SHANGHAI, Aug 26 (SMM) - This is a roundup of China's metals weekly inventory as of August 26.

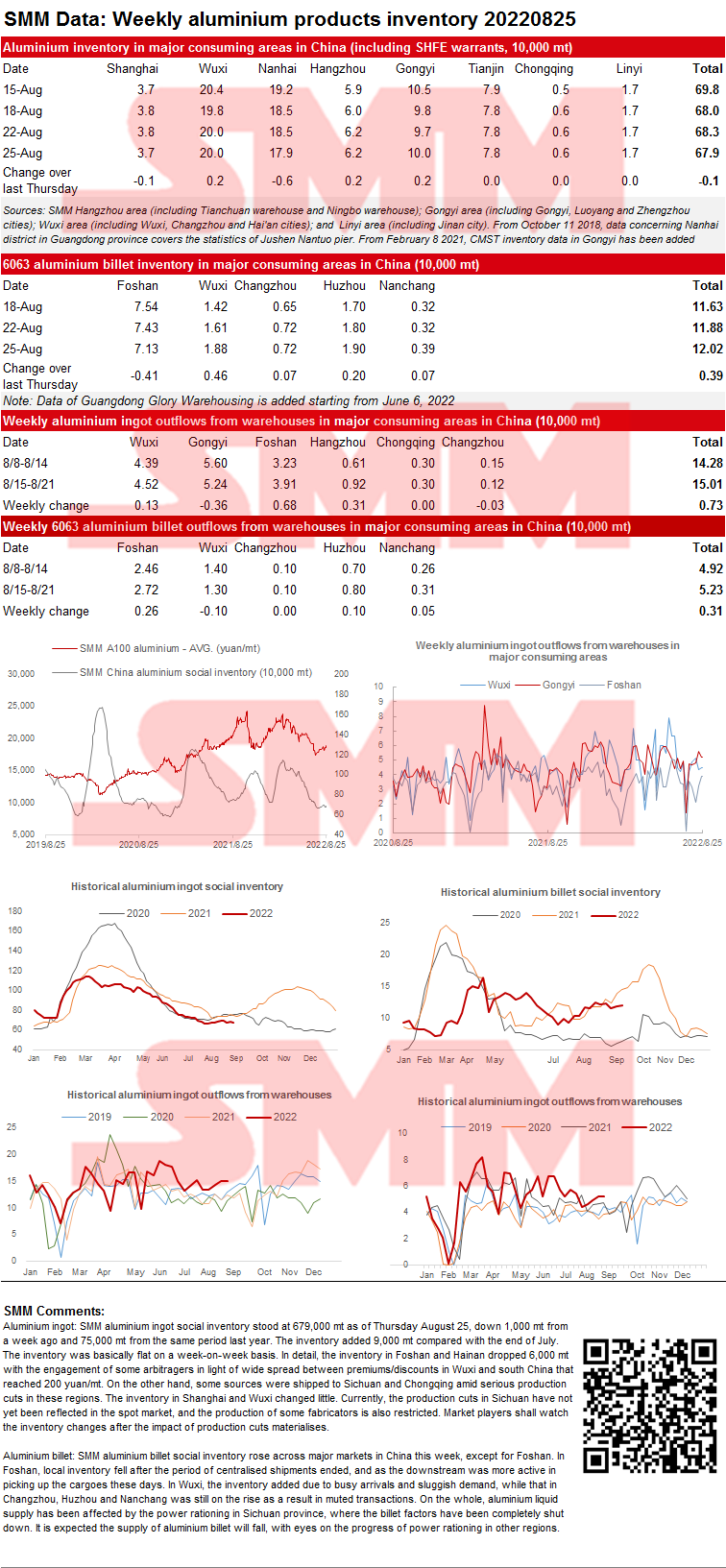

Aluminium Ingot Social Inventory Dropped while Billet Inventory Rose

SMM aluminium ingot social inventory stood at 679,000 mt as of Thursday August 25, down 1,000 mt from a week ago and 75,000 mt from the same period last year. The inventory added 9,000 mt compared with the end of July. The inventory was basically flat on a week-on-week basis. In detail, the inventory in Foshan and Hainan dropped 6,000 mt with the engagement of some arbitragers in light of wide spread between premiums/discounts in Wuxi and south China that reached 200 yuan/mt. On the other hand, some sources were shipped to Sichuan and Chongqing amid serious production cuts in these regions. The inventory in Shanghai and Wuxi changed little. Currently, the production cuts in Sichuan have not yet been reflected in the spot market, and the production of some fabricators is also restricted. Market players shall watch the inventory changes after the impact of production cuts materialises.

