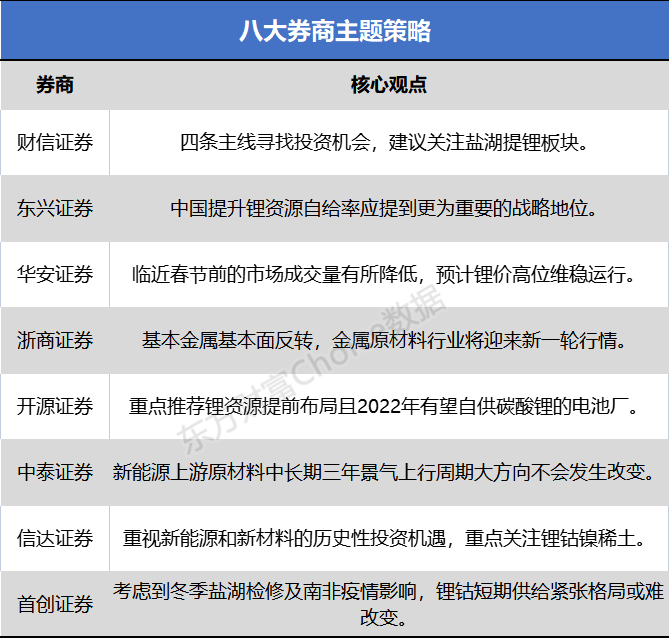

Daily theme strategy discussion, Oriental Fortune Network summarizes the views of eight brokerages, reveals the current situation of the industry, observes the market trend, and feels the pulse A shares for you in advance.

Caixin Securities: four main lines looking for investment opportunities suggest paying attention to the salt lake lithium extraction plate

It is suggested to look for investment opportunities from the following four main lines: 1. Biodegradable materials plate. Degradable material is a hot spot of policy in our country. At present, PLA and PBAT materials are the most mature and may be popularized on a large scale. It is suggested that we should pay attention to Jindan technology and Cofco technology with PLA lactide core technology, Hengli petrochemical with PBAT integrated industrial chain, and Tongcheng new material with BASF PBAT core patent.

2. Semiconductor material plate. The localization of semiconductor materials is a general trend. It is recommended to pay attention to the upstream semiconductor material subdivision plate high-quality companies, including Nanjing University Optoelectronics, Jacques Technology, Walter Gas, Jinhong Gas and so on. Jiang Huawei, a leading company in wet electronic chemicals, etc.

3. New energy lithium plate. With the recovery of the proportion of lithium iron phosphate, the demand for phosphoric acid of upstream raw materials will rise rapidly. It is suggested to pay attention to the targets of phosphorus chemical related enterprises, such as Xingfa Group, Yuntu Holdings, Xin Yangfeng, Yuntianhua and so on.

4. Extracting lithium plate from salt lake. It is expected that the mainstream technologies of lithium extraction from salt lakes in China in the future are adsorption, membrane and extraction. From the current point of view, the adsorption extraction of lithium by Lanxiao technology has been used in Zangge and Jintai, and the effect is good. Lanxiao technology is recommended. At the same time, it is suggested that we should pay attention to Jiuwo Hi-Tech and Sanda membrane marked by membrane method, and extract Xinhua shares marked by membrane method.

Dongxing Securities: China's raising the self-sufficiency rate of Lithium Resources should be raised to a more important Strategic position

The spot auction mode of concentrate has an impact on the current long order pricing mechanism, and the trend of integration of lithium industry chain is becoming more and more obvious. In 2021, Australian lithium concentrate spot successfully achieved sales through the bidding auction mode, the anchoring effect of the bidding price has been fully demonstrated, and the mine bargaining power has been significantly improved. The successful implementation of the auction model and the high premium space relative to the long order may lead to the follow-up of new mines, leading to the decline of the proportion of the long Association or the adjustment of the pricing formula, which may have a far-reaching impact on the future pricing mechanism of the industry. The profit space of lithium salt processing in China is facing further compression, and it is more difficult to obtain the right of underwriting at low cost.

From the perspective of the industrial chain, whether it is the extension of processing / battery enterprises to the resource end, the self-built processing capacity of mines or the cooperation with downstream enterprises to build factories, all parties in the industry are trying to build their own business integration and coordination, in order to achieve the purpose of grabbing excess profits and increasing pricing power.

