SMM7 June 6: the LME metal market has ups and downs this morning. As of 09:30, Lunxi copper, aluminum and nickel rose nearly 0.3%, Lunxi was flat, Lunxi lead fell nearly 0.1%, and Lunzn zinc fell nearly 0.4%. Domestically, Shanghai nickel rose nearly 0.8%, Shanghai aluminum rose nearly 0.6%, Shanghai tin rose nearly 0.4%, Shanghai zinc fell nearly 0.2%, and Shanghai copper and lead fell nearly 0.5%.

On the copper side, on the supply side, copper prices continued to rise last week. Some scrap copper suppliers kept a gambling mentality and were reluctant to sell. When copper prices fell over the weekend, they began to avoid risks. High copper prices were still good for scrap copper merchants as a whole. On July 1, the recycled copper (brass) standard has officially landed on schedule, and the relevant departments are speeding up the introduction of relevant qualification certification and regulatory measures, but it will take some time before they are actually available. According to SMM, industry insiders have high expectations for the availability of the new standards in September, and they still rely on approvals to import scrap copper for the time being, but most enterprises have basically run out of approvals in the second quarter. In order to make up for the gap, China has a high enthusiasm for the import of copper ingots which are not restricted by approval documents. At present, the data of the application for approval for the third quarter of the waste enterprises have been submitted, but according to the trend of decreasing approval every quarter, some views think that the volume of the new round of approval should not be very large, and the landing of the recycled copper standard will also have an impact on the subsequent approval volume, so it is difficult to make a judgment in terms of policy.

[selected SMM Weekly] Copper prices continue to be good for the scrap copper industry, but the level of start-up is still restricted by raw materials.

In terms of aluminum, the average spot price of Guangdong aluminum ingots was 14334 yuan / ton last week, up 234 yuan / ton from the previous month, exceeding the spot price at the end of January. During the week, the Shanghai Aluminum Index closed at the real positive line, with the main contract rising by more than 3%, breaking through and standing firmly in full digits, and the difference between July and August widened sharply from 160 yuan / ton to 300 yuan / ton. Guangdong aluminum ingot spot to futures upward discount trend downward, from about 300 yuan / ton to 150 yuan / ton, the spot price gap between Guangdong and Shanghai narrowed slightly to 30m / ton 80 yuan / ton. The inventory of aluminum ingots in Guangdong on Friday was 154800 tons, an increase of 3300 tons compared with last Wednesday. Futures rose sharply, the spot is relatively weak and weak; northern aluminum ingots and imported aluminum ingots arrived, the supply of goods in circulation in Guangdong increased during the week, downstream just need to purchase mainly. Traders are actively shipping, the basis and monthly difference structure is not conducive to spot hedging, the implementation of long orders is normal, the market is more bearish followed by rising water, the monthly difference also has a further expanding trend. It is expected that the spot price gap between Guangdong and Shanghai is expected to narrow this week and continue to narrow.

[SMM Weekly report selected] the monthly difference of aluminum will rise sharply, expand inventory, increase the basis and fall back.

Lead, lead fundamentals, the market is expected to deliver nearly 20,000 tons, smelters are now gradually expanding spot discount, social inventory continues to accumulate, from the traditional trading logic of lead, lead fundamentals are relatively weak, but due to low lead precipitation funds, serious capital control, short-term does not rule out the main funds to continue to enter the market to drive up prices, so from the perspective of lead fundamentals, the current high level is more likely to fall. In the primary lead market, it is understood that during the Dragon Boat Festival, some lead battery production enterprises have a holiday of 1MUR for 3 days, while smelters produce more normally, while lead prices rise all the way after the festival, and the downstream just need to replenish the warehouse is limited, while the profits of recycled lead are gradually repaired, and the recycled lead sticker expands rapidly, so that the inventory of electrolytic lead smelters continues to transfer to the warehouse, and the growth rate is larger than that before the festival. In addition, this week, some primary lead smelters went into overhaul, but the recycled lead discount showed no sign of narrowing for the time being, suppressing electrolytic lead trading; the price difference of another lead contract widened, the spot maintained the discount trade, and some holders intended to deliver their positions. Social inventory may continue to increase this week.