SMM aluminium billet social inventory rose across major markets in China this week, except for Foshan. In Foshan, local inventory fell after the period of centralised shipments ended, and as the downstream was more active in picking up the cargoes these days. In Wuxi, the inventory added due to busy arrivals and sluggish demand, while that in Changzhou, Huzhou and Nanchang was still on the rise as a result in muted transactions. On the whole, aluminium liquid supply has been affected by the power rationing in Sichuan province, where the billet factors have been completely shut down. It is expected the supply of aluminium billet will fall, with eyes on the progress of power rationing in other regions.

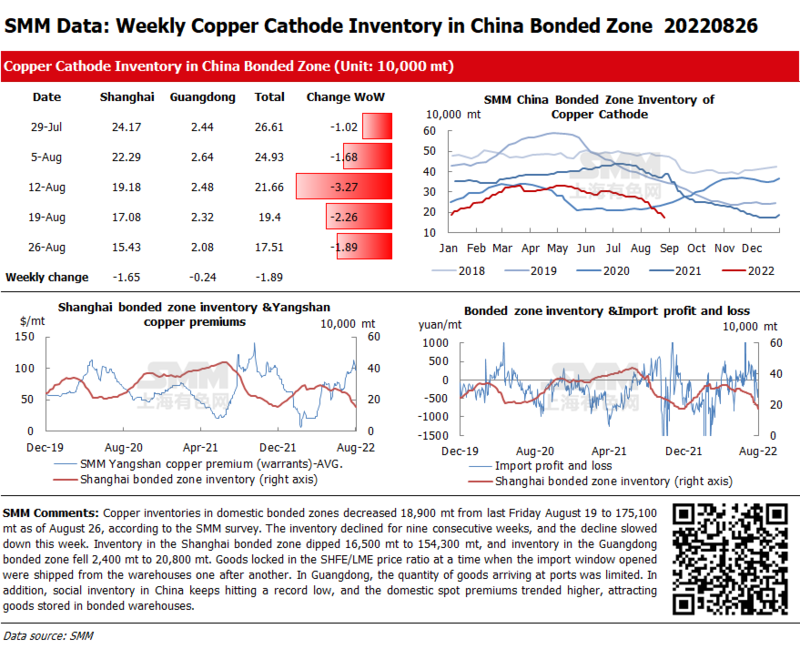

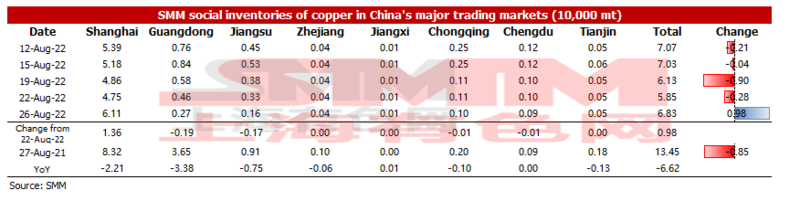

Copper Inventories in Domestic Bonded Zones Dipped 18,900 mt from Last Friday

Copper inventories in domestic bonded zones decreased 18,900 mt from last Friday August 19 to 175,100 mt as of August 26, according to the SMM survey. The inventory declined for nine consecutive weeks, and the decline slowed down this week. Inventory in the Shanghai bonded zone dipped 16,500 mt to 154,300 mt, and inventory in the Guangdong bonded zone fell 2,400 mt to 20,800 mt. Goods locked in the SHFE/LME price ratio at a time when the import window opened were shipped from the warehouses one after another. In Guangdong, the quantity of goods arriving at ports was limited. In addition, social inventory in China keeps hitting a record low, and the domestic spot premiums trended higher, attracting goods stored in bonded warehouses.

Copper Inventory across Major Chinese Markets Added 9,800 mt from Monday

As of Friday August 26, SMM copper inventory across major Chinese markets stood at 68,300 mt, up 9,800 mt from Monday and 7,000 mt from last Friday. Compared with Monday's data, copper inventory in most regions across China decreased except that in Shanghai. The total inventory fell 66,200 mt compared with the same period last year when the inventory was recorded at 134,500 mt. Among them, the inventory in Guangdong dropped 33,800 mt, and that in Shanghai dipped 22,100 mt.

In detail, the inventory in Shanghai added 13,600 mt to 61,100 mt because the arrival of imported copper increased. The inventory in Guangdong decreased 1,900 mt to 2,700 mt, which keeps hitting new lows. On one hand, the arrival of imported copper was low. On the other hand, domestic copper output was unstable, which may not improve in the short term.

