SMM7 March 13: against the backdrop of a pick-up in macro sentiment and optimism in the capital market, non-ferrous metals are strongly pulled up, and Shanghai lead is no exception. Coupled with the existence of 07 contracts forcing the market, the main 2008 contract today reached 15545 yuan / ton, closing at 15460 / ton as of today, an increase of 2.42%. However, the development of the epidemic situation in the United States is still serious, and the domestic need to pay attention to the impact of the flood season on the lead industry chain, there are still great uncertainties in the macro level.

The fundamentals of lead are still weak. On the one hand, there was a certain increase in lead supply in July, mainly from recycled lead. With the continuous rise of lead prices, the profits of recycled lead have been repaired, and the production enthusiasm of recycled lead enterprises is better. It is expected that the operating rate of recycled lead enterprises will continue to increase in July. On the other hand, downstream consumption has not yet improved, traders and battery manufacturers are afraid of high and careful mining, only to maintain just demand, coupled with the current recycled refined lead to maintain a deep discount, today's average price of SMM1# lead mainstream quotation at 350m / ton, downstream procurement tends to recycled lead deep water supply, the demand for electrolytic lead is limited. Overall, lead is currently in a state of oversupply, and according to SMM research, the social inventory of lead ingots has risen for nine consecutive weeks. As of July 10, the total inventory of lead ingots in the five places reached 36500 tons, an increase of more than 2700 tons over the week of July 3, confirming this. And the current futures disk price is much higher than the spot, primary lead refineries and traders tend to deliver, the previous warehouse receipt inventory will maintain growth, the social inventory of lead ingots is expected to maintain growth this week.

"Click to view the SMM lead industry chain database

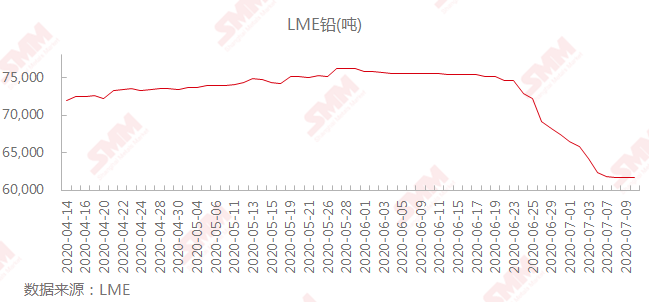

However, SMM believes that Lun lead stocks have continued to decline since June 17. As of July 10, LME lead stocks stood at 61675 tons, down 14475 tons from the high since the beginning of the year, indicating to a certain extent that overseas consumption is recovering one after another, and that the lead consumption peak season in the third quarter may be coming. However, the position of the domestic Shanghai lead 2007 contract remains high, which deviates from the warehouse receipt inventory, and the macro atmosphere has improved, and the short-term lead price is expected to rise.

Click to sign up for SMM 2020 (15th) lead and Zinc Summit

Scan the QR code in the picture to sign up for the lead-zinc summit and fill in the personal information on the last page. The meeting staff will contact you later!