[SMM Weekly selected] lead ingot social inventory accumulation fundamentals are weak and lead prices are expected to fall back.

In terms of zinc, as far as Shanghai zinc is concerned, Shanghai zinc maintained a range concussion last week. The performance of overseas employment data is eye-catching, and the macro mood has obviously picked up, but the boost for Shanghai zinc is relatively limited, mainly because the fundamental support is still weak. This week, with the increase in domestic zinc concentrate supply, smelter raw material inventory rebounded. Under previous mining and metallurgical negotiations, zinc concentrate processing fees were raised for the first time in a year, with local increases of around 100m / t, boosting smelters' willingness to produce. In addition, Xing'an copper and zinc production resumes, Chifeng medium color goes into overhaul, and imported zinc is affected by ratio downwards. it is expected that it is difficult to increase the inflow of imported zinc this week, which is basically the same as last week, so on the whole, the increment on the supply side is still greater than the reduction. From the consumer point of view, with the end of the rush brought by the semi-annual report, the orders of most galvanized enterprises fell, the start of galvanized sheet enterprises was relatively stable, the orders of galvanized pipe and other structural enterprises were more differentiated, and the profits of small and medium-sized enterprises were poor; alloy enterprises weakened again, the smelter squeezed orders and domestic demand came together, and the orders remained weak. The zinc oxide plate is stable and good, and the warming of the automobile plate drives the zinc oxide enterprises to start work. On the whole, there is still no bright spot on the consumer side. From a technical point of view, the lower 20-day moving average support is stronger, but the MACD index is about to become a dead cross, indicating that Shanghai zinc may have downward momentum. Although the fundamentals are weak, the macro positive mood is strong, and it is expected that Lun Zinc may fluctuate in the range of the 20-day moving average. Overall, Lun Zinc is expected to run at US $2,050 per ton this week; 2008 of the main contract for Shanghai Zinc is expected to run at 16550 Mel 17150 yuan / ton, and the spot side is expected to raise water around 40 Mel 80 yuan / ton in July.

[selected SMM Weekly] overseas economic stimulus boosts macro Shanghai and zinc fundamentals are weak and are expected to fall back.

In terms of nickel, the weekly nickel price basically fluctuates around the previous position, and the fundamentals are weak but mostly known news, such as the increase in the supply of nickel pig iron and the pressure on stainless steel market shipments in the off-season, etc., on the whole, the short-term contradiction is not obvious; in the macro aspect, some overseas data are bright, and in the major links, we can see that overseas countries are still following the logic of consumer recovery, coupled with national policies to support enterprises have a certain effect, macro relative preference; Under the comprehensive action, the nickel price fluctuates in the range. Due to the sharp rise in nickel prices on Friday, and there are no obvious positive factors in the fundamentals, including the protest by residents near Weda Bay on Friday, which seems to be hyped, the effect on the market may be limited, and the mindset of shorting when going high is obviously enhanced. Nickel prices are likely to fall back high next week, focusing on whether long positions can hold on to a breakthrough. Shanghai nickel 102000 won 107,500 yuan per ton, Lunni 12650 won 13300 yuan per ton.

[SMM Weekly selection] the limited delivery makes Jinchuan Nickel Shengshui temporarily strong and the overall trading atmosphere is still low.