Looking forward, as the power rationing in various regions is eased, the domestic copper output will gradually increase. However, consumption is likely to weaken next week against the high premiums and copper prices as well as the month-end factor. SMM believes that the weekly inventory next week may continue to rise.

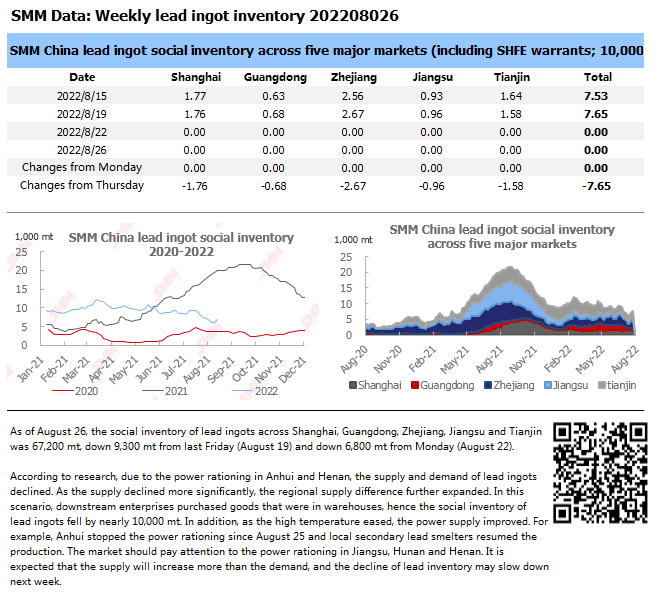

Social Inventory of Lead Ingot Fell by Nearly 10,000 mt amid the Power Rationing

As of August 26, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 67,200 mt, down 9,300 mt from last Friday (August 19) and down 6,800 mt from Monday (August 22).

According to research, due to the power rationing in Anhui and Henan, the supply and demand of lead ingots declined. As the supply declined more significantly, the regional supply difference further expanded. In this scenario, downstream enterprises purchased goods that were in warehouses, hence the social inventory of lead ingots fell by nearly 10,000 mt. In addition, as the high temperature eased, the power supply improved. For example, Anhui stopped the power rationing since August 25 and local secondary lead smelters resumed the production. The market should pay attention to the power rationing in Jiangsu, Hunan and Henan. It is expected that the supply will increase more than the demand, and the decline of lead inventory may slow down next week.

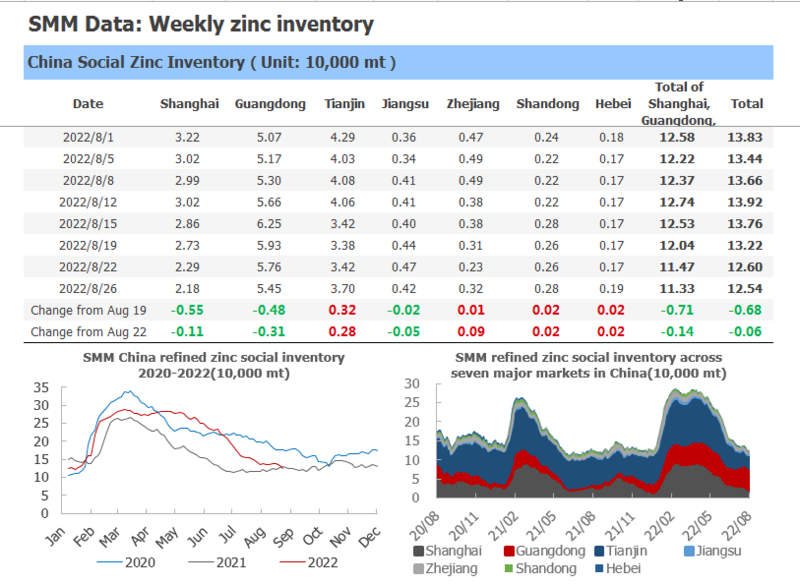

Zinc ingot social inventory across seven major markets in China decreased 600 mt from Monday

