SHANGHAI, Mar 9 (SMM) - At the beginning of 2022, domestic aluminium maintained high profitability, and aluminium managed an exciting start in 2022. According to the SMM aluminium cost model (measured by real-time raw material prices), the weighted average full cost of China's aluminium industry in February was about 18,255 yuan/mt, a year-on-year increase of 34.5%. On the combination of SMM prices, SMM believes that the average instant profit of domestic aluminium in February was 4,468 yuan/mt, an increase of 80% year-on-year. All aluminium capacities were making profits in February.

Cost: The prices of raw and auxiliary materials as well as electricity all recorded large increases year-on-year

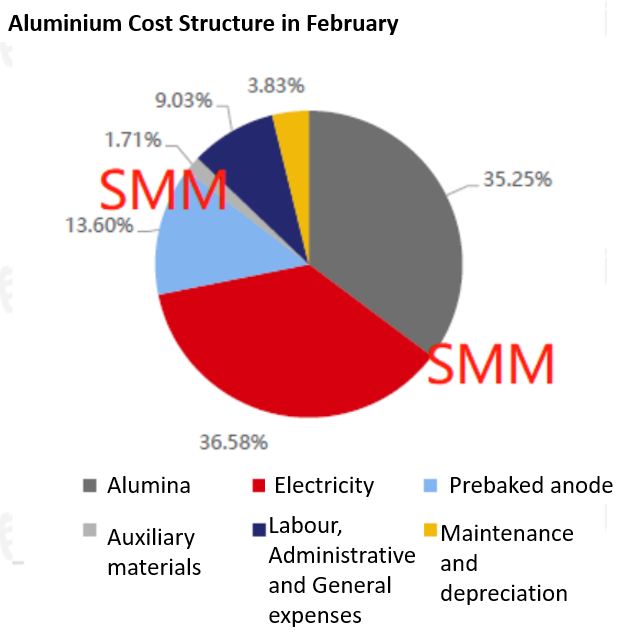

Electricity: In February, the electricity cost of domestic aluminium remained flat month-on-month and rose 46% year-on-year

Before the Spring Festival, the National Development and Reform Commission held a special meeting to guarantee coal supply and price stabilisation during the Spring Festival. Domestic coal enterprises maintained stable production in the holiday season, and were required to lift the inventory level at ports. Thermal coal prices were weak under the expectation of price regulation and guaranteed supply. After the Spring Festival, domestic port inventories were low, and thermal coal prices rebounded. On February 9, the National Development and Reform Commission convened a meeting on ensuring supply and stabilising prices again, requiring the prices at port shall be lower than 900 yuan/mt, and those at pithead shall below 700 yuan/mt. On February 24, the National Development and Reform Commission convened a price control meeting again, requiring that medium and long-term transaction prices of 5,500 kcal thermal coal at Qinhuangdao Port shall move between 570-770 yuan/mt (tax included).

As a whole, the domestic thermal coal market in February mainly fluctuated within a narrow range. The electricity cost of domestic self-provided power plants was relatively stable. According to the real-time thermal coal price of the month, the cost of self-provided power plants in East China was about 0.4-0.5 yuan/KWH. The company settles according to the local grid price. Among them, the grid electricity price in Guangxi, Guizhou and other places is 0.57-0.67 yuan/KWH as a whole, which is still at a relatively high level. According to the real-time thermal coal prices of the current month, the cost of captive power plants in east China was about 0.4-0.5 yuan/kWh in February. Some enterprises settled the costs according to the local grid power prices. Among them, the grid power prices in Guangxi and Guizhou were 0.57-0.67 yuan/kWh, which was still at a relatively high level. According to SMM survey, the weighted average electricity price of domestic aluminium enterprises in February was about 0.49 yuan/kWh, a year-on-year increase of 46%, and flat month-on-month. The electricity cost per tonne of aluminium accounted for about 36.58% of the total cost, ranking first among others.

Alumina: In February, the prices of alumina rose before falling

In February, domestic operating alumina capacities dropped mainly because the refineries in Shanxi, Shandong and Henan were inconsistent in production due to the Winter Olympics, and the local refineries cut the production for nearly half a month. In addition, the outbreak of the pandemic in Guangxi affected some alumina production and transportation. In early February, domestic alumina prices rose rapidly. With more refineries that cut the production before resuming the operation, the support from the fundamentals weakened, and the prices of alumina corrected rapidly later in the month. According to SMM data, the cost of alumina for domestic aluminium in February was about 3,319 yuan/my, a month-on-month increase of 10.5% and a year-on-year increase of 36%, accounting for 35.25% of the total cost.

Auxiliary materials: Prebaked anode prices rose further on strong cost support

In February, the domestic prebaked anodes ushered in a rebound in the market. The benchmark price of large aluminium plants in Shandong was raised by 350 yuan/mt from the previous month, and the benchmark price was set at 5,005 yuan/mt. The prebaked anode industry chain is relatively simple, with aluminium being the only downstream sector, hence the pricing power is mostly in the hands of aluminium smelters. Aluminium smelters will mostly decide the purchase prices of prebaked anode of the next round based on the prices of petroleum coke and coal tar pitch in the previous round. The price changes of anodes in various regions are roughly the same. Considering the difference in raw material transportation distance, the prebaked anodes used in aluminium smelters in north-west and south-west China are generally higher than those in east China. According to SMM, the national weighted average price of domestic prebaked anodes in February was about 5,521 yuan/mt, a year-on-year increase of 45% and a month-on-month increase of 7%.

Short-term outlook: In March, the cost of domestic aluminium is still expected to rise. The full cost of domestic aluminium is expected at 18,100-18,700 yuan/mt in March. SMM believes that the domestic aluminium industry will still maintain a high profitability in March, and the industry's average profit will be around 4,300 yuan/mt.

And the reasons are as follows:

Thermal coal: China government will continue to stabilise the prices and supply in the coal market. However, the continued surge in overseas energy prices may affect the imports of thermal coal. The potential falling imports will not only exacerbate the shortage of coal for captive power plants but also raise the prices.

Alumina: The tensions between Russia and Ukraine escalated, and Rusal closed its Nikolaev alumina plant in Ukraine, involving a production capacity of 1.77 million mt. The supply of overseas alumina has tended to be in short supply from a tight balance, boosting the prices of overseas alumina by 22% in the month. However, if the conflict or the sanctions on Rusal escalate, the price gap between overseas and Chinese alumina will continue to expand, and China may change from a major alumina importer to an exporter, and boost the domestic alumina market.

Auxiliary materials: Prebaked anode prices are expected to rebound sharply in March under the strong support of petroleum coke prices.

Spot: In March, the aluminium prices are expected to be rise supported by overseas supply shortage and strong domestic fundamentals, and the most-traded SHFE aluminium contract will move between 22,500-24,500 yuan/mt.

Risks: At present, the high profitability of the aluminium industry is largely due to the high aluminium prices. The cost has been at a historically high level compared with the previous years. In the case of high cost and high profit, aluminium enterprises also need to be vigilant about aluminium prices that may pull back rapidly in the future.

![Uncertainty Still Surrounds the Geopolitical Situation in the Middle East, and Aluminum Prices Still Have Short-Term Upward Momentum [SMM Aluminum Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/bHIPd20251217171651.jpg)

![SHFE Aluminum Saw Wide Swings for Multiple Days, While Alloy Followed the Uptrend Strongly [SMM Cast Aluminum Alloy Morning Comment]](https://imgqn.smm.cn/usercenter/ifCaw20251217171652.jpg)