SHANGHAI, Dec 2 (SMM) - This is a roundup of China's metals weekly inventory as of December 2.

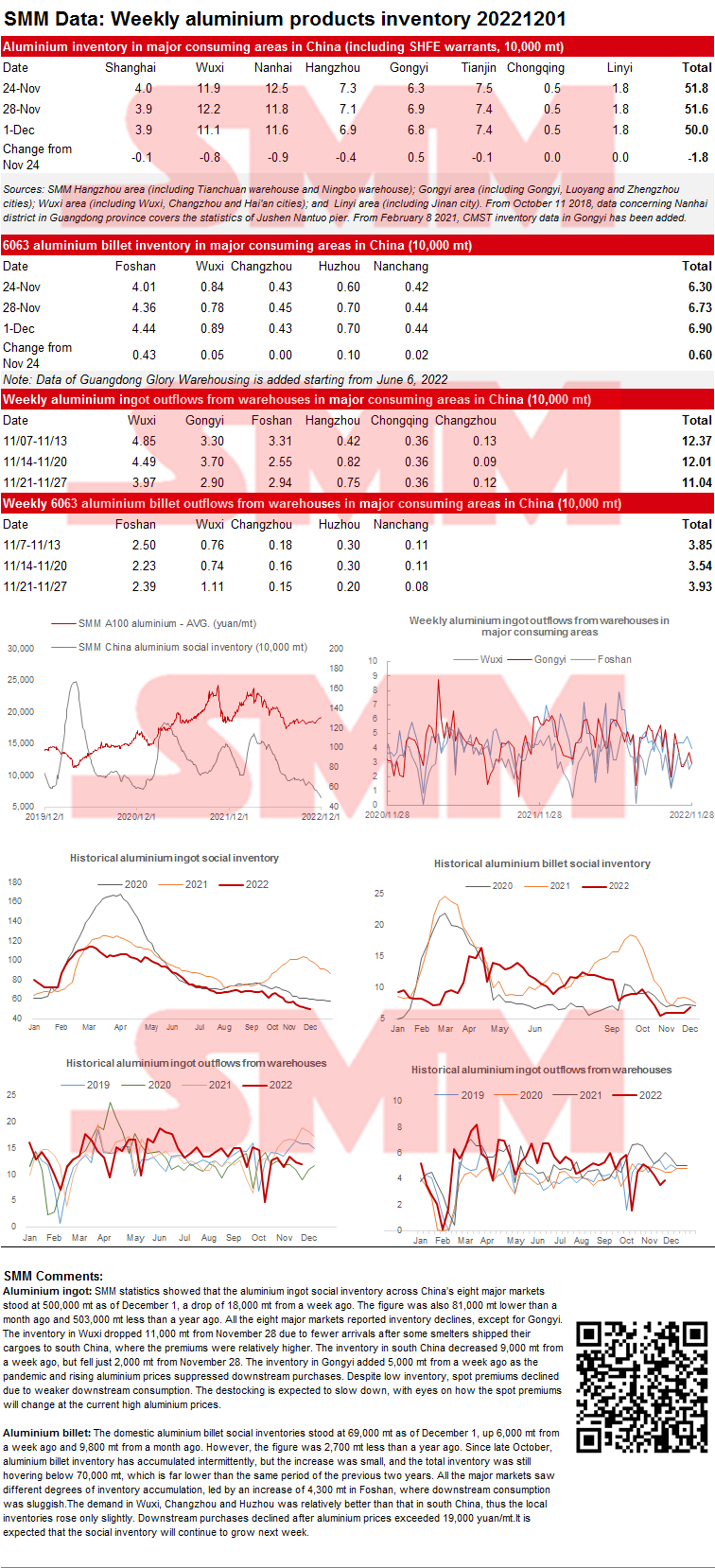

SMM China Aluminum Ingot and Billet Social Inventory as of December 1

Aluminium ingot: SMM statistics showed that the aluminium ingot social inventory across China’s eight major markets stood at 500,000 mt as of December 1, a drop of 18,000 mt from a week ago. The figure was also 81,000 mt lower than a month ago and 503,000 mt less than a year ago. All the eight major markets reported inventory declines, except for Gongyi. The inventory in Wuxi dropped 11,000 mt from November 28 due to fewer arrivals after some smelters shipped their cargoes to south China, where the premiums were relatively higher. The inventory in south China decreased 9,000 mt from a week ago, but fell just 2,000 mt from November 28. The inventory in Gongyi added 5,000 mt from a week ago as the pandemic and rising aluminium prices suppressed downstream purchases. Despite low inventory, spot premiums declined due to weaker downstream consumption. The destocking is expected to slow down, with eyes on how the spot premiums will change at the current high aluminium prices.