Tin, last week Shanghai tin 2009 contracts showed an overall upward trend of concussion. At the beginning of the week, tin opened at 137920 yuan / ton in Shanghai. At the beginning of the week, weak demand in the lower reaches of the week pulled down spot prices. Futures prices fell somewhat, reaching the lowest point of 136680 yuan / ton in the week, and then bottomed out. Bulls entered the market, giving up the decline and rising at the beginning of the week. The horizontal market fluctuated in the middle of the week, and its bulls continued to enter the market on Friday from the night market, reaching a weekly high of 140240 yuan / ton in the morning. After briefly breaking the pressure level of 140000 yuan / ton, it fell back to close at 139790 yuan / ton. The weekly level rose 1700 yuan / ton, or 1.23%, with 116000 hands traded and 29161 positions, an increase of 25521 hands. During the week, the main force of tin in Shanghai is positive, the physical part is above all weekly lines, and the lower shadow line is supported by the 5-week moving average. In terms of indicators, the opening of weekly MACD indicators is still upward, while that of daily MACD indicators is downward, but there is a trend that the two lines intersect and form a golden fork. The daily and weekly K lines are close to the upper track of the Bollinger belt. By the close of trading on Friday, Shanghai tin returned to the high level of the previous year's platform, and the gap due to the decline in the epidemic has been basically made up, and the downside space is limited in the short term. Bulls continue to enter the market on Friday, considering its position cost, the pressure above is expected to be near the year-ago high of 140500 yuan / ton in the short term.

[SMM Weekly Special topic] the overall upward trend of tin in Shanghai shows a concussive upward trend, and the discount is significantly lower than that of last week.

In terms of the black system, the thread rose nearly 0.2%, the hot coil fell nearly 0.1%, stainless steel, coking coal and iron ore fell by nearly 0.4%, and coke fell by nearly 1.2%. Last week, the thread trend was strong before and after, and in the first half of the week, terminal demand seasonally weakened, superimposed by the second outbreak of the epidemic in the United States sparked fears of global economic uncertainty, the market was cautious and empty, and the spot market was due to the epidemic in the north and rain in the south. In particular, procurement at construction sites along the Yangtze River has been delayed under the attack of heavy rain, and prices have been moving down all over the country. By the end of the week, the news that production restrictions on environmental protection in Tangshan had been strictly implemented this time had boosted the spot market and recovered a small part of this week's decline. Last week, the current price of the hot volume period was first weak and then strong, and basically returned to the pre-festival level as of Friday. Last week, affected by the inventory decline and increase, the market mentality changed from optimism to caution, superimposed thread rainy season drag, resulting in the early week volume trend continued to be sluggish, the terminal affected by the procurement rhythm has also slowed down. Later, with the continuous heating up of the news of environmental protection production restrictions and the stimulation of the macro good news, the black department rebounded strongly, driving the volume to follow the rise, prompting the market mentality to pick up, and the terminal procurement and speculative receipt were also more active than at the beginning of the week, and the transaction rebounded.

[selected SMM Weekly] the rainy season is coming out of the steel price rise.

Crude oil rose slightly in the last period and the number of new confirmed cases in the United States surged, raising concerns that the recovery in energy demand could stall. The United States is the world's largest oil consumer. On the data side, preliminary assessments of energy intelligence show that although West African members still do not comply with the agreement, the 10 OPEC members participating in OPEC (Opec) production cuts have cut production by nearly 1.8 million barrels a day in June.

In terms of precious metals, Shanghai gold and silver rose nearly 0.1 per cent as concerns about an increase in coronavirus cases offset a boost to risk sentiment from positive US and Chinese economic data.

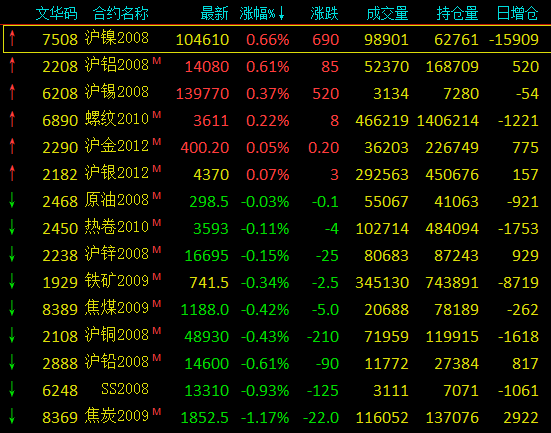

As of 09:35, the status of contracts in the metals and crude oil markets:

Brief comments on SMM:

Copper: on Friday night, Lun Copper closed at 6015 US dollars / ton, down 1.29%. Trading volume was 12000 lots, and short positions increased by 892 to 298000 lots. Shanghai Copper 2007 contract closed at 48850 yuan / ton, down 0.59%, with a turnover of 57000 lots and a long position reduction of 1987 to 120000 lots. There was a correction in copper prices on Friday. Lun Copper recovered its gains in the previous two days and broke the 5-day moving average, while Shanghai Copper closed down more than 400 yuan, mainly due to a large technical setback in the previous period, as well as a more obvious increase in domestic inventories on Friday. On the macro front, the manufacturing PMI index of China and the United States continued to improve in June compared with the previous month, and the added value of non-farm payrolls in the United States reached an all-time high in June, strengthening the expectation of sustained economic improvement; the central bank cut re-lending and rediscount interest rates since July 1, allowing local debt to replenish the capital of small and medium-sized banks, monetary policy sent a signal to amplify credit, and the favorable tone on copper prices remained unchanged. From a fundamental point of view, the increase in domestic inventory this week is mainly due to the influx of imported copper, although the actual consumption has entered the off-season, but the domestic production of electrolytic copper is restricted by raw materials, and the epidemic situation in South America continues to ferment, Codelco announced that the pandemic led to the suspension of the Teniente expansion project, the upstream supply port risk still exists, and there is also support for copper prices. On the spot side, the market inquiry atmosphere warmed up after the market fell, and traders' confidence in raising prices improved, and it is expected that the rising water level will be maintained today. It is estimated that today Lun copper 6000 won 6060 US dollars / ton, Shanghai copper 48800 won 49,100 yuan / ton. It is estimated that the spot water is 10 yuan / ton today-30 yuan / ton.

The second China (Yingtan) Copper Industry Summit Forum and the 15th China International Copper Industry chain Summit

Aluminum: the main 2008 contract of Shanghai Aluminum opened at 13985 yuan / ton last Friday morning, rising first and then falling in the afternoon, fluctuating around 14000 yuan / ton; rising steadily since Wan4 in the afternoon, reaching a intraday high of 14075 yuan / ton, closing at 14055 yuan / ton in late trading, trading volume decreased to 82000 hands, position increased to 168000 hands, daily line closed at Xiaoyang, weekly line closed at entity Dayang. The total position in the Shanghai Aluminum Index decreased slightly to 440000 lots, while the trading volume decreased to 161000 lots. The main force of Shanghai Aluminum opened slightly higher in the night market, then fluctuated in the range of 14010 won 14100 yuan / ton, and then closed at 14055 yuan / ton. The rising trend of aluminum futures remains unchanged, and the spot rising water has fallen somewhat. It is expected that the main operating range of Shanghai aluminum will be 13900mur14200 yuan / ton today.

Lead: lun lead continues a strong trend, market risk appetite is high, short-term is expected to continue to rise; Shanghai lead high decline, mainly suppressed by inventory accumulation, short-term lead prices continue to be weak. It is expected that today's SMM1# lead price will fall by 75 RMB125 / ton.

