SHANGHAI, Jan 21 (SMM) - This is a roundup of China's metals weekly inventory as of January 21.

Aluminium Social Inventories Up 2,000 mt on Week

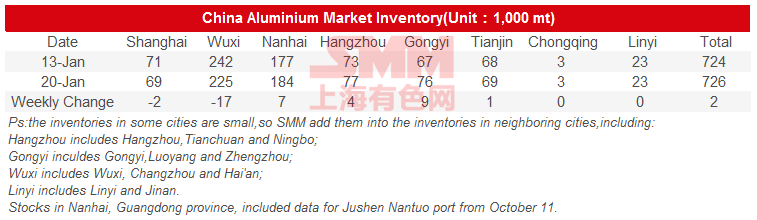

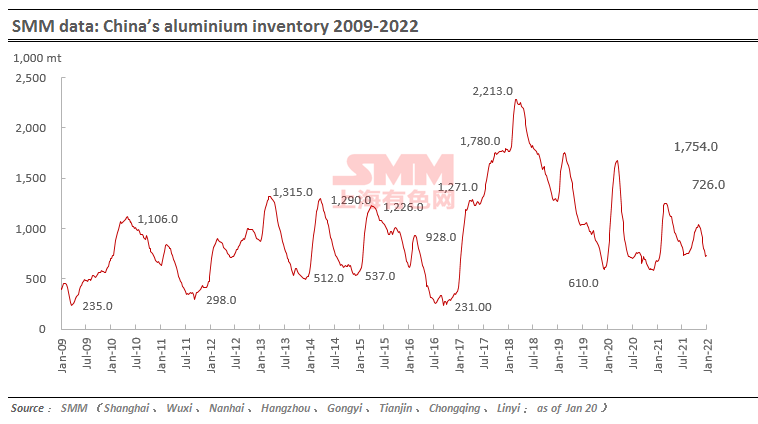

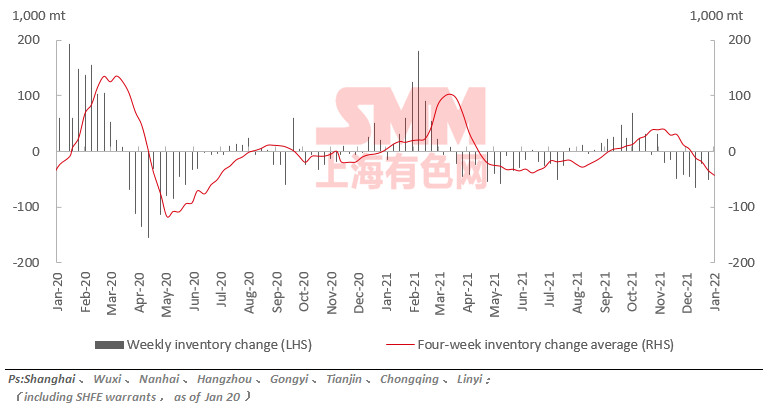

SMM data showed that China's social inventories of aluminium across eight consumption areas rose 2,000 mt on the week to 726,000 mt as of January 20, mainly contributed by Nanhai, Hangzhou and Gongyi.

The inventory rose by 4,000 from Monday January 17. And the inventory in Shanghai and Wuxi dropped mainly because the arrivals were low and the shipments were moderate.

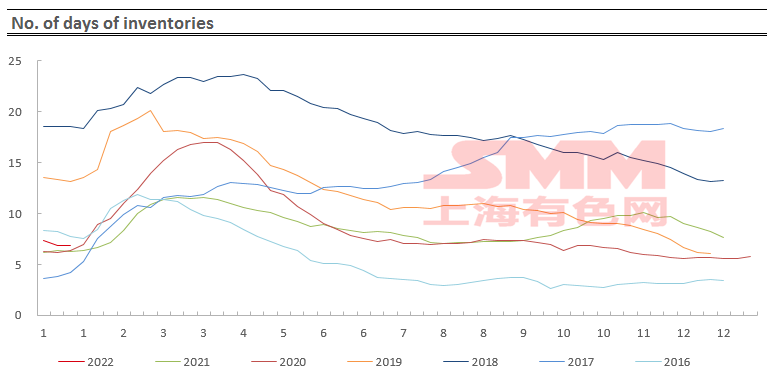

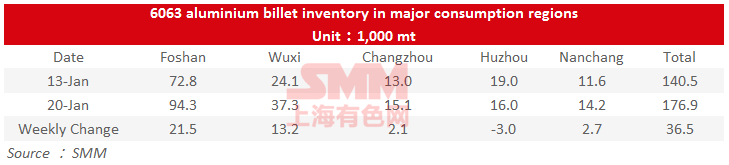

Aluminium Billet Inventories Up 36,500 mt on Week

The stocks of aluminium billet in five major consumption areas added 36,500 mt to 176,900 mt on January 20 from a week ago, a significant increase of 25.95%. The inventory has been rising for four straight weeks.

