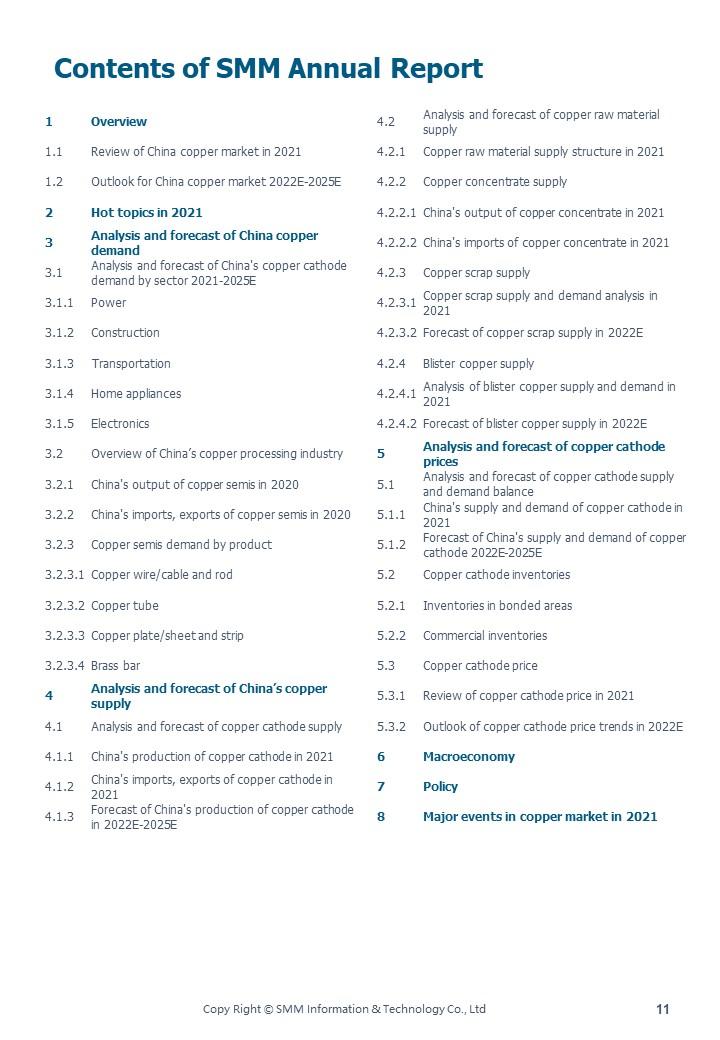

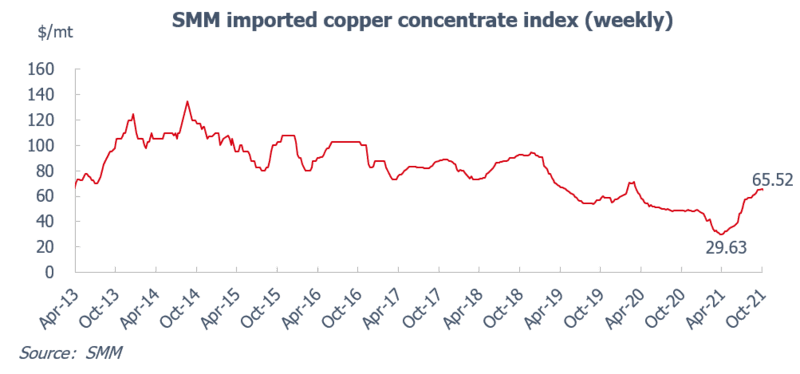

SHANGHAI, Nov 15 (SMM) - Although there were hardly any disruptions to the production at overseas mines from the COVID-19 pandemic at the beginning of 2021, many unexpected shipping issues in South America have caused sudden changes in the copper concentrate spot market. Las Bambas mine underwent community roadblocks in mid-December, 2020, and the impact on the mine exceeded market expectations. The ports in Chile faced high tides in January, which were concentrated in the northern region, the main copper concentrate production area in the country. That affected the delivery of large copper mines such as Escondida and Chuquicamata. The new mines did not yield output until the end of Q2. As such, TCs of imported copper concentrate in China fell to below $30/mt between January and mid-April, dropping to the lowest in a decade, and the smelters bore great pressures back then.

