SHANGHAI, Jun 25 (SMM) – This is a roundup of China's metals weekly inventory as of June 25.

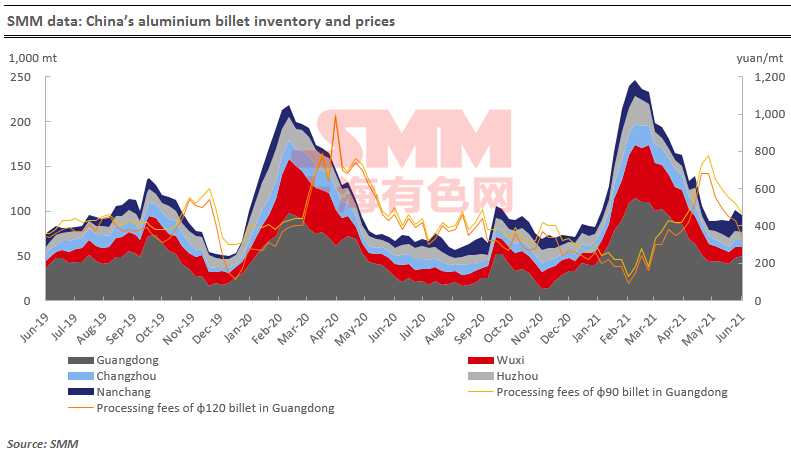

Aluminium billet inventories dropped 3,500 mt on week

The outbound volume of the aluminium billet dropped by 6,800 mt to 38,300 mt last week, a decrease of 15%.

Aluminium prices were mainly affected by the policies, macroeconomics, and fundamentals. Downstream purchase was low amid strong wait-and-see sentiment. The stocks of aluminium billet in five major consumption areas fell by 3,500 mt to 97,300 mt from the previous week, a slight decrease of 3%.

The inventories in Fushan and Changzhou increased by 1,900 mt and 400 mt respectively, while that in Wuxi, Huzhou, and Nanchang all fell about 2,000 mt. According to SMM survey, aluminium downstream orders declined, and the downstream companies were less willing to purchase after the release of national reserves was announced. The outbound volume of aluminium billet is expected to drop next week, and the inventories may increase.

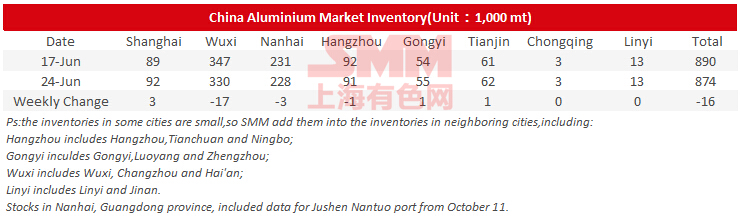

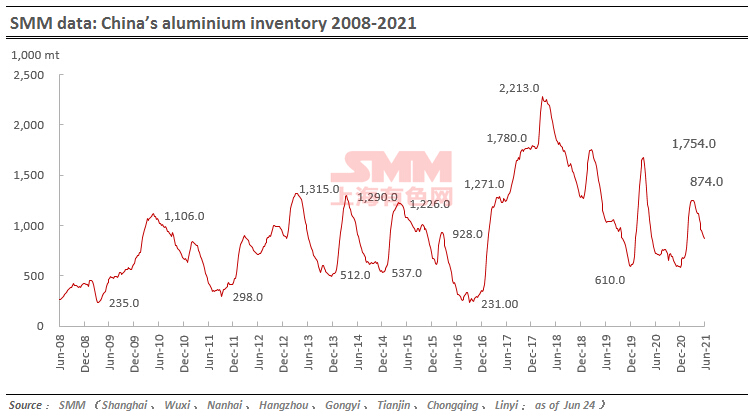

Primary aluminium inventories fell 16,000 mt on week

SMM data showed that China’s social inventories of aluminium across eight consumption areas fell 16,000 mt on the week to 874,000 mt as of June 24. The stocks kept falling in Wuxi and Hainan.

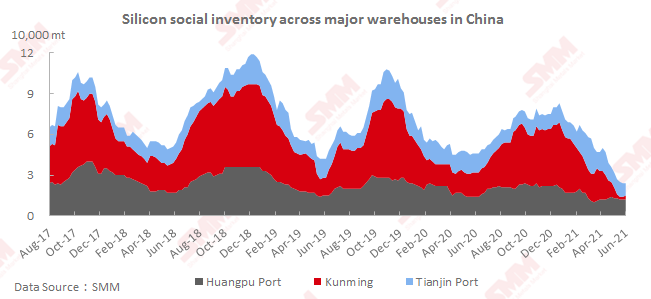

Silicon metal social inventories stood flat on week

Social inventories of silicon in Huangp port, Kunming, and Tianjin port totalled 24,000 mt, flat from a week ago.