European and American countries have obvious resource advantages and broad terminal automobile market, and make efforts to increase processing capacity and try to build their own supply chain closed loops. The previous cooperation mode of "Australian Mine + Chinese processing Plant" may face challenges. Considering geopolitics, industrial upgrading and other factors, China's promotion of lithium resource self-sufficiency rate should be mentioned to a more important strategic position; for the domestic lithium industry, enterprises with good resource endowment, high guarantee rate and strong certainty of performance release will get a higher valuation premium. Related companies: Ganfeng Lithium Industry, Tianqi Lithium Industry, Salt Lake shares.

Huaan Securities: the market trading volume has decreased near the Spring Festival. It is expected that the high lithium price will maintain a stable operation.

Lithium salt manufacturers have entered the maintenance period, supply is tight catalytic price is expected to rise. At present, the stock in advance of the Trade Festival is basically completed, and the market trading volume near the Spring Festival has decreased, and the high lithium price is expected to maintain a stable operation. It is suggested to focus on: Huayou Cobalt Industry and Hanrui Cobalt Industry, which are the targets of the integrated layout of cobalt industry; Ganfeng Lithium Industry, Tianqi Lithium Industry, the leading enterprises with high self-sufficiency rate of lithium resources; Salt Lake Lithium related targets: salt Lake shares, Tibet Everest, Tibet Mining, medium Mine Resources; Lithium Mica related targets: Yongxing Materials, Jiangdian Special Machinery; spodumene related targets: Sichuan Energy Power.

Zeshang Securities: basic metal fundamentals reverse metal raw material industry will usher in a new round of market

With the Beijing Winter Olympic Games approaching, the production of alumina enterprises in some Shandong areas is limited, environmental control is expected to stimulate alumina prices to a certain extent, while some downstream processing enterprises are gradually entering the Spring Festival holiday, demand is sluggish, inventory is expected to continue to rise. At present, relevant policies are being deployed around stable growth, and the issuance of special bonds is speeding up. At a regular briefing on the policy of the State Council on the management of special bonds, Xu Hongcai said, "in view of the great pressure on steady growth in the first quarter of next year, the Ministry of Finance has recently issued some new special bond quotas ahead of schedule, requiring all localities to issue and use them early in the first quarter of next year. The issuance of special bonds next year should grasp three words: early, accurate and fast. The steady growth measures of local governments are expected to accelerate the landing, the fundamentals of basic metals are reversed, and the metal raw materials industry will usher in a new round of market.

Open source securities: battery plants that focus on the advance layout of lithium resources and are expected to self-supply lithium carbonate in 2022

Due to the contradiction between supply and demand, the price of lithium has continued to rise since July 2021. Up to now, the price of battery-grade lithium carbonate is 34-350000 yuan / ton, the price of industrial-grade lithium carbonate is 32-330000 yuan / ton, part of the competitive selling price is 35-365000 yuan / ton, and the quoted price of lithium hydroxide is about 26-300000 yuan / ton. The recent rising price of lithium carbonate is affected by the limited supply of natural gas in the western region on the one hand and the extraction of lithium from salt lakes by the low temperature in winter on the other hand. It is expected that the contradiction between supply and demand in 2022 will be concentrated in Q1, and the contradiction between supply and demand at the end of Q1 in 2022 is expected to be alleviated. Lithium prices are expected to remain high throughout the year in 2022.

Supply side: in 2022, we should focus on the completion of salt lake and mineral projects. It is expected that 2022Q4 production capacity will be gradually released, with an annual lithium supply of 76-800000 tons. The supply side is restricted by the long release cycle of the new capacity of lithium salt (2-3 years) and the world's most important high-quality resources have been carved up in the last round. Most of the lithium resources recently purchased by lithium companies or battery factories are primary mines, and there is some uncertainty about the input and output.

Demand side: but the penetration of new energy vehicles will increase rapidly in the next few years, and the demand is likely to exceed expectations. We expect global lithium battery shipments to reach 1300-1500GWH in 2024, measured in terms of lithium carbonate consumption per GWh. Lithium carbonate demand is expected to exceed 1 million tons in 2024 and 1.5 million tons in 2025 (lithium battery 1700-2000GWh shipments).