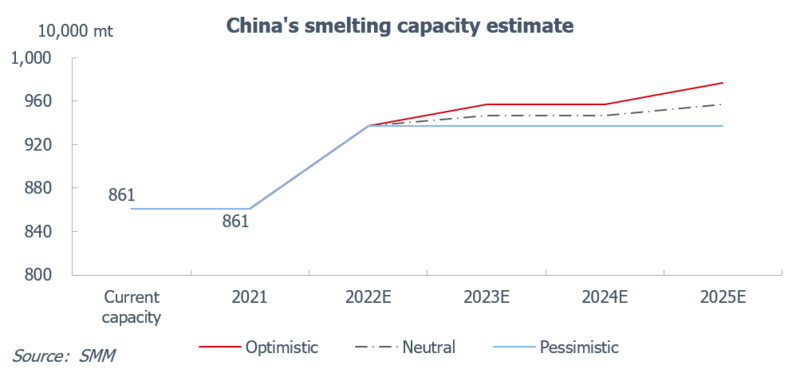

The new and expansion capacity of global copper mines was released from mid-April, while there were hardly any new smelting projects worldwide commencing production in the year. The production enthusiasm of mines has been boosted by continuously rising copper prices. Meanwhile, the global copper mines have been less threatened by the risks brought on by wage negotiations. In this scenario, spot TCs of copper concentrate have trended higher. With the commissioning and further release of new and expanded capacity, the copper concentrate supply and demand balance is expected to turn optimistic in 2022. Please refer to SMM annual report for where the global copper concentrate supply and demand balance will be heading next year and onwards.

China has experienced a rare nationwide large-scale power rationing since the second half of this year, out of a series of factors such as abnormal weather and energy structure upgrading. Companies were forced to temporarily suspend production due the power rationing. As far as SMM understands, the power rationing and production suspensions have so far swept through at least 10 provinces including Jiangsu, Zhejiang, Shandong, Fujian, Guangxi and Yunnan. In this regard, many people are confused as of why there are still frequent power rationing today even as China's hydropower, coal power and wind power have all achieved rapid development in recent years. And to what extent has the power rationing impacted the upstream, midstream and downstream sectors of copper cathode? For detailed analysis, please refer to SMM annual report.

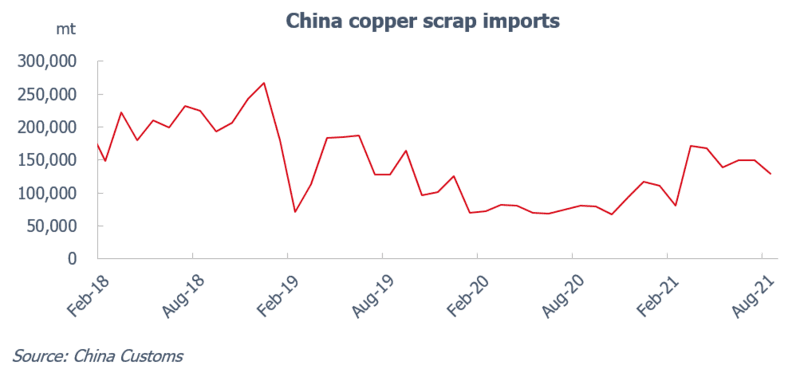

2021 is the first year that China has achieved zero import of solid waste and implemented the raw material standard of secondary copper/brass. Import companies have changed from hesitance to actively purchasing overseas products under the new standard. The import data has improved significantly, but the domestic supply shortage of copper scrap continued, which has intensified in the third quarter. In addition to the disruptions to overseas copper scrap supply from the COVID-19 pandemic, the domestic prohibition of waste imports and strict requirements on environmental protection also created many difficulties for the import of copper scrap. Meanwhile, Jiangxi's preferential tax policies for copper scrap are still attracting a large number of copper scrap processing capacity to come online, with the accumulated capacity reaching 10 million mt. The huge supply gap is another major driver of the continued shortage of domestic copper scrap supply. The supply shortage of copper scrap has boosted the recovery of copper cathode consumption, and its substitution effect has a significant impact on the copper industry. When can the supply of copper scrap improve? For detailed analysis, please refer to SMM annual report.