Aluminium billet: The domestic aluminium billet social inventories stood at 69,000 mt as of December 1, up 6,000 mt from a week ago and 9,800 mt from a month ago. However, the figure was 2,700 mt less than a year ago. Since late October, aluminium billet inventory has accumulated intermittently, but the increase was small, and the total inventory was still hovering below 70,000 mt, which is far lower than the same period of the previous two years. All the major markets saw different degrees of inventory accumulation, led by an increase of 4,300 mt in Foshan, where downstream consumption was sluggish.The demand in Wuxi, Changzhou and Huzhou was relatively better than that in south China, thus the local inventories rose only slightly. Downstream purchases declined after aluminium prices exceeded 19,000 yuan/mt.It is expected that the social inventory will continue to grow next week.

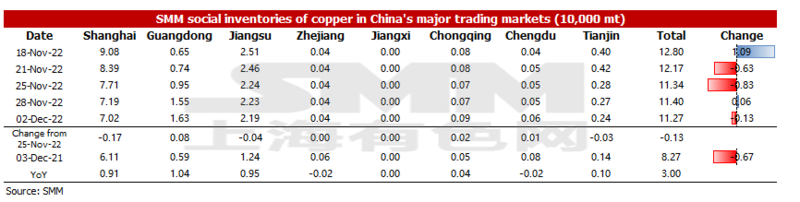

Copper Inventory in Major Chinese Markets Dips 1,300 mt from Monday

As of Friday December 2, SMM copper inventory across major Chinese markets stood at 112,700 mt, down 1,300 mt from Monday and 700 mt from last Friday. Compared with Monday’s data, the inventories in east China and Tianjin declined, while those in the south and south-west China grew slightly. The total inventory was 30,000 mt higher than in the same period last year when the figure was 82,700 mt. Among them, the inventory in Shanghai added 9,100 mt, that in Guangdong grew 10,400 mt, and that in Jiangsu rose 9,500 mt.

In detail, the inventory in Shanghai dropped 1,700 mt to 70,200 mt compared with Monday, and that in Jiangsu fell 400 mt to 21,900 mt. The arrivals of imported and domestic copper were limited this week, and downstream companies increased their purchases in December. Inventory in Guangdong added 800 mt to 16,300 mt. On one hand, the surrounding smelters resumed their normal production and increased their shipments. On the other hand, the overall consumption in Guangdong was poor, which is reflected in the low average daily shipment flowing out of the warehouses in Guangdong.

Looking forward, the arrival of imported copper will rise this week, but that of domestic copper will not grow sharply, the SMM survey shows. The overall supply will be higher than this week. Consumption may recover slightly amid the relaxation of COVID-19 control measures in various regions. The inventory next week will drop slightly amid the growing supply and demand.