According to SMM data, the zinc ingot inventories across seven major markets in China totalled 125,400 mt as of August 26, down 600 mt from Monday and 6,800 mt from the previous week. Since the price difference of premiums between Shanghai and Tianjin expanded at the beginning of the week, some goods holders shipped their cargoes from Shanghai to Tianjin, leading to a decline in the Shanghai inventory. In Guangdong, the arrivals were relatively tight, and some goods holders also transfer zinc ingots to Tianjin for its high premiums. In addition, some smelters also delivered their goods to Tianjin, which accelerated the destocking of Guangdong inventory. In addition, after the zinc prices rallied, downstream traders purchased on rigid demand for the fears of further rise in the future. Therefore, the inventory in Guangdong dropped on the week. In Tianjin, the arrivals of goods from smelters in north China remained low. But, thanks to the high premiums in Tianjin, some stocks in Guangdong and Shanghai were transferred to there, contributing to a slight growth in Tianjin inventory as the market purchase on rigid demand was limited. It is expected that the Tianjin inventory will trend higher next week. Overall, the total inventory in Shanghai, Guangdong and Tianjin fell 1,400 mt, and that across seven major regions in China declined 600 mt from Monday.

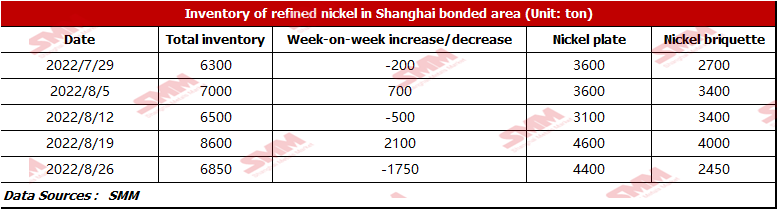

Bonded Zone Inventory of Nickel Dropped 1,750 mt from Last Friday

According to the SMM research, the bonded zone inventory stood at 6,850 mt this week. The inventory of nickel briquette was 2,450 mt, and that of nickel plate was 4,400 mt, down 200 mt WoW. The slight decrease in nickel plate inventory was caused by the small import profits and the poor downstream demand. The inventory of nickel briquette dropped 1,550 mt, because the nickel sulphate capacity is gradually released in the peak season of new energy industry, which demands more nickel briquette in the short term.

Social Inventory of Silicon Metal Decreased on the Week

According to SMM, the social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port decreased 1,000 mt from the previous week to 109,000 mt as of August 26. The inflow and outflow of Tianjin port changed little on the week, while the inventory of Huangpu port declined as the arrivals were less and the shipments increased. The inventory of Kunming city increased slightly due to the poor transactions. The increase of inventory in Sichuan and other regions slowed down due to the seasonal decline in the output.

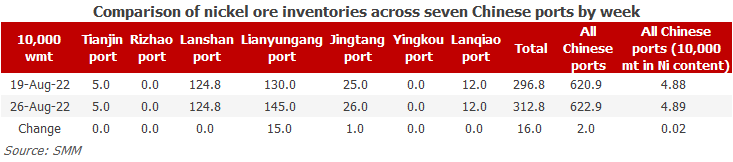

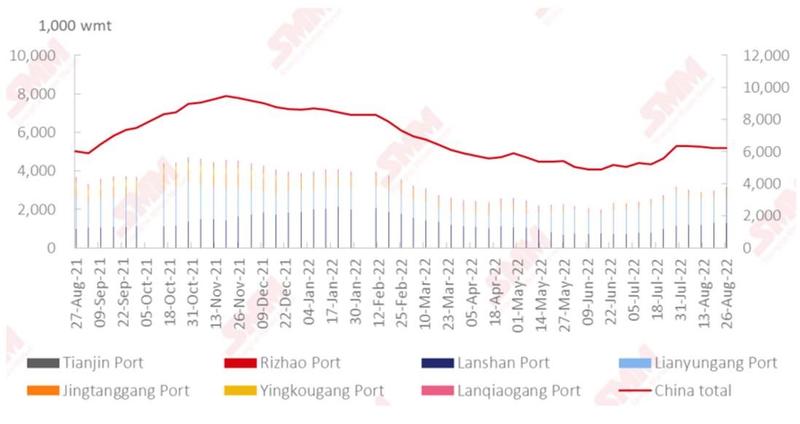

Nickel Ore Inventories at Chinese Ports up 20,000 wmt WoW

As of August 26, port inventories of nickel ore in China added 20,000 wmt to 6.23 million wmt compared with last week. The total Ni content stood at 48,900 mt. Port inventory of nickel ore across seven major Chinese ports stood at 3.13 million wmt, 160,000 wmt higher than last week. The current demand for nickel ore from NPI plants and steel mills was poor, and consumption of nickel ore was slow in the case of low output. Although shipments from mines stood stable, the performance was still poor compared with the same period last year, hence the arrivals were lower than expected. Short-term ore inventory will hover around the current level. NPI plants are less willing to restock amid the bearish market outlook, so the port inventory cannot increase significantly.