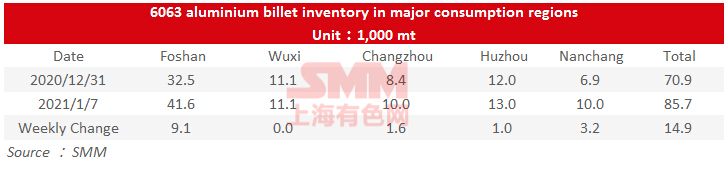

SHANGHAI, Jan 7 (SMM) –SMM data showed that stocks of 6063 aluminium billet across the five major consumption areas – Foshan, Wuxi, Huzhou, Changzhou and Nanchang – in China expanded 14,900 from the prior week to 85,700 mt as of January 7. Stocks were stable in Wuxi, but built up in the other four areas, with Guangdong seeing the largest increase in aluminium billet stocks which increased 9,100 mt on the week to 41,600 mt. Stocks expanded 3,200 mt to 10,000 mt in Nanchang, while rose slightly by 1,600 mt and 1,000 mt in Changzhou and Huzhou respectively.

![Some aluminum plants in the Middle East announce production resumptions, overseas daily average aluminum production up 1.6% MoM [SMM Analysis]](https://imgqn.smm.cn/usercenter/BCdNp20251217171653.jpg)