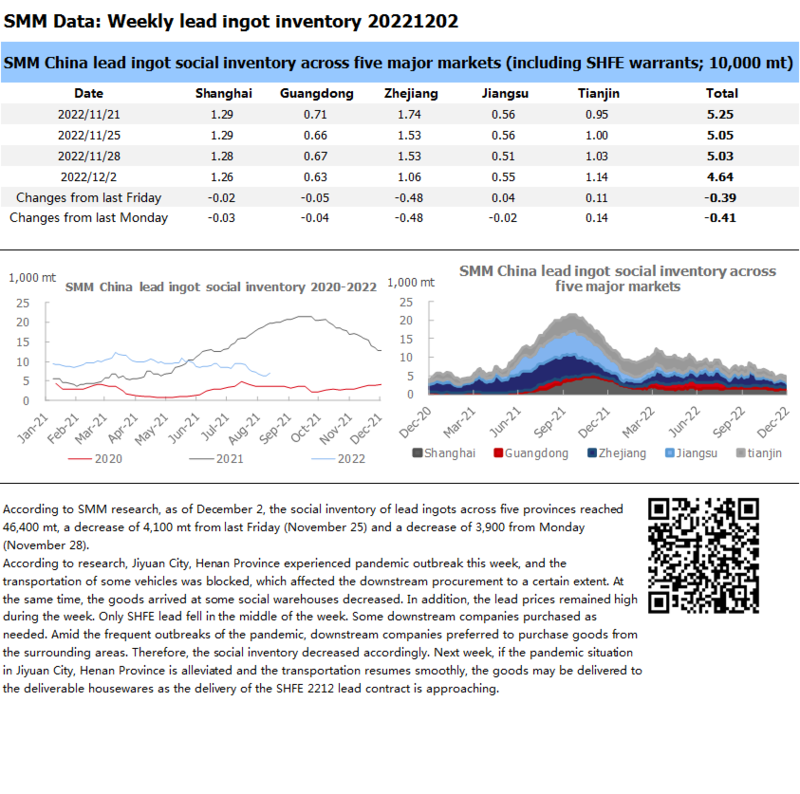

Social Inventory of Lead Ingots Declines as Pandemic Affects Transportation

According to SMM research, as of December 2, the social inventory of lead ingots across five provinces reached 46,400 mt, a decrease of 4,100 mt from last Friday (November 25) and a decrease of 3,900 from Monday (November 28).

According to research, Jiyuan City, Henan Province experienced pandemic outbreak this week, and the transportation of some vehicles was blocked, which affected the downstream procurement to a certain extent. At the same time, the goods arrived at some social warehouses decreased. In addition, the lead prices remained high during the week. Only SHFE lead fell in the middle of the week. Some downstream companies purchased as needed. Amid the frequent outbreaks of the pandemic, downstream companies preferred to purchase goods from the surrounding areas. Therefore, the social inventory decreased accordingly. Next week, if the pandemic situation in Jiyuan City, Henan Province is alleviated and the transportation resumes smoothly, the goods may be delivered to the deliverable housewares as the delivery of the SHFE 2212 lead contract is approaching.

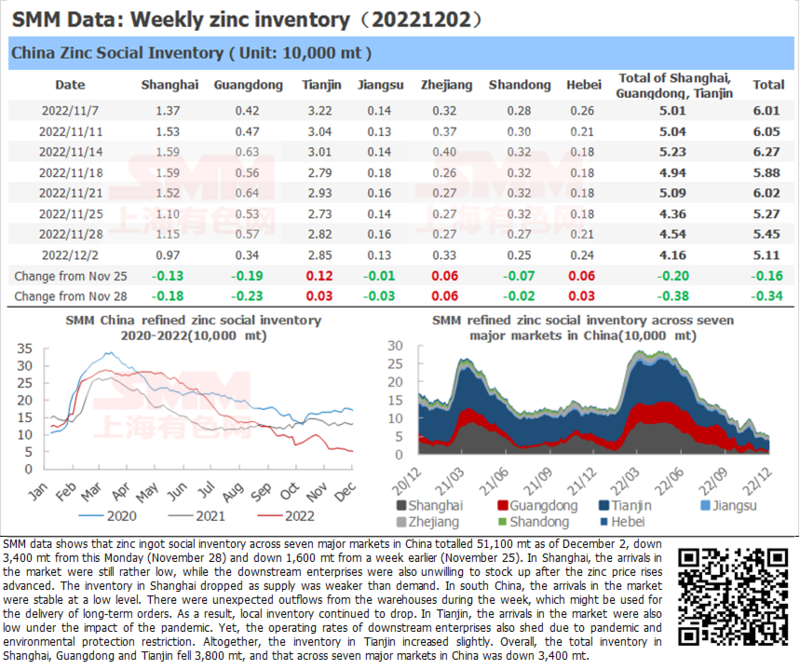

Zinc Ingot Social Inventory Down 3,400 mt from this Monday

SMM data shows that zinc ingot social inventory across seven major markets in China totalled 51,100 mt as of December 2, down 3,400 mt from this Monday (November 28) and down 1,600 mt from a week earlier (November 25). In Shanghai, the arrivals in the market were still rather low, while the downstream enterprises were also unwilling to stock up after the zinc price rises advanced. The inventory in Shanghai dropped as supply was weaker than demand. In south China, the arrivals in the market were stable at a low level. There were unexpected outflows from the warehouses during the week, which might be used for the delivery of long-term orders. As a result, local inventory continued to drop. In Tianjin, the arrivals in the market were also low under the impact of the pandemic. Yet, the operating rates of downstream enterprises also shed due to pandemic and environmental protection restriction. Altogether, the inventory in Tianjin increased slightly. Overall, the total inventory in Shanghai, Guangdong and Tianjin fell 3,800 mt, and that across seven major markets in China was down 3,400 mt.