Battery factories with advanced layout of lithium resources and expected self-supply of lithium carbonate in 2022 are recommended: Ningde Times, BYD, Yiwei Lithium Energy, Guoxuan Hi-Tech and so on. In addition, after the high price of Q1 lithium carbonate in 2022, it is good for core growth and post-cycle targets: Enjie shares, Pu Tailai, German Nano, Rongbai Technology, Dangsheng Technology, Jinbei Electric and so on.

Zhongtai Securities: the medium-and long-term upstream raw materials of new energy will not change the general direction of the three-year upstream cycle.

For basic metals, China's economic work in 2022 will set the tone of "steady word first", which will support the prices of basic metals to a certain extent, but from the global dimension, 1) the structural changes before, during and after the outbreak of overseas economic demand, and 2) the taper trend of global liquidity remains unchanged, and the downward trend of basic metals may not have been fundamentally changed.

For the upstream raw materials of new energy, such as lithium, cobalt, rare earth, copper foil, aluminum foil, etc., the short-cycle demeanor is still strong, and the general direction of the medium-and long-term three-year upstream cycle will not change, and the industrial boom is the most clear and firm.

From the point of view of the core target: 1) new energy automobile industry chain: Ganfeng lithium industry, Tianqi lithium industry, China Mineral Resources, Yongxing Materials, Yahua Group, Huayou Cobalt Industry, Luoyang Molybdenum Industry, Northern rare Earth, Shenghe Resources, Zhenghai Magnetic Materials, Jinli permanent Magnet, Dadixiong, Dingsheng New Materials, Norde shares, Jiayuan Technology and so on. 2) basic metals: Yunnan Aluminum Co., Ltd., Shenhuo Co., Ltd., Tianshan Aluminum Industry, Suotong Development, Zijin Mining, Tongling Nonferrous, etc. 3) Precious metals: Shandong gold, Shengda resources, etc.

Cinda Securities: attach importance to the historic investment opportunities of new energy and new materials, focusing on lithium, cobalt, nickel and rare earths

In the context of the "double carbon" goal, we attach importance to the historic investment opportunities of new energy and new materials, focusing on new energy metals (lithium, cobalt, nickel, rare earths) with strong demand and weak supply pattern, and new metal materials that benefit from industrial upgrading and domestic substitution. Lithium suggests paying attention to Tianqi Lithium Industry, Ganfeng Lithium Industry, Yongxing material, Shengxin Lithium Energy, etc.; New Materials suggest paying attention to Homei New Materials, Power Diamond, Hesheng shares, Quartz shares, Bowei Alloy, Chujiang New Materials, etc. Titanium suggests paying attention to Bao Ti shares, Anning shares, etc.; Precious Metals suggest paying attention to Chifeng Gold, Yintai Gold, Precious Research Platinum Industry, etc. Industrial metals suggest to pay attention to cloud aluminum shares, Shenhuo shares, Western Mining, Zijin Mining, Lizhong Group, Suotong development and so on.

Pioneering Securities: considering the impact of winter salt lake maintenance and the epidemic situation in South Africa, it may be difficult to change the short-term supply tension of lithium and cobalt.

Recently, the Ministry of Industry and Information Technology and other departments issued the "14th five-year Plan for the Development of Raw Materials Industry", proposing that by 2025, the production capacity of bulk products of key raw materials such as crude steel and cement will only decrease, and the utilization rate of capacity will remain at a reasonable level. at the same time, it is proposed that the carbon emission of electrolytic aluminum will be reduced by 5%. We believe that the proposal of the document once again strictly restricts the future total production capacity of some commodities, while the reduction target of electrolytic aluminum carbon emissions is good for the recycled aluminum industry, and it is recommended to pay attention to Yiqiu Resources, Mingtai Aluminum and Aluminum of China.

In addition, considering the influence of the overhaul of salt lakes in winter and the epidemic situation in South Africa, it may be difficult to change the short-term supply of lithium and cobalt, so it is recommended to pay attention to Tianqi lithium industry, Ganfeng lithium industry and Huayou cobalt industry.

![March Battery Materials Import and Export Data Released, Spodumene Imports Hit New High, Lithium Carbonate Continued YoY Growth [SMM Special Report]](https://imgqn.smm.cn/usercenter/Jgxij20251217171726.jpg)