SMM, Feb. 10:

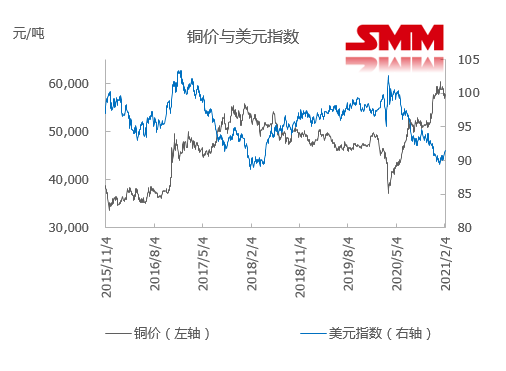

After the advent of 2021, copper prices as a whole showed a trend of horizontal consolidation. Driven by the arrival of Biden at the beginning of the month and the expectation of a new round of stimulus bills, copper prices surged above 60000 yuan / ton all the way, reaching a peak of around 60800 yuan / ton. Before the end of January, due to the continuous tightening of the liquidity margin of the domestic central bank, commodity and financial markets gave up their previous increases one after another. the pattern of high shocks in copper prices since late January was broken. After a continuous correction, the center of gravity of Shanghai copper fell to the range of 57000-58000 yuan per ton. while Lun Copper fluctuated around 7800 US dollars per ton, from a macro point of view, the promotion process of the new round of fiscal stimulus bill in the United States has been repeatedly thwarted, and the recent US economic data are better than expected. The stronger-than-expected performance of US factory orders in December showed that the manufacturing sector was strong. The ADP data on Wednesday and the data on initial jobless claims last week on Thursday were both good, and the macro data were all positive. As a result, gold fell below the 1800 mark and the dollar index rose to 91.5, although the strong and high dollar put pressure on copper prices. However, the rise and rebound of crude oil has given some support and guidance to base metals. Us crude oil has been rising for five consecutive years, breaking through 57 US dollars per barrel, brushing the new high in the past year, indicating the effect of OPEC production reduction and the recovery of confidence brought about by the gradual economic recovery, which has contributed to the rise in metal prices to a certain extent.

On the supply side, the news of the storm problems in the ports in northern Chile and the re-imposition of the epidemic blockade in Peru intensified expectations of a tight spot market for copper concentrate, and the spot TC continued to decline. As of January 29, the SMM copper concentrate import index was $43.85 / ton, down $2.32 / ton from the previous week. The tension at the raw material end is transmitted to the domestic smelting end, and the inflow of imported copper is also relatively limited. In the off-season of domestic consumption in January, supply fell short of demand. The rising water price in Shanghai has also risen, and it is even difficult to see the discount market before the festival. Overall, fundamentals still supported copper prices in January.

At the beginning of this month, Shanghai copper opened at 57820 yuan / ton. Biden was optimistic about the stacked US economic data on Taiwan. Copper prices surged through the 60000 yuan / ton mark led by the outer disk. At one point, after rising to 60800 yuan / ton, Trump's series of operations led to market panic about the possible black swan incident, superimposed by a series of liquidity tightening operations that the Federal Reserve said at the meeting, such as possible bond purchases, which instantly cooled the market mood. Copper prices returned to a narrow range of 58000-59000 yuan / ton, and at the end of the month, with the turn of domestic liquidity, the dollar index continued to rise, the copper price operation center moved down again, and finally closed at 57550 yuan / ton, a drop of 0.79% within the month, leaving a long upper lead. Lun Copper, driven by the US stimulus bill, was slightly stronger than Shanghai Copper, opening at US $7784 / ton and finally closing at Cross Star. With the return of the Spring Festival holiday in February, stronger domestic consumption led to stronger fundamentals to support copper prices on the Brin middle track.

After the festival, it is expected that the copper price operation hub will move up slightly, and the center of gravity will remain at a high level.

After experiencing the liquidity performance of the central bank at the end of January, squeezing some of the gains in the stock market and commodity market, after entering February, the central bank has started 270 billion reverse repurchase plus 100 billion 14-day reverse repurchase on February 4. for the upcoming Spring Festival capital peak, the central bank will certainly focus on stable liquidity expectations, and there has also been a significant rebound in market confidence before the festival. The copper market has been supported and rebounded obviously after the bottom, and the departure of the bears has also laid a technical foundation and confidence for the bulls to enter the market in the future. Technically, the copper price regained the support of the recent average on Friday after briefly touching the bottom of Brin and falling below all averages. On February 8th and 9th, it continuously jumped high and broke through all the moving average pressure, and effectively broke through the Bollinger middle rail and stood firm at the 59000 yuan / ton mark.

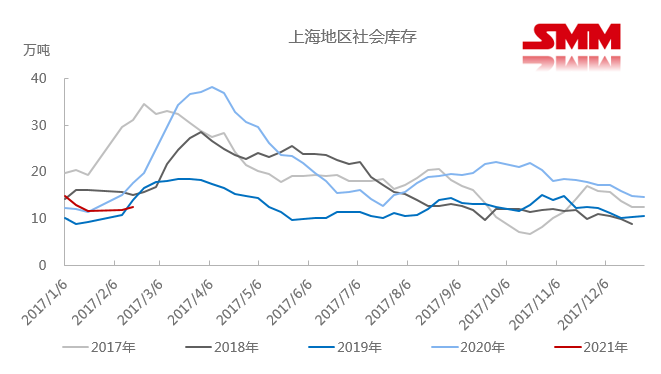

From a fundamental point of view, although the traditional Spring Festival effect has a certain negative effect on copper consumption, the holiday time of copper processing enterprises varies greatly during the long Spring Festival holiday in 2021, and the enterprises with shorter holiday time are mainly concentrated in the export-related home appliances. Electronics industry, clothing luggage and plumbing industry, that is, enamelled wire, copper pipe, copper strip and copper bar and other industries. Some central and state-owned enterprises have taken the lead in responding to the call of the state to encourage employees to celebrate the Spring Festival locally according to the production situation of the enterprises and the wishes of their workers. it is expected that after the seven-day Spring Festival holiday, these enterprises will start work soon and return to work in a timely manner. to form a certain degree of confidence and support for post-holiday consumption. Overall, the market the week before the festival did not show the momentum of accumulation in previous years, according to the SHFE inventory report last Friday, inventory in Shanghai decreased by 3781 tons, Guangdong decreased by 499 tons, according to SMM bonded warehouse weekly inventory data showed that last week the bonded warehouse decreased by more than 7000 tons, indicating a reduction in import declaration, market supply-side reductions and post-holiday consumption rebound expectations, but also to the market long waiting for confidence. There are only two trading days left in China this week. Shanghai Copper 2103 contract shows a slight decline after rising. It is expected that the overall operation in February will be 58000-60000 yuan / ton, the international copper 2103 contract will run at 52000-53500 yuan / ton, LME still has two trading days in the week, and Lunchong is expected to run at 7950-8150 US dollars / ton.

"Click to view the SMM metal industry chain database

![This week, copper social inventories in major regions of China continued destocking [SMM weekly data].](https://imgqn.smm.cn/usercenter/XBbTq20251217171709.jpg)

![Macro Factors Weigh on Copper Prices, SHFE Copper Inter-Month Spread Occasionally Sees Backwardation Structure [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/CJXfS20251217171710.jpg)