The inventory in Kunming increased amid higher operating rates in Yunnan. The inventory at Huangpu port was largely unchanged. The silicon metal arriving at Tianjin port this week will also be shipped out within the week. Since the operating rates will drop in north China and rise in South China, the total silicon metal social inventories are expected to stand stable.

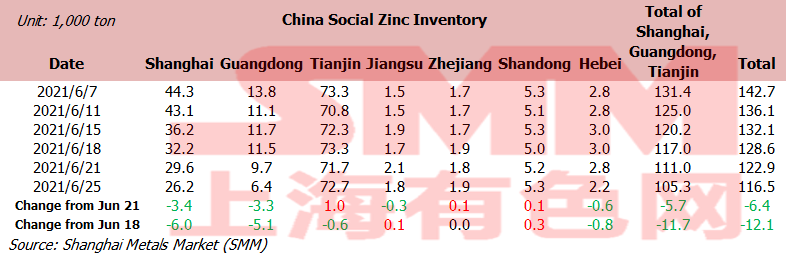

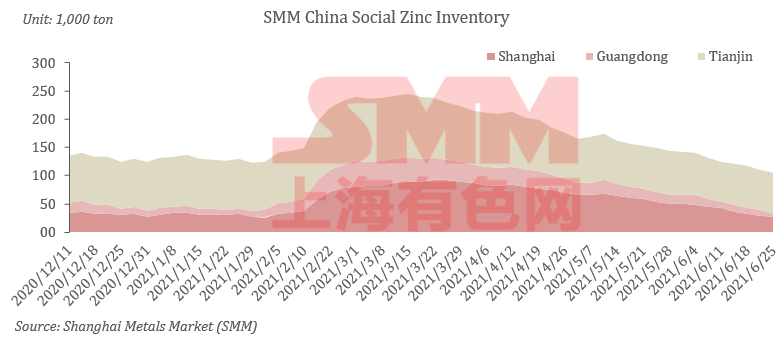

Zinc social inventories shrank 12,100 mt on week

SMM data showed that social inventories of refined zinc ingots across Shanghai, Tianjin, Guangdong, Jiangsu, Zhejiang, Shandong and Hebei decreased 12,100 mt in the week ended June 25 to 116,500 mt. The stocks fell 6,400 mt from Monday June 21.

Stocks in Shanghai continued to decrease as downstream demand for restocking increased when prices fell, and the inflow of imported zinc slowed down. In south China's Guangdong, downstream orders in the low-price range increased, and deliveries were made one after another in the week, driving stocks to hit a new low. Stocks in Tianjin fell slightly as overall downstream demand was still weak.

Stocks across the three major trading hubs (Shanghai, Tianjin and Guangdong) fell 11,700 mt this week, after an 8,000 mt decrease last week.

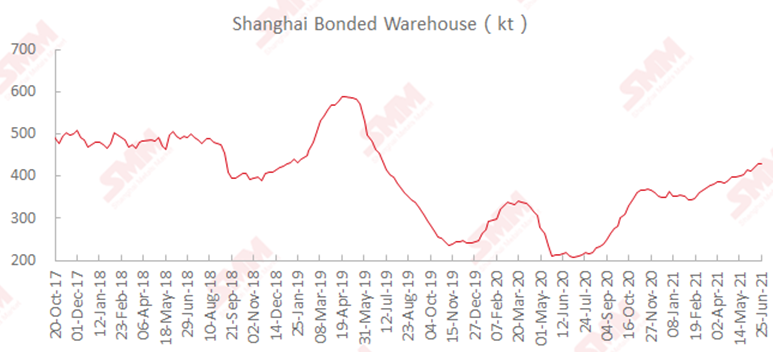

Shanghai bonded copper stocks rose 500 mt on week

Stocks of copper in Shanghai bonded areas increased on larger arrivals for the third consecutive week.

SMM data showed that the stocks rose 500 mt from the prior week to 429,800 mt as of Friday June 25. The growth rate narrowed significantly.

Terms of trade showed signs of improvement at the beginning of this week. The spot import loss narrowed to less than 100 yuan/mt, which stimulated the import demand for customs declaration. The buyer's demand for warehouse receipts and bills of lading arrived in recent months in the foreign trade market increased, and the Yangshan copper premium rebounded at the bottom.

