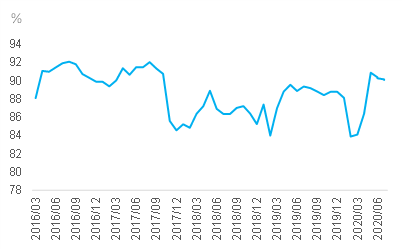

According to SMM research, the operating rate of blast furnace in the second week of July was 90.1%, down 0.06% from last week. It is estimated that the operating rate will pick up slightly next week.

Since the beginning of this week, the stock market has risen sharply, and market sentiment has picked up somewhat. Superimposed with the news that the Brazilian president has unfortunately infected with the new crown, the market is worried about the contraction of the ore supply side and rekindled the enthusiasm for long ore. Today, the iron ore 09 contract increased by 53000 hands, up 2.74%, continuing to lead the rise in black. Rebar futures also broke through 3700 points, reaching a seven-month high. At present, the contraction of the supply side of steel mills is still continuing. according to the latest research data of SMM, as of July 7, the operating rate of independent electric arc furnace steel mills reached 73.24%, down 4.49% from the same period last week and 11.52% from 84.76% in the same period in June. On the demand side, the market is generally worried that the rainstorm and the college entrance examination will affect the release of short-term demand, but from the actual transaction data, the release of demand is not pessimistic. Driven by strong futures, traders are enthusiastic about replenishment. The trading volume of building materials in the past two days is more than 250000 tons. Once the late weather comes out, demand is expected to recover strongly.

In the context of abundant liquidity and good macro-economy, it is expected that this round of steel price rebound is expected to continue.

Fig. 1 the operating rate of blast furnace has dropped slightly for four consecutive weeks.

Source: SMM Steel

Specific research feedback:

Steel mill A (East China): part of the hot metal has been transferred to produce strip steel, and the strip steel profit is slightly better.

Steel mill B (South China): production is normal at present and there is no maintenance plan.

Steel mill C (Huazhong): the output of building materials has decreased, hot metal has been transferred to hot and cold rolling, and the inventory is high.

Steel plant D (southwest): normal full-load production, now the output is the historical peak, inventory has increased, later may be scheduled for maintenance, but has not yet set a time.

Steel plant E (North China): 4000m3 blast furnace shutdown and maintenance is not over, other rolling lines take turns for maintenance.