All the other four market recorded gains in inventory except Huazhou. The inventory in Foshan and Wuxi contributed most of the increase, which rose by 21,500 mt and 13,200 mt respectively, up 29.53% and 54.77% on a weekly basis. The downstream orders weakened further this week, resulting in sluggish demand for aluminium billet.

Looking into next week, it expected that the downstream consumption will remain week, hence the weekly aluminium billet inventory will keep rising.

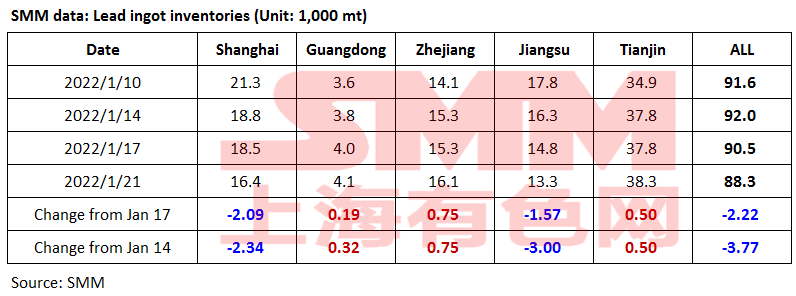

Lead Ingot Social Inventory Fell 3,800 mt on Week

The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 3,800 mt from January 14 and 2,200 mt from January 17 to 88,300 mt as of January 21.

Considering that the logistics will be stopped during the Chinese New Year holiday, the downstream enterprises were stocking up the raw materials. However, the transportation of lead ingots was interrupted by the COVID-19 pandemic and early CNY holidays in some regions, so the users tended to purchase from nearby regions. As such, the inventories continued to fall in Jiangsu and Shanghai, and the total social inventory declined.

Most of the downstream battery producers will start to take holidays next week, while the primary lead will basically maintain their production, which may result in the increase in the inventories. And the stocks are likely to rise more significantly at smelters due to the stopped logistics.

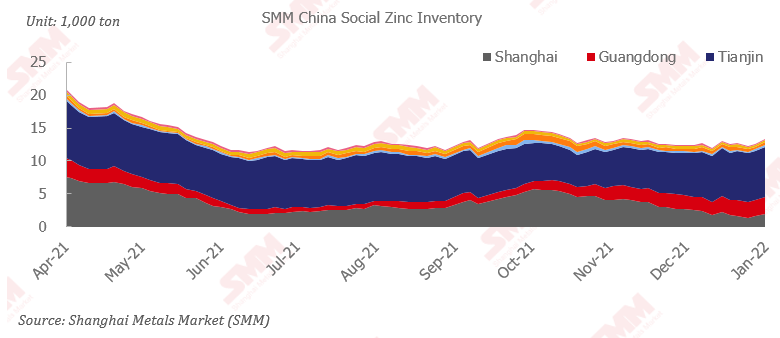

Zinc Ingot Social Inventory in Seven Major Regions Rose 10,500 mt

As of January 21, the zinc ingot inventory across the seven major regions in China totalled 133,600 mt, up 7,400 mt from January 17 and up 10,500 mt from January 14, according to SMM data. The increase in Shanghai was due to more arrivals and closures of downstream producers for the CNY. The inventory in Guangdong rose as downstream demand declined, even as fewer goods arrived. The inventory in Tianjin continued to increase amid modest arrivals and falling demand. The total inventories across Shanghai, Guangdong, and Tianjin rose by 9,600 mt from January 14.

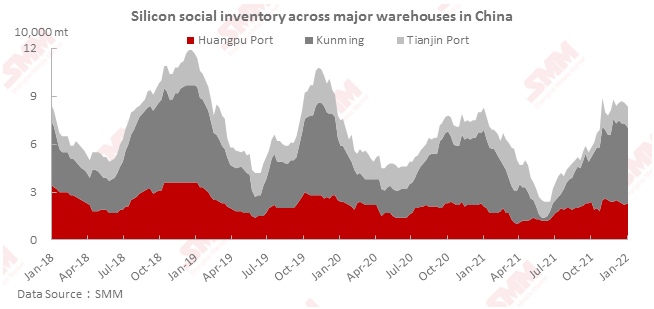

Silicon Metal Social Inventory Declined 2,000 mt on Week

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port decreased 2,000 mt from the previous week to 82,000 mt as of Friday January 21. The domestic transactions shrank sharply this week. The inventory in Kunming declined due to the low arrivals. The shipments from Huangpu port were relatively high, while that from the Tianjin port were few. The port operations are expected to be halted by next Tuesday. The social inventory of silicon metal is expected to drop slightly next week.