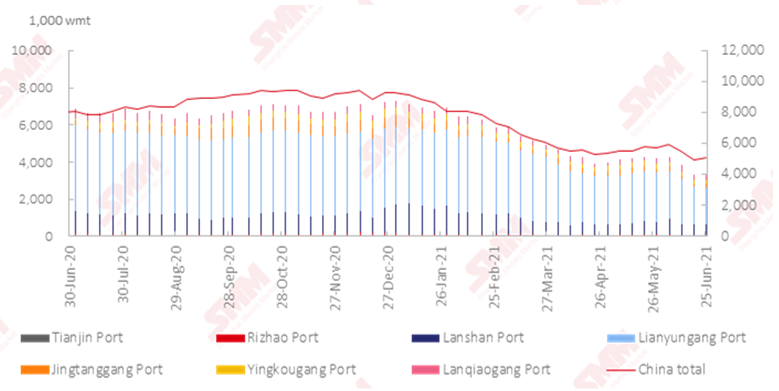

Nickel ore inventories at Chinese ports rose 137,000 wmt to 5.1 million wmt

Nickel ore inventories across all Chinese ports increased 137,000 wmt from June 18 to 5.1 million wmt as of June 25, showed SMM data.

In Ni content, the stocks stood at 40,200 mt.

SMM data also showed that nickel ore stocks across seven major Chinese ports increased 77,000 wmt during the same period to 3.4 million wmt.

Nickel ore stocks increased slightly this week, and inventories at Chinese ports remained stable. Nickel ore stocks were unlikely to increase significantly under the high domestic demand, and some ports still unloaded slowly recently. Time chartered vessels in July have been basically sold out with small market circulation.

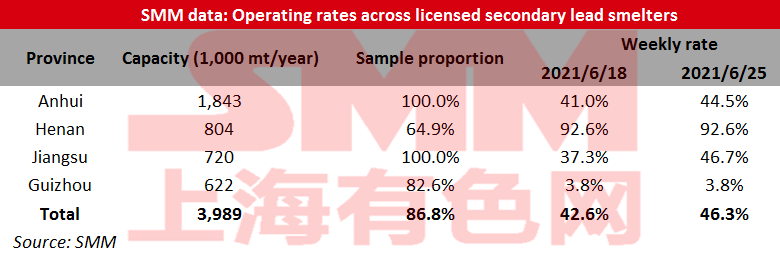

Secondary lead operating rates rose to 46.25% on week

Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 46.25% in the week ended June 25, up 3.7 percentage points from the previous week, showed an SMM survey.

The operating rate in Anhui rose 3.56 percentage points on the week to 44.53% as the smelters gradually resumed production from maintenance. Some companies in Jiangsu that were suspended due to technological transformation also resumed operation this week, and secondary lead output increased. Jiangxi Xinya is expected to recover normal production next week, the production of large plants in Anhui will further recover, and other large smelters will gradually resume work. Operating rates are expected to rise next week.

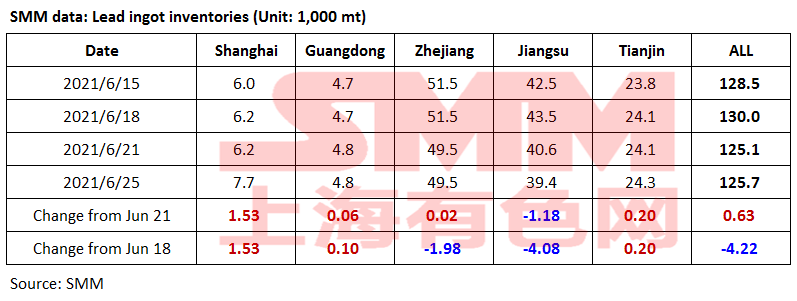

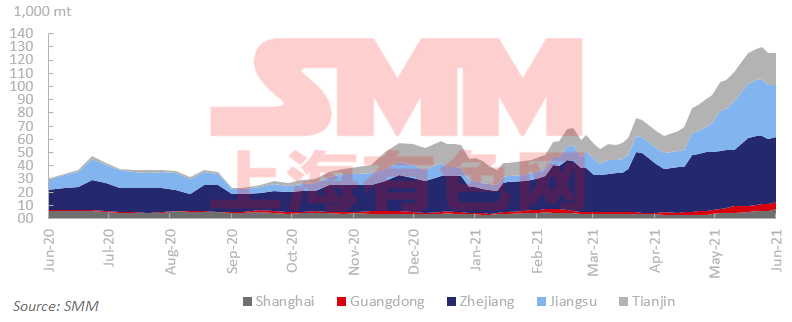

Lead ingot social inventories down to 125,700 mt on week

Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 4,200 mt from the prior week but rose 600 mt from June 21 to 125,700 mt as of Friday June 25, an SMM survey showed.

