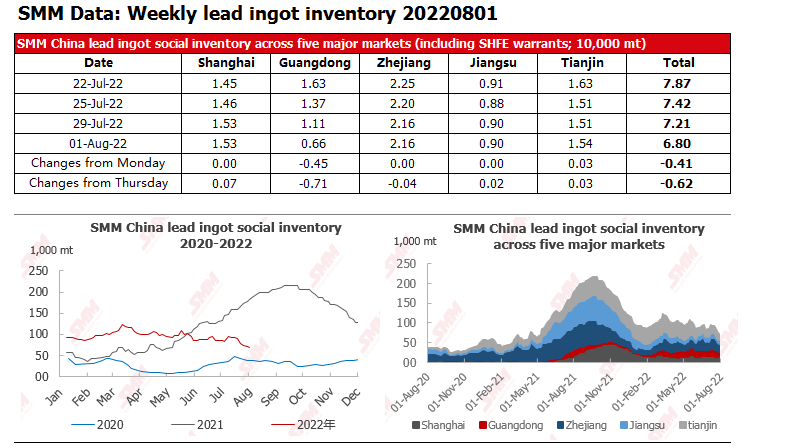

SHANGHAI, Aug 1 (SMM) - As of August 1, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 68,000 mt, down 4,100 mt from last Friday (July 29) and down 6,200 mt from last Monday (July 25).

According to research, the lead ingot inventory in Guangdong fell most sharply. Due to the active trading activity in the spot market, the operating rates of downstream increased and the the demand for lead ingots increased. However, the inventory in Guangdong fell significantly because the stocks may be transferred due to the follow-up impact of the warrants pledge scandal of aluminium. In addition, due to the eased impact of maintenance and power rationing, the supply of lead ingots gradually recovered. At the same time, the consumption of lead-acid batteries improved and downstream enterprises purchased as needed. In addition, as the smelters shipped in huge discounts, downstream enterprises tended to purchase from smelters. Therefore, the market transactions decreased. In this scenario, the inventories in most place decline more slowly, some even increased slowly. However, due to the huge decline of inventory in Guangdong, the overall social inventory of lead ingots fell.

![Secondary Lead Raw Material Recycling Diverged, Secondary Crude Lead Supply Tightened and Prices Are Expected to Remain Firm in the Future [SMM Scrap Battery & Secondary Crude Lead Weekly Review]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![Downstream Enterprises Bought the Dip, and Primary Lead Enterprise Plant Inventory Continued to Decline [SMM Weekly Review of Primary Lead Inventory]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)

![SHFE Lead Closed Slightly Higher Intraday, Lead Prices Remained Volatile Amid the Tug-of-War Between Sellers and Buyers [Brief Commentary on Lead Futures]](https://imgqn.smm.cn/usercenter/xVgcv20251217171721.jpg)