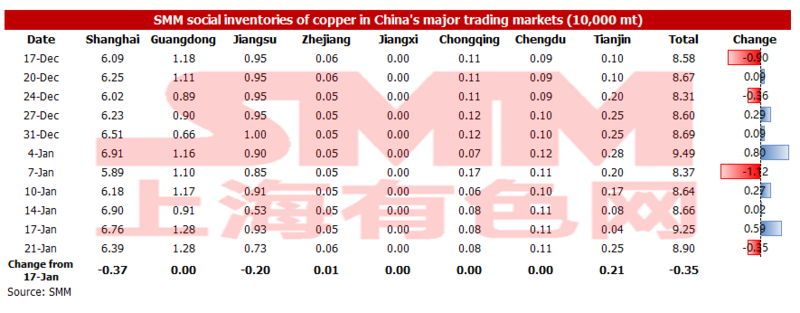

Copper Inventory in Major Chinese Markets Dipped 3,500 mt on Week

As of Friday, January 21, the copper inventories in major domestic markets decreased 3,500 mt from Monday to 89,000 mt, but added 2,400 mt from a week earlier to 86,600 mt, growing for the second straight week. Compared with Monday, only the inventory in Tianjin increased significantly, while the inventory fell across Shanghai and Jiangsu. The inventory in other areas changed little.

Specifically, the inventory in Shanghai decreased by 3,700 mt to 63,900 mt, the inventory in Jiangsu dipped 2,000 mt to 7,300 mt, and the inventory in Tianjin grew 2,100 mt to 2,500 mt.

The increased shipments arrivals in Tianjin after the COVID situation improved drove the inventory growth. In east China, the limited customs clearance for imported copper, combined with the stockpiling by downstream producers ahead of CNY holidays, lowered the inventories in Shanghai and Jiangsu significantly.

As the CNY holidays near, more downstream buyers will be closed next week, and the consumption will further weaken. The inventory is expected to accumulate.

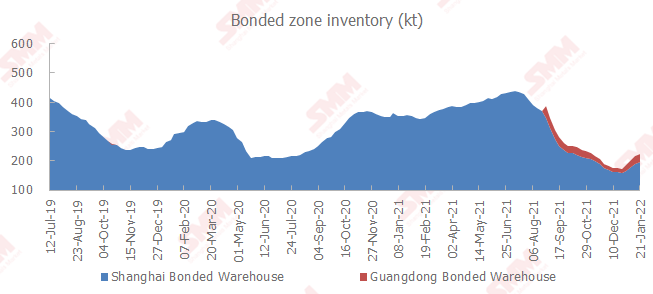

Copper Inventory in China Bonded Zone Grew 7,700 mt on Week

The copper inventories in the domestic bonded zones added 7,700 mt from January 14 to 224,500 mt as of Friday January 21, the second consecutive week of growth, according to the most recent SMM survey.

The inventory in the Shanghai bonded zone was up 9,000 mt to 197,000 mt, while the inventory in the Guangdong bonded zone fell 1,300 mt to 27,500 mt. The trading in the copper import market has weakened as the CNY holidays approach. The severe import losses also weakened the import demand. Therefore, some traders stocked their cargoes into the bonded warehouses. Meanwhile, domestic smelters exported some copper cathode into the bonded zone, growing the inventory in the Shanghai bonded zone. The inventories in the Guangdong bonded zone decreased slightly due to lower shipments arrivals.

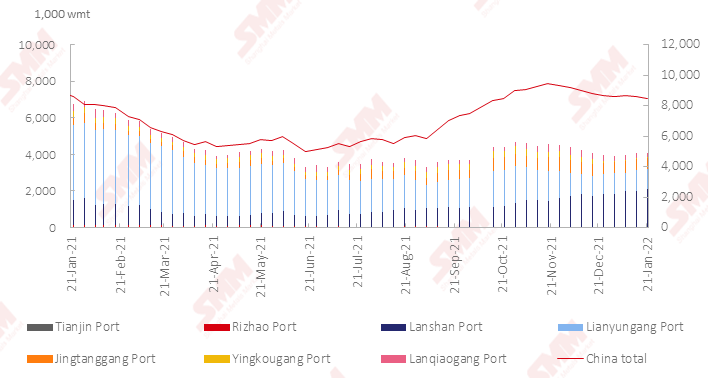

Nickel Ore Inventories at Chinese Ports Fell 142,000 wmt

The nickel ore inventory at Chinese ports dipped 142,000 wmt from a week earlier to 8.45 million wmt as of January 21. Total Ni content stood at 66,400 mt. The total inventory at seven major ports stood at around 4.1 million wmt, up 18,000 wmt from a week earlier.

Customs data showed that the imports of laterite nickel ore dropped sharply in December due to the significant impact from the wet season. The port inventory trended lower. However, the downstream purchasing interest has weakened recently as the nickel ore prices are expected to rise.

The port inventory will enter the downward track again.