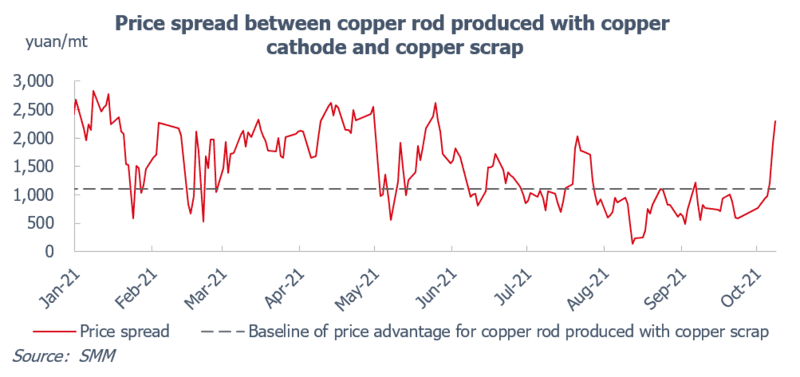

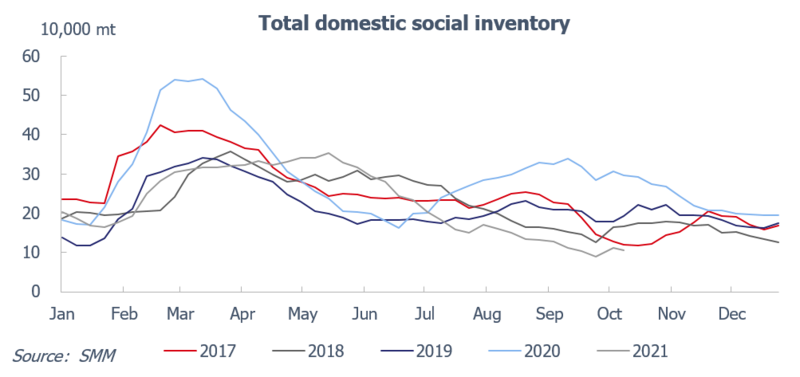

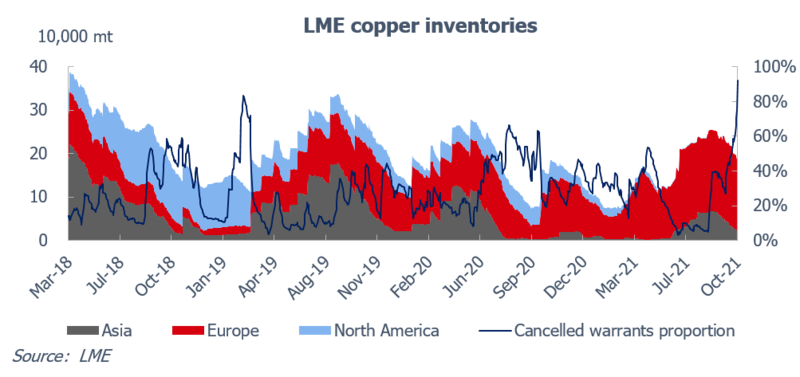

A large number of traders offered their copper scrap inventories that have been stored for many years for sale at the beginning of 2021 when the copper prices continued to rise. The price difference of between copper cathode and copper scrap once widened to around 3,000 yuan/mt, increasing the substitution of copper cathode by copper scrap. As such, the market inventory of copper cathode accumulated during the traditional peak season of April and May. However, with the fall of copper prices and the depletion of copper scrap inventory, the substitution effect of copper scrap has weakened since June. The copper cathode inventory unexpectedly declined sharply during the traditional off-season from July to August. The copper inventory in Guangdong fell to around 900 mt at one point amid the power rationing and maintenance at smelters. In contrast, LME copper inventories continued to rise during the year, up from a low of 75,000 mt to around 200,000 mt, but they were still at a historically low level. The proportion of LME cancelled warrants has risen to 92% in just a few days since October, lowering the copper inventory available for access to the lowest level since 1974. The LME 0-3 spread soared from discounts to premiums of over $1,000/mt amid a short squeeze. Why do the domestic and overseas inventories diverge? And what has resulted in the short squeeze overseas? For detailed analysis, please refer to SMM annual report.

