The inventory has increased for three consecutive weeks since the end of December, which was caused by the poor downstream consumption. Compared with Monday's data, the inventories across various regions grew this week. The total inventory was 48,900 mt higher than in the same period last year when the figure was 86,600 mt. Among them, the inventory in Shanghai added 22,900 mt YoY, that in Guangdong stood flat, that in Jiangsu grew 22,300 mt, and that in Zhejiang rose 3,700 mt.

In detail, the inventory in Shanghai increased 8,200 mt to 91,900 mt compared with Monday, and the inventory in Jiangsu added 4,100 mt to 27,600 mt. Smelters in north China shipped their goods actively to the east before the delivery of the SHFE 2301 copper, which contributed to the growth of inventory in east China. Inventory in Guangdong rose 400 mt to 9,100 mt. Production of the nearby smelters has not grown to the normal level despite the end of the overhaul. Besides, the transportation of goods was delayed at the year-end. In addition, the demand decreased as most downstream companies in Guangdong have taken their Chinese New Year holiday, which can also be reflected in the recent continuous decline in the average daily shipments flowing out of the warehouses in Guangdong. In general, the copper supply and demand in the Guangdong market were both weak.

Looking forward, the arrival of imported copper will be low WoW next week, but that of domestic copper will grow somewhat, the SMM survey shows. The overall supply is expected to increase compared with this week as the smelters will increase their shipments to the warehouses approaching the delivery of SHFE 2301 copper while the downstream consumption will reduce. The consumption will decline greatly next week since the downstream companies will have the CNY holiday one after another. SMM believes that the supply will grow while the consumption may decrease next week, thus the inventory will increase further.

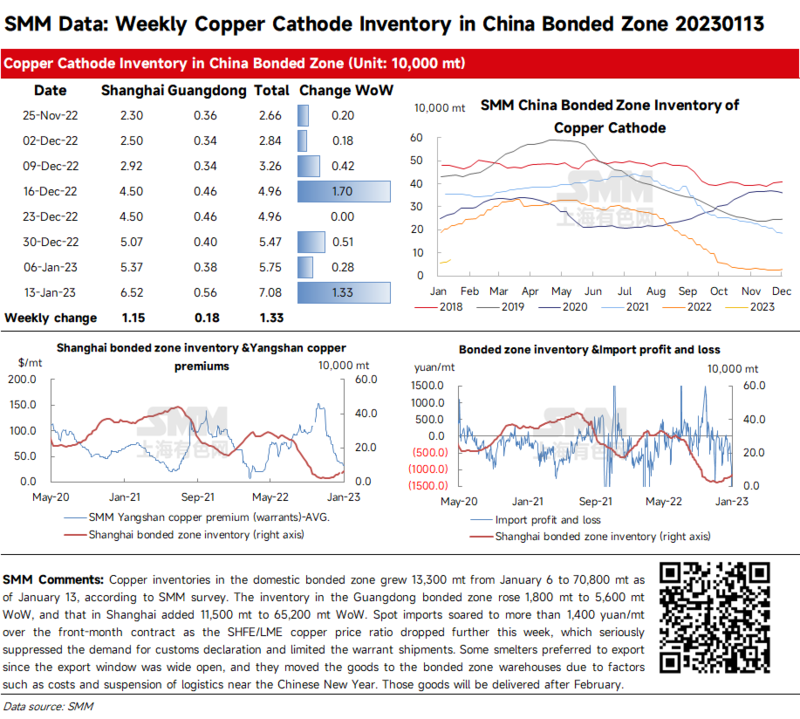

Copper Inventories in Domestic Bonded Zone Add 13,300 mt from January 6

Copper inventories in the domestic bonded zone grew 13,300 mt from January 6 to 70,800 mt as of January 13, according to SMM survey. The inventory in the Guangdong bonded zone rose 1,800 mt to 5,600 mt WoW, and that in Shanghai added 11,500 mt to 65,200 mt WoW. Spot imports soared to more than 1,400 yuan/mt over the front-month contract as the SHFE/LME copper price ratio dropped further this week, which seriously suppressed the demand for customs declaration and limited the warrant shipments. Some smelters preferred to export since the export window was wide open, and they moved the goods to the bonded zone warehouses due to factors such as costs and suspension of logistics near the Chinese New Year. Those goods will be delivered after February.

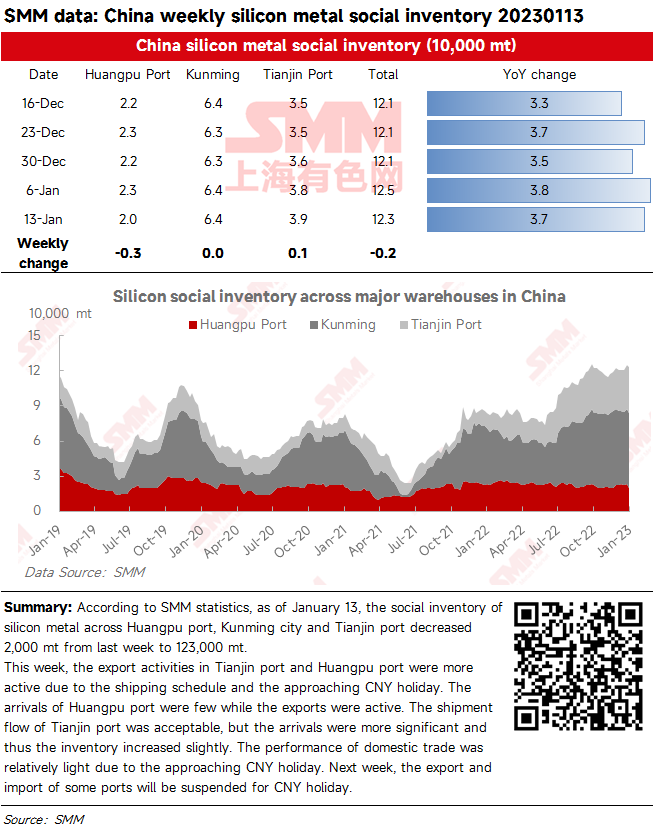

Social Inventory of Silicon Metal Declined Slightly amid the Active Export Activities

According to SMM statistics, as of January 13, the social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port decreased 2,000 mt from last week to 123,000 mt.

This week, the export activities in Tianjin port and Huangpu port were more active due to the shipping schedule and the approaching CNY holiday. The arrivals of Huangpu port were few while the exports were active. The shipment flow of Tianjin port was acceptable, but the arrivals were more significant and thus the inventory increased slightly. The performance of domestic trade was relatively light due to the approaching CNY holiday. Next week, the export and import of some ports will be suspended for CNY holiday.