Zinc: last Friday, the main 2008 contract of Shanghai zinc opened at 16695 yuan / ton, which was driven up by the outer disk at the beginning of the day. After rising 16805 yuan / ton, Lun zinc was suppressed by the 5-day moving average, Shanghai zinc fell step by step, giving up intraday gains, accelerated the decline after a brief arrangement of 16685 yuan / ton, explored a low of 16615 yuan / ton, the bulls entered the bargain, the center of gravity of Shanghai zinc moved up to 16675 yuan / ton in a narrow range, and at the end of the day, Shanghai zinc tried to break, but the daily moving average fell back. The center of gravity was slightly adjusted to 16680 yuan / ton for consolidation, and finally closed down at 16690 yuan / ton, down 30 yuan / ton, or 0.18%. The trading volume increased to 66808 lots, and the position increased to 86499 lots. Last Friday, Shanghai zinc recorded two consecutive overcast, the center of gravity moved down, below the 20-day moving average support, MACD indicators into a dead fork. The zinc concentrate processing fee was raised for the first time in July, boosting the production will of the smelter, the supply side was loose, the consumer side was superimposed by the domestic traditional off-season and the development of overseas epidemic situation, and the downstream consumption was weaker than the previous month, restraining the action energy of Shanghai zinc. Pay attention to macro guidance in the short term. The contract price of Shanghai Zinc 2008 is expected to operate in the range of 16400 murals 16900 yuan per ton. It is expected that domestic Shuangyan zinc will increase the water price by 80,000,000 yuan / ton in July.

"SMM" 2020 (15th) lead and Zinc Summit

Nickel: last week, the nickel price basically fluctuated around the previous position, and the fundamentals were weak but mostly known news, such as the increase in the supply of nickel pig iron and the pressure on stainless steel market shipments in the off-season, etc., as a whole, the short-term contradiction is not obvious; in the macro aspect, some overseas data are bright, and in the major links, we can see that overseas countries are still following the logic of consumer recovery, coupled with the fact that national policies support enterprises to have a certain effect, and the macro side is relative preference. Under the comprehensive action, the nickel price fluctuates in the range. Nickel prices are likely to fall back high next week, focusing on whether long positions can hold on to a breakthrough. Shanghai Nickel 102000MUR 107,500 yuan / ton, Lunni 12650USD13300 / ton. Last Friday, the main contract of Shanghai Nickel changed month to 2010 contract, and the overnight Shanghai Nickel 10 contract opened at 106030 yuan / ton last Friday. The short positions increased sharply after the night trading opened, and the bulls did not have enough confidence to follow. Shanghai Nickel concussion fell below the 105000 barrier to explore a low night low of 104620 yuan / ton, and then rebounded slightly, and the center of gravity returned to around 105000 yuan / ton again, fluctuating narrowly until the close. At 104880 yuan / ton, the settlement price fell 960 yuan / ton, or 0.91%, compared with the previous trading day. The trading volume was 308000 lots, and the position increased by 7412 lots to 101000 lots. The overnight Shanghai Nickel 10 contract closed at the small negative column last Friday, with the K-pillar stable station above the moving average and the position of 105000 yuan / ton under pressure and oscillation. this week, the United States will release some important economic data, which is expected to perform well, and be on guard against the short-term fluctuations brought about by the data area. test the pressure at the 105000 gate today.

"2020 (Fifth) China International Nickel, Cobalt and Lithium Summit Forum

Tin: Shanghai tin trend: last Friday night, the main tin 2009 contract opened at 140050 yuan / ton, the highest was 140240 yuan / ton, and the lowest was 139200 yuan / ton. It closed at 139800 yuan / ton, up 10 yuan / ton, 9415 hands, 29385 positions, an increase of 224 hands. The main 2009 contract of Shanghai tin opened as high as 140050 yuan / ton last Friday night, then fluctuated all the way down under the joint influence of long short forces, hitting the lowest point of 139200 yuan / ton in the night market, and then the bulls entered the market. Shanghai tin rebounded and the center of gravity moved up slightly. It closed higher at 139800 yuan / ton in late trading. It is a cross star, the physical part is above all moving averages, the upper pressure level is expected to be around 140500 yuan / ton, and the lower support level is expected to be around 138000 yuan / ton 10-day moving average.

2020 China Ni-Cr stainless Steel Industry Market and Application Development Forum

Scan the QR code, apply for participation or join the SMM metal exchange group

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)