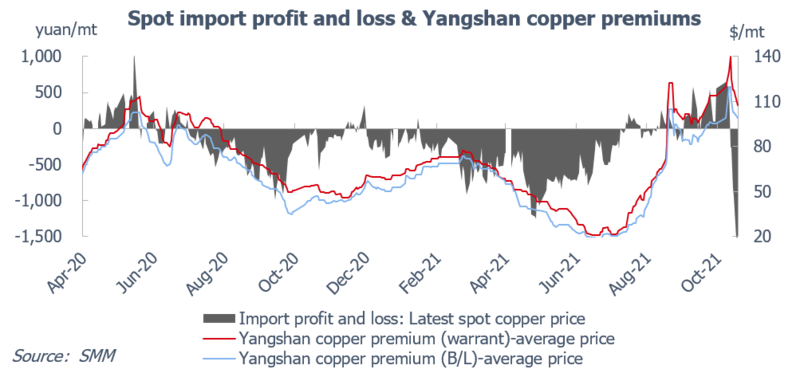

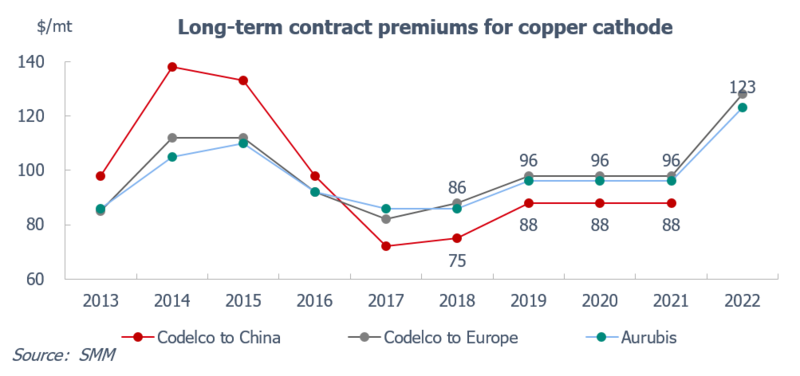

The copper import market has undergone great changes in 2021 and was completely different in the second half of the year from the first half. The import window has remained closed in the first half of the year, and the demand for customs declaration was extremely poor. Yangshan copper premiums have been falling all the way and even hit the lowest level in SMM's records. The long-lasting sluggish copper import market in China has resulted in varying degrees of declines in the amount of copper cathode exported to China by other countries. In Q3, due to the continuous disruptions to the production at domestic smelters, the domestic fundamentals were strong on the back of domestic power rationing, shortage of copper scrap and limited inflow of imported goods. The inventory continued to fall, and the SHFE/LME copper price ratio continued to rally. The spot import profit window has opened many times and the profit was lucrative, bolstering Yangshan copper premiums to exceed $140/mt. The opening of the import window has also prompted some traders to move overseas cargoes to China, but why we have not seen an increase in imports for a long time? And where will the benchmark in the Chinese market be standing as Aurubis and Codelco have substantially raised the premiums for copper cathode that will be shipped to Europe next year under long-term contracts? How will the traders respond? For detailed analysis, please refer to SMM annual report.