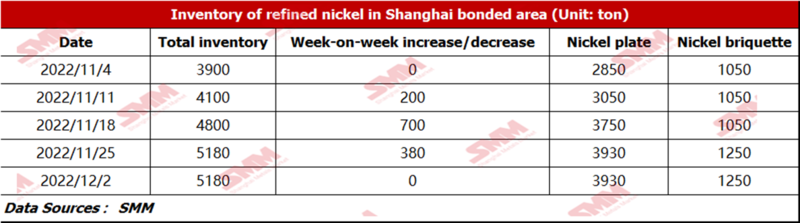

Bonded Zone Inventory of Nickel Stays Unchanged from November 25

As of December 2, bonded zone inventory of nickel stood flat WoW at 5,180 mt. The inventory of nickel briquette was 1,250 mt, and that of nickel plate was 3,930 mt. The SHFE/LME price ratio remained at 7.5-7.6 within the week, and the spot import losses stood at around 20,000 yuan/mt. In addition, the downstream demand for pure nickel continued to be poor, so there was almost no customs clearance for pure nickel in the bonded zone this week.

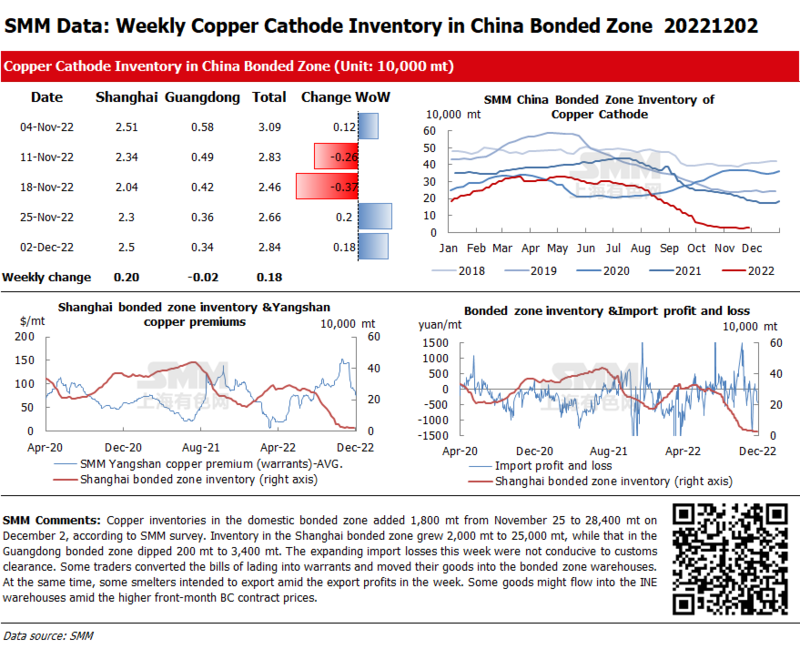

Copper Inventories in Domestic Bonded Zones Up 1,800 mt from November 25

Copper inventories in the domestic bonded zone added 1,800 mt from November 25 to 28,400 mt on December 2, according to SMM survey. Inventory in the Shanghai bonded zone grew 2,000 mt to 25,000 mt, while that in the Guangdong bonded zone dipped 200 mt to 3,400 mt. The expanding import losses this week were not conducive to customs clearance. Some traders converted the bills of lading into warrants and moved their goods into the bonded zone warehouses. At the same time, some smelters intended to export amid the export profits in the week. Some goods might flow into the INE warehouses amid the higher front-month BC contract prices.