Lead supply did not fully recover amid maintenance in both primary and secondary lead smelters. Secondary lead smelters held prices firmly for shipments, and the demand turned to primary lead at lower prices early this week, leading to the decline in lead ingot inventories. However, lead prices fluctuated upward later this week, and downstream purchase declined due to the high prices. The discounts of secondary refined lead expanded to 350-250 yuan/mt (ex-factory) over the average price of SMM #1 lead as of June 25. Downstream rigid demand switched to the secondary lead, and lead ingot inventories increased slightly. Currently, secondary lead smelters are more active to ship goods amid recovered profits. If the consumption does not rebound significantly, lead ingot social inventories are likely to further increase.

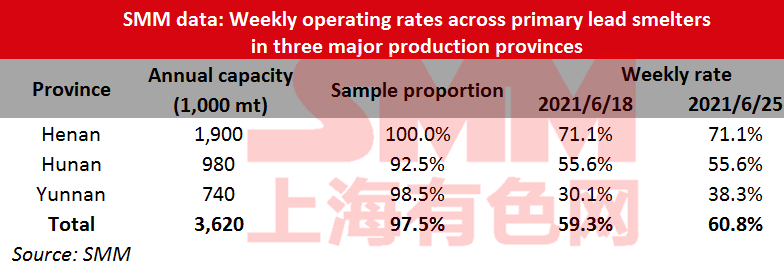

Primary lead smelter operating rates rose to 60.8%

Operating rates across primary lead smelters in Henan, Hunan and Yunnan provinces gained 1.5 percentage points from the previous week to 60.8% in the week ended June 25, showed an SMM survey.

Henan and Hunan saw normal primary lead production this week. Hunan Chenzhou Xiongfeng has stopped the crude lead production line recently, and is expected to resume the production of refined lead and crude lead in July. Henan Shibin cancelled the production cut plan for the insufficient raw materials, and maintained normal production. Yunnan Hongqian resumed production this week, but not in full capacity.

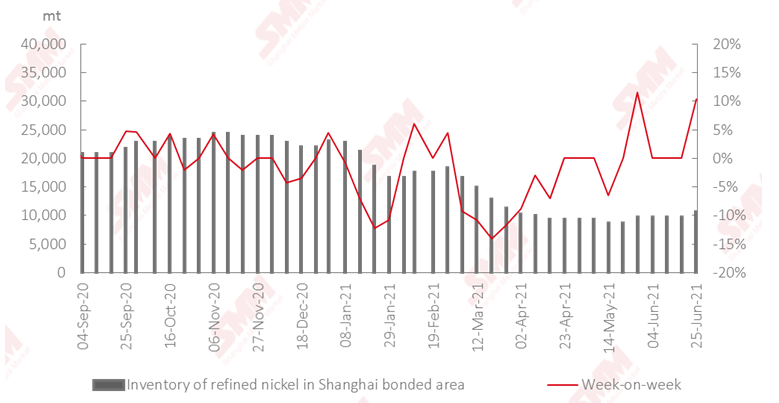

Shanghai bonded refined nickel stocks rose 1,000 mt on week

Inventories of refined nickel in the Shanghai bonded areas increased 1,000 mt from a week ago and stood at 10,700 mt as of June 25, showed SMM data.

It was reported that more than 1,000 mt of nickel plates arrived in ports from LME warehouse last weekend, and some of the goods were moved into the bonded area. The domestic nickel plate premium was still at a high level this week, and the import window opened after SHFE nickel rose sharply on Wednesday. It is reported that the offer and inquiry of US dollar goods have obviously picked up, and it is expected that the supply of goods in the bonded area will continue to flow into China in the later period.

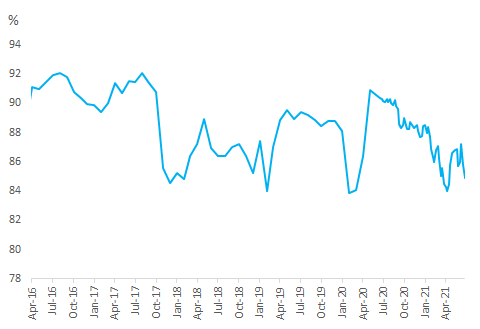

Operating rates of blast furnaces across Chinese steelmakers fell 0.9 percentage point on week

Operating rates of blast furnaces at steel mills fell 0.9 percentage point from a week ago and decreased 0.8 percentage point from a month ago to 84.9% as of June 24, SMM survey showed. Nearing the 100th anniversary of the founding of the Party, production restrictions in Hebei, Tangshan and other places have strengthened, and other areas have also strictly carried out safety and environmental inspections. In addition, the demand entered the off-season. Stocks increased across the country. Steel plants have different levels of maintenance plans. It is expected that operating rates of blast furnaces will still maintain a downward trend next week.