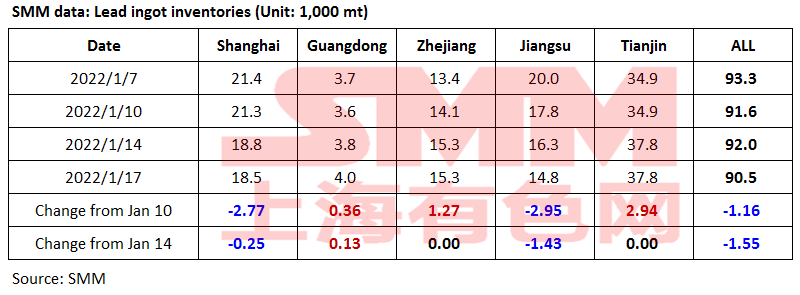

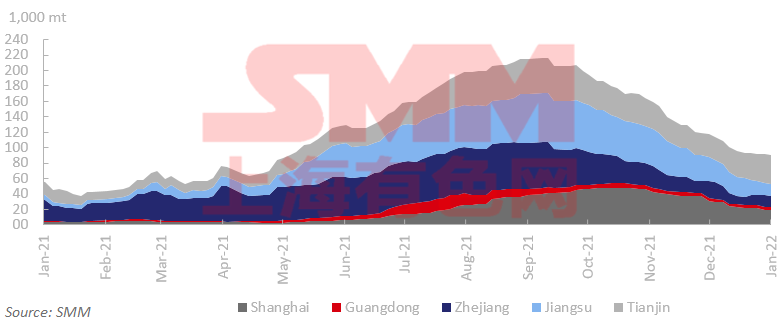

SHANGHAI, Jan 17 (SMM) – The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 1,600 mt from last Friday January 14 and fell 1,200 mt from last Monday January 10, as of January 17.

According to SMM research, the lead ingot supply varied greatly in different regions. There were both primary and secondary lead smelters resuming the production after maintenance, while the downstream was still restocking as a convention ahead of the Chinese New Year.

In details, the inventory in Guangdong, Tianjin and Zhejiang rose as the primary and secondary lead smelters in Guangdong and Anhui resumed the production; while the affected transportation due to the COVID pandemic in Tianjin resulted in slower shipments for delivery of orders. The Inventory in Shanghai and Jiangsu continued to drop partly because the smelters in Jiangsu were still under maintenance. Meanwhile, the downstream restocked for the CNY holiday, and some had to purchase from adjacent areas as the pandemic has led to higher freights.

![Weekly Review of Lead Futures Prices (2026.3.20-2026.4.3) [SMM Lead Weekly Review]](https://imgqn.smm.cn/usercenter/riosq20251217171722.jpg)

![Weekly Brief Review of the Lead Concentrates Market (March 30, 2026 - April 03, 2026) [SMM Lead Concentrates Weekly Review]](https://imgqn.smm.cn/usercenter/bAjSC20251217171721.jpg)

![The Off-Season in Consumption Is Expected to Arrive Soon, Trading in the Primary Lead Spot Market Was Muted and Premiums Declined [SMM Weekly Review of the Refined Lead Spot Market]](https://imgqn.smm.cn/usercenter/LCtEk20251217171721.jpeg)