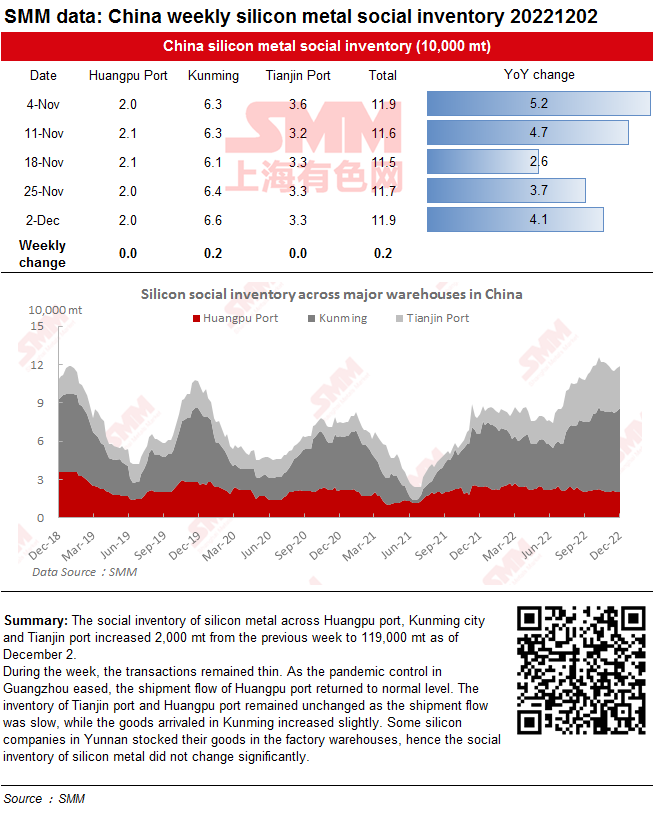

Social Inventory of Silicon Metal Increases as the Transactions Remain Thin

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port totalled 119,000 mt as of December 2, up 2,000 mt on the week.

During the week, the transactions remained thin. As the pandemic control in Guangzhou eased, the shipment flow of Huangpu port returned to normal level. The inventory of Tianjin port and Huangpu port remained unchanged as the shipment flow was slow, while the goods arrivaled in Kunming increased slightly. Some silicon companies in Yunnan stocked their goods in the factory warehouses, hence the social inventory of silicon metal did not change significantly.

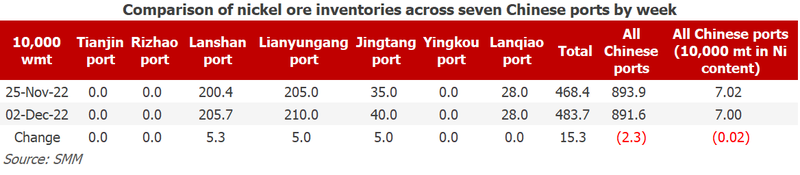

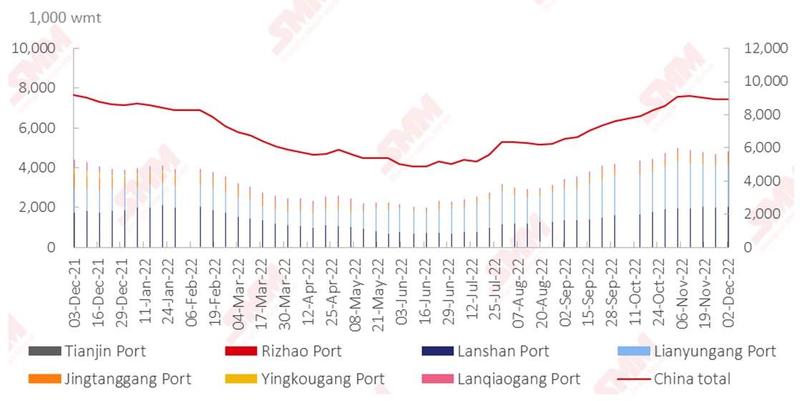

Nickel Ore Inventories at Chinese Ports Down 23,000 wmt WoW

As of December 2, inventory of nickel ore across Chinese ports dipped 23,000 wmt to 8.92 million wmt compared with last Friday. The total Ni content stood at around 70,000 mt. Port inventory of nickel ore across seven major Chinese ports stood at 4.84 million wmt, 153,000 wmt higher than last week. On the demand side, NPI plants suffered losses amid the falling NPI prices. Besides, steel mills cut their production, thus the NPI plants became less willing to produce, reducing the nickel ore demand. On the supply side, recently, the shipments flowing out of the ports in the Philippines have gradually decreased, and the inflow of nickel ore to the Chinese market has declined. It is expected that the stock of nickel ore at ports will continue to decline in the future, but the import volume from other countries and regions such as New Caledonia will be relatively considerable. In addition, the consumption of nickel ore at NPI plants will be limited. Port inventory of nickel ore may fall limitedly in the short term.

![[SMM Analysis] Futures Lack Momentum to Rise Further, Pre-Holiday Demand Stalls, and Stainless Steel Social Inventory Accumulation Intensifies](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)