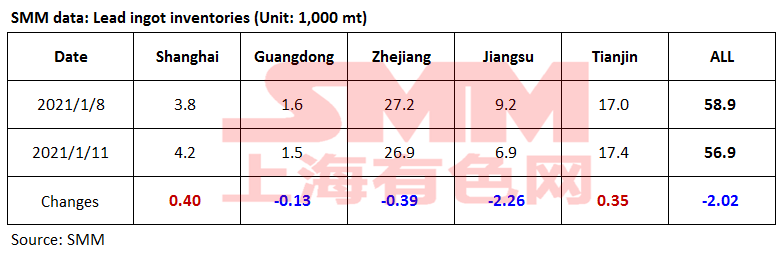

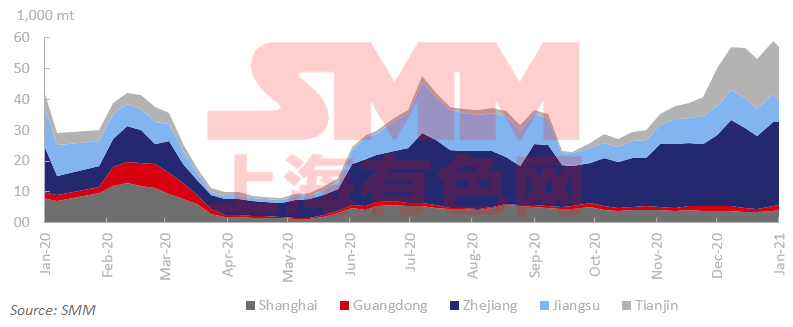

SHANGHAI, Jan 11 (SMM) – Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin fell 2,000 mt from last Friday January 8 to 56,900 mt as of Monday January 11, an SMM surveyed showed.

The cold weather and Covid-induced transport restrictions slowed shipments to social warehouses. Besides, falling lead prices deterred smelters from selling. As of January 11, discounts of secondary lead narrowed to 100-150 yuan/mt, ex-works, against the average price of SMM 1# lead. Some downstream users switched to the trade market. Secondary lead smelters in Inner Mongolia and Hebei suspended production from this week due to the COVID-19 outbreak and shortages of battery scrap.

![Secondary refined lead traded at a discount ex-factory, and enterprises' losses remained hard to reverse [SMM Secondary Refined Lead Weekly Review]](https://imgqn.smm.cn/usercenter/yqTpQ20251217171721.jpeg)

![Domestic Secondary Crude Lead Transactions Follow the Market, Short-Term Inflows of Imported Crude Lead Remain Low [SMM Secondary Crude Lead Weekly Review]](https://imgqn.smm.cn/usercenter/XMxKT20251217171720.jpeg)

![Smelter production cuts limit raw material demand, limiting upside room for scrap batteries [SMM Scrap Battery Weekly Review]](https://imgqn.smm.cn/usercenter/qnyHQ20251217171721.jpeg)