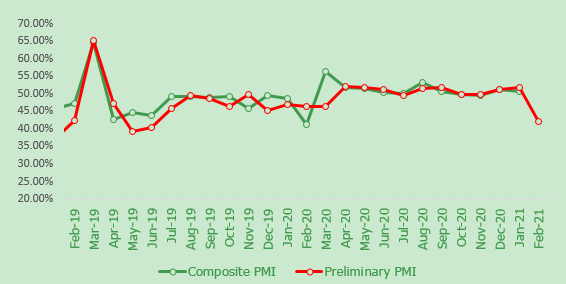

SHANGHAI, Feb 2 (SMM) – SMM data showed that the purchasing manager's index (PMI) for downstream nickel industries, including stainless steel, electroplating, alloy and battery, stood at 50.61 in January, down 0.49 points from December. A reading above 50 indicates expansion, while a reading below 50 indicates contraction.

Production sub-index continued to decrease and remained below 50, planned output of #300 stainless steel fell

The composite sub-index for production in January decreased 3.93 points from December to 45.86, staying in contraction. The production sub-index in the stainless steel sector fell 3.83 points month on month to 45.24, remaining in contraction, as most stainless steel plants were operating normally while some large-scale steel plants had a decline in production due to rotation maintenance. The production sub-index in the electroplating sector came in at 49.67 in January, and the overall operating rates also declined slightly compared with December.

New orders sub-index fell below 50, orders of most sectors except electroplating were stable

The overall sub-index for new orders in January fell slightly by 0.89 point month on month to 49.83 in December, falling into the contraction range. The new order sub-index of the electroplating sector declined sharply from 53.24% in December to 49.67% in January, also falling into the contraction range, as operating rates of the downstream hardware and bathroom sector decreased during the Chinese New Year, and some electroplating companies have scheduled their holiday and shutdown plans, which also affected orders. The new orders sub-index in the stainless steel sector stood at 50%, flat from December and November. The improvement in foreign trade has significantly boosted the stainless steel products sector, and steel mills’ orders and shipments have also remained stable from the previous two months, significantly better than the same period in previous years.

Raw materials inventory sub-index increased significantly, many downstream companies actively restocked before CNY

The composite sub-index for raw materials inventory in January gained 17.51 points month on month to 67.07, returning to expansion. The raw material inventory sub-index in the stainless steel sector rose 21.9 percentage points from December to 69.05%. The profit of stainless steel plants in January improved significantly, and steel mills’ restocking willingness is relatively active. The raw material inventory sub-index of the electroplating sector rose to 54.58%, as most of electroplating plants normally restocked in January, and some large-scale electroplating plants planned to produce during the CNY holiday, leading to centralised restocking. Due to the booming orders in the alloy sector, alloy companies started active stockpiling for CNY in January, and the raw material inventory sub-index rose to 53.5%. The raw material inventory sub-index in the battery sector stood at 68.79%, down 16.97% from the previous month. Although the index sub-was lower than the previous month, it was still much higher than 50, mainly because January is regarded as the high season of CNY stockpiling and most companies were bullish on raw materials in the near term, urging all companies to restock raw materials actively.

Finished goods inventory sub-index continued to improve and stayed in expansion, inventories at stainless steel plants remained decreases

The overall sub-index for finished products stocks rose 3.98 points on the month to 66.62 in January, staying in expansion. The sub-index for the stainless steel sector increased by 3.81 points month on month to 69.05. Finished products stocks across steel mills showed a downward trend due to better-than-expected consumption with low planned output of steel mills and the delivery plans of major mills. Many steelmakers experienced delays in the delivery of orders this month, and social inventories also declined slightly accordingly.