SHANGHAI, Aug 23 (SMM) – For LME zinc, the monthly retail sales in July in the United States fell 1.1% year on year. Some goods have been returned as the Fed has stopped offering relief payment to residents. The minutes of the Fed meeting last week showed that officers have discussed to reduce debt purchases, delivering hawkish signals. Weak macro front and expectations has aggravated the pessimistic sentiment in overseas markets. The backwardation of LME cash to the three-month contract rose to $1.5/mt. LME stocks accumulated 4,250 mt while the cancelled warrants fell 9,550 mt, showing that there were still hidden stocks overseas. It is expected that LME zinc will return to the contango structure. LME zinc prices are expected to stand at $2,900-2,990/mt this week.

Operating rates at smelters in Guangxi reached 90-100% from August 19 to 20 as power curtailment in Guangxi was eased; Hulunbuir Chihong suspended production, affecting about 12,000 mt of suplly for one month; government stockpiles suspended releasing in August but future releases could be expected. Supply temporarily declined, but will increase in the future. Consumption is not inspiring. Domestic galvanised zinc orders failed to increase further and export orders were muted. Dies-casting zinc alloy orders are likely to transfer into domestic market. Supply and demand are expected to weaken in H2, with macro fronts and released government stockpiles suppressing zinc prices. The most-traded SHFE contracts prices are expected to stand at 21,800-22,800 yuan/mt this week, spot premiums of Shanghai zinc stood at 180-230 yuan/mt over the September contract.

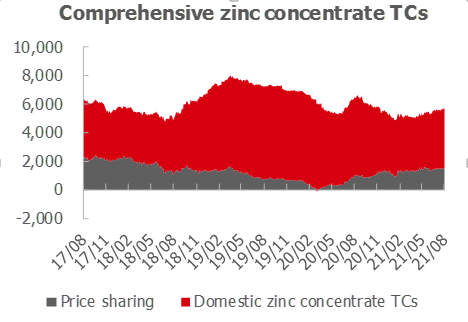

TCs across various regions were unchanged last week. Power curtailment in Guangxi ended gradually, with the capacity utilisation rates of Hechi Nanfang Nonferrous Yelian recovering to over 90%. Power restrictions in Yunnan exerted a limited impact on production at smelters. Huize basically returned to normal output while Yunnan Luoping Zinc & Electricity failed to achieve full capacity. Production in Sichuan stabilised. Demand signalled recovery. But arrivals of zinc concentrate at Fangchenggang Port thinned and supply in south-west China remained tight. Chihong Zn & Ge Co. is expected to suspend production for over 3 months due to accidents. There will be a sudden reduction in demand. Inner Mongolia has begun to assemble production reduction inspection teams to inspect the mines where accidents took place, which has not yet affected the production. Part of imported zinc concentrate has arrived in Lianyungang Port and smelters began to deliver goods. The